11g Release 6 (11.1.6)

Part Number E22767-06

Home

Contents

Book

List

Contact

Us

|

Oracle® Fusion Applications Cost Accounting and Receipt Accounting Implementation Guide 11g Release 6 (11.1.6) Part Number E22767-06 |

Home |

Contents |

Book List |

Contact Us |

|

Previous |

Next |

This chapter contains the following:

Manage Cost Organizations, Cost Organization Relationships, and Cost Books

Define Planning Cost Organizations, Planning Cost Components, and Estimate Mappings

Manage Cost Components and Cost Analysis Mappings

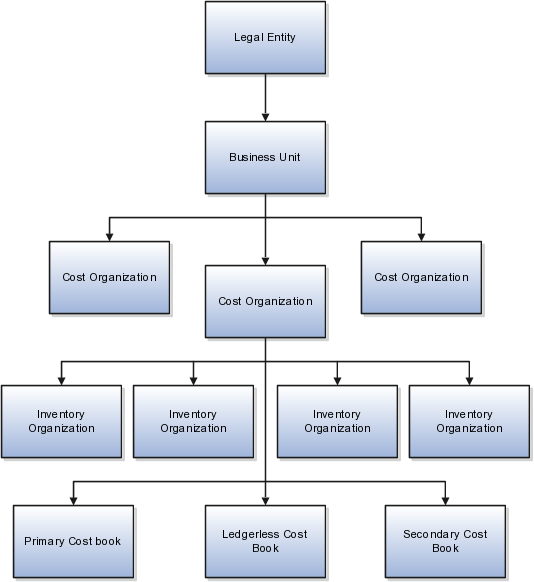

A cost organization structure comprises cost organizations, inventory organizations, and cost books. Your accounting and business needs determine how you set up your cost organization structure. This structure in turn determines how the cost processors create cost accounting distributions and accounting entries for inventory transactions.

This figure illustrates the relationship between cost organizations, inventory organizations, and cost books.

A cost organization can represent a single inventory organization, or a group of inventory organizations that roll up to a business unit. You can group several inventory organizations under a cost organization for financial reporting purposes. However a cost organization can map to only one business unit.

The inventory organizations that are assigned to a cost organization must all belong to the same legal entity.

For each cost organization, define an item validation organization from which the processor should derive the default units of measure. You can designate one of the inventory organizations assigned to the cost organization to be the item validation organization, or you can designate the item master organization to be the item validation organization.

A cost book sets the framework within which accounting policies for items can be defined. You can define different cost books for each of your financial accounting, management reporting, and analysis needs. By assigning multiple cost books to a cost organization, you can calculate costs using different rules simultaneously, based on the same set of transactions.

Every cost organization must have one primary cost book that is associated with the primary ledger of the legal entity to which the cost organization belongs. You can also assign secondary ledger-based cost books for other accounting needs, as well as ledgerless cost books for simulation purposes. For example, you could assign a primary cost book for financial reporting, a secondary cost book for business analysis, and a ledgerless cost book to simulate results using different cost calculations.

When you assign a cost book to a cost organization, you can optionally associate it with a ledger. The cost book then inherits the currency, conversion rate, cost accounting periods, and period end validations of that ledger. If you are assigning a ledgerless cost book, then you define these elements manually.

Set up your cost organization structure to accommodate your costing and accounting needs. The following discusses considerations for creating cost organizations, their association with inventory organizations, and their assignment to cost books.

When deciding what cost organizations to set up, consider the following:

Financial reporting. You typically create a separate cost organization for every business unit.

Data security needs. The cost organizations that you create may be determined by the separation of duties and security requirements for your users.

Note

You can use the effective start and end dates on the Manage Cost Organization Relationships page, to manage changes in the existence of a cost organization, for example, due to mergers, acquisitions, or restructuring.

