Understanding Cost Objects

Cost objects represent cost information about products, customers, and channels. They are the final results of the activities performed by your business—the focal points of costing and profitability analysis.

You already added product, customer, and channel data to your central repository of information—the Operational Warehouse - Enriched (OWE). In addition, you may have defined trees for the customer, product, channel, and department cost object types. Using Activity-Based Management, you can use these trees for the Activity-Based Management engine's cost object roll-up.

Understanding Cost Object Use

A primary cost object is the final customer, product, or channel. This is the object about which you want to derive cost or revenue information. Use a secondary cost object for costing components of a final customer, product, or channel.

Understanding Cost Object Groups

There are three cost object groups:

Single-dimensional

Multidimensional

Sustaining

Understanding Single-Dimensional Cost Objects

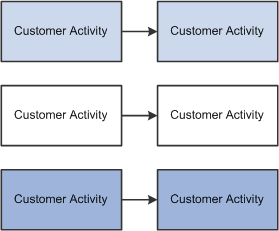

A single-dimensional cost object exists in a single Activity-Based Management dimension. Select a single, common dimension for each combination of activities and cost objects. The single-dimensional approach assures that every activity relates to a customer, product, or channel. These are linked through activity drivers to a corresponding customer, product, channel, or department cost object, letting you accurately measure costs.

Image: Example of single-dimensional cost objects

Single-dimensional costing preserves the cause and effect relationship between activities and cost objects as shown in the following illustration.

Understanding Multidimensional Cost Objects

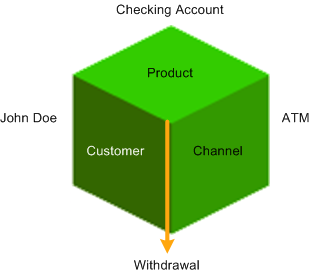

A multidimensional cost object — often referred to as transaction costing — is a combination of two or more Activity-Based Management dimensions such as those involved in a transaction. Multidimensional cost objects are useful in service-based organizations, such as banks, where costs are not easily defined as belonging to a customer, product, channel, or dimension. Many costs actually represent the point where multiple dimensions intersect. For example, when a customer withdrawals money from a bank's ATM, the specific transaction takes place at the intersection of three dimensions as shown in the following illustration.

Image: Example of a multidimensional cost object

Example of a multidimensional cost object.

Because you can derive multidimensional cost objects from transaction tables that record customer, product, and channel dimensions, metadata can group certain characteristics together to establish a costing basis. Using metadata to define table and data structures provides flexibility in developing models for your business since doing so lets you create multidimensional cost objects that you can use for costing.

Understanding Sustaining Cost Objects

The cost object supports the overall dimension or organization. Product-sustaining cost objects enable the production of individual products or services. Customer-sustaining cost objects let an organization sell to an individual customer, but are not independent of the volume or mix of the products and services sold and delivered to the customer. You can easily trace sustaining cost objects to the customer, product, or service for which the cost objects are performed. However, the quantity of resources used in the product- and customer-sustaining cost objects are independent of the production and sales volumes and quantity of production batches and customer orders.