By assigning cost organizations to a set, the entities defined at the set level can be shared by all the cost organizations belonging to that set. A cost organization set enables you to streamline the setup process, and helps you avoid redundant setup by sharing set-level definitions of your cost profiles, valuation structures, cost elements, and cost component groups across the cost organizations that belong to the set.

You also have the flexibility to assign cost organizations to different sets, for example if they are in different lines of business. That way you can segregate the definitions that are shared.

Your operation may lend itself to a simple configuration of one inventory organization to one cost organization. Or, when there are many inventory organizations in the same business unit, you may group several inventory organizations under a single cost organization for any of the following reasons:

Costing responsibilities. You may want to group inventory organizations that roll up to a manager or a cost accounting department under the same cost organization.

Uniform cost accounting. For example, if you want to define your overhead rules just once and apply them to transactions from several inventory organizations, you could group those inventory organizations into one cost organization.

Cost sharing. If there are items in more than one inventory organization for which you want a single average cost, those inventory organizations must fall under the same cost organization.

Note

You can use the effective start and end dates on the Inventory Organizations tab of the Manage Cost Organization Relationships page, to manage changes in the relationship of an inventory organization to a cost organization.

Every cost organization must be assigned one primary cost book that is associated with the primary ledger of the legal entity to which the cost organization belongs. You may also assign several secondary cost books as needed for other purposes such as: business analysis and management reporting, local currency accounting, or profit tracking of inventory items.

You can also assign ledgerless cost books to a cost organization for simulation purposes.

The following examples illustrate cost organization structures that support different cost accounting needs.

Set up three inventory organizations to optimize materials management across three different locations. Because they all belong in the same business unit and are managed by one cost accounting department, you could group them under a single cost organization; or you could assign each inventory organization to its own cost organization.

Three inventory organizations are geographically dispersed, and each one falls under a separate business unit. Create three cost organizations, and assign each inventory organization to its own cost organization.

Four inventory organizations are geographically dispersed. Two of them fall under one business unit, and two fall under another business unit. You could group the inventory organizations under two cost organizations corresponding to the two business units; or you could assign each inventory organization to its own cost organization.

Two inventory organizations in the same business unit need to share a single average cost for some items. These inventory organizations must belong to the same cost organization.

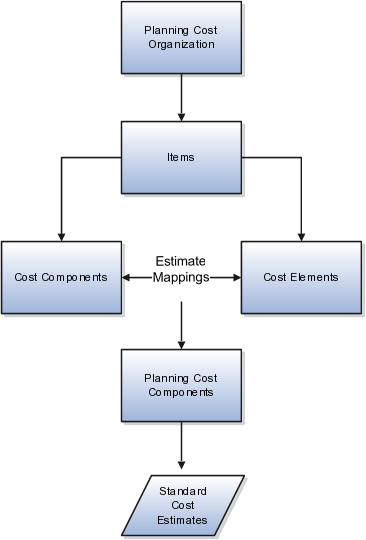

Standard cost planning refers to the process of estimating standard costs for use in the costing of inventory transactions. Planning cost organizations, planning cost components, and estimate mappings are the main elements used in the standard cost planning process.

This figure illustrates the relationship between the standard cost planning elements, and how they are used to generate standard cost estimates.

A planning cost organization is used to plan and estimate the standard costs of items. It is defined at the set level, therefore, you can associate it with all cost elements, cost components, planning cost components, and estimate mappings that belong to the same set.

After you finalize and approve a standard cost estimate, you publish it to a cost organization for accounting purposes; that is to say, the estimate is converted to a standard cost that can be used to cost inventory transactions.

You can create new estimates of standard costs based on cost components and cost elements that are derived from different sources. You can copy the following costs into a new cost estimate on the Copy Costs page:

Cost components from existing cost estimates

Cost components from existing standard costs

Cost elements from existing perpetual average costs

Cost elements from existing actual costs

On the Manage Estimate Mappings page, specify how to map cost components and cost elements to planning cost components. These mappings are used when you copy costs from existing standard cost estimates or existing costs, to a new standard cost estimate. You do this on the Copy Costs page, where you specify the estimate mapping that applies when copying a cost component or a cost element from the source cost or cost estimate to the destination cost estimate.

A cost organization can be used both as an accounting and a planning organization. A cost organization is used to cost inventory transactions using the perpetual average, actual or standard cost method; a planning cost organization is used to estimate standard costs.

You create a cost organization in the Oracle Fusion Global Human Resources application, on the Manage Cost Organization page. You then designate it as an accounting cost organization in the Oracle Fusion Cost Management application, on the Manage Cost Organization Relationships page, and its reference group attribute is automatically set to Costing Core Setups. You can also designate it as a planning cost organization on the Manage Planning Cost Organizations page, and its reference group attribute is automatically set to Cost Planning Setup.

Map cost components and cost elements to analysis codes within analysis groups. This enables you to define alternate views of item costs, and summarize costs for different reporting needs.

Map cost elements and cost components to as many analysis group and analysis code combinations as you need. For example, group cost elements into fixed and variable analysis groups, or direct and indirect analysis groups. Or you can map landed cost components to analysis groups to track landed cost charges from different sources.

You can assign a cost element to multiple analysis codes. An analysis code must be unique within an analysis group, and it can be reused in multiple analysis groups. For each analysis group you can set up a default analysis code that is used for cost elements that are not assigned to an analysis code.

The following are examples of cost elements mapped to analysis codes and analysis groups.

|

Analysis Group |

Analysis Code |

Cost Element |

|---|---|---|

|

AG1 |

Variable Cost |

Direct Material |

|

|

Inbound Freight |

|

|

Material Handling |

|

|

Outbound Freight |

|

|

Direct Labor |

|

|

Internal Profits |

|

Fixed Cost |

Store Supervisor |

|

|

Factory Rent |

|

AG2 |

Indirect Cost |

Outbound Freight |

|

|

Internal Profits |

|

|

Store Supervisor |

|

|

Factory Rent |

|

|

Electricity |

|

|

Depreciation |

|

Direct Cost |

Direct Material |

|

|

Inbound Freight |

|

|

Material Handling |

|

|

Direct Labor |

|

Default |

Miscellaneous Cost |

The following are examples of cost components mapped to analysis codes and analysis groups.

|

Analysis Group |

Analysis Code |

Cost Component |

Cost Component Source |

|---|---|---|---|

|

AG1 |

Variable Cost |

Direct Material |

Cost Planning |

|

|

Inbound Freight |

Landed Cost Management |

|

|

Material Handling |

User-Defined |

|

|

Outbound Freight |

Landed Cost Management |

|

|

Direct Labor |

Cost Planning |

|

|

Internal Profits |

Predefined |

|

Fixed Cost |

Store Supervisor |

Cost Planning |

|

|

Factory Rent |

User-Defined |

|

AG2 |

Indirect Cost |

Outbound Freight |

Landed Cost Management |

|

|

Internal Profits |

Cost Planning |

|

|

Store Supervisor |

Predefined |

|

|

Factory Rent |

User-Defined |

|

|

Electricity |

User-Defined |

|

|

Depreciation |

Predefined |

|

Direct Cost |

Direct Material |

Cost Planning |

|

|

Inbound Freight |

Landed Cost Management |

|

|

Material Handling |

Landed Cost Management |

|

|

Direct Labor |

User-Defined |

Yes. You can inactivate a user-defined cost component code at any time. You can delete a user-defined cost component code only if it is not mapped to a cost element or an analysis group, and it is not used in a standard cost definition.

Yes. You can delete or edit a cost component group mapping only if it is not referenced in a cost profile.

Yes. You can delete or edit the mapping of a cost element to an analysis group, even if the cost element is mapped to a cost component group that is referenced in a cost profile.