4. Defining Attributes Specific to OTC Products

In this chapter, we shall discuss the manner in which you can define attributes specific to an OTC Options Interest Rate and Currency product.

4.1 OTC Options Products

This section contains the following topics:

- Section 4.1.1, "Create OTC Option products"

- Section 4.1.2, "Indicating Exchange Rate Variance"

- Section 4.1.3, "Specifying OTC Product Preferences"

- Section 4.1.4, "Specifying Main Details"

- Section 4.1.5, "Specifying Currency Option Preferences"

- Section 4.1.6, "Exotics"

- Section 4.1.7, "Specifying Interest Rate Option Preferences"

- Section 4.1.8, "Specifying Interest Rate Option Schedules Preferences"

- Section 4.1.9, "Specifying Rate Fixing Details"

- Section 4.1.10, "Specifying Swaption Details"

- Section 4.1.11, "Defining Interest Rate Option Schedules"

- Section 4.1.12, "Defining Charge Components for a Product"

- Section 4.1.13, "Defining Taxes for Product"

4.1.1 Create OTC Option products

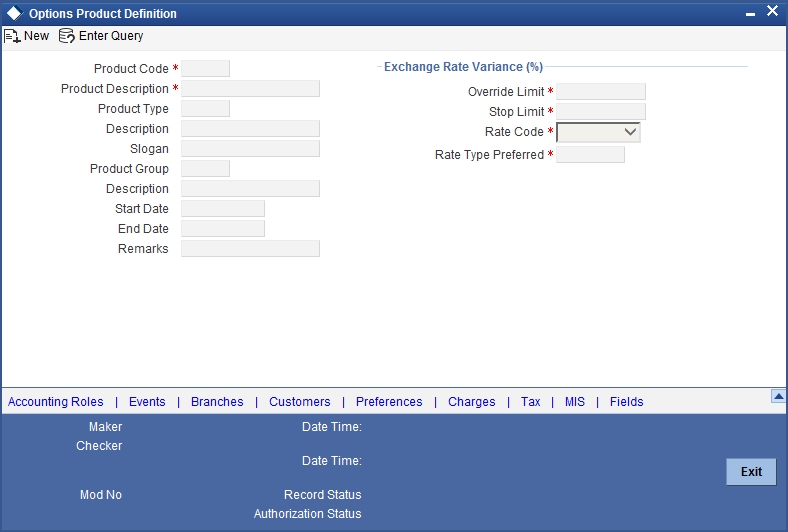

You can create OTC Options products in the ‘OTC Product Definition’ screen, invoked from the Application Browser. In this screen, you can enter basic information relating to a product such as the Product Code, the Description, etc.

You can invoke the ‘Options Product Definition’ screen by typing ‘OTDPRMNT’ in the field at the top right corner of the Application tool bar and clicking the adjoining arrow button.

The first attribute you define for a product is its Type. Once you have made this basic classification you can tailor the product to suit your requirements. Therefore, before you begin specifying the attributes of a product you have to indicate whether the product is an Interest Rate option product or whether it is a Currency option product.

Since you define products for convenience, all OTC deals involving the product inherit the attributes defined for the product. Yet, you have room for flexibility. You can change the inherited attributes of a specific option to suit your requirement at the time of processing it.

For any product you create in Oracle FLEXCUBE, you can define generic attributes, such as branch, currency, and customer restrictions, interest details, tax details, etc., by clicking on the appropriate icon in the horizontal array of icons in this screen. For an OTC product, in addition to these generic attributes, you can specifically define other attributes. These attributes are discussed in detail in this chapter.

You can define the attributes specific to an OTC product in the ‘OTC Product Definition Main’ screen and the ‘OTC Product Preferences’ screen. In these screens, you can specify the product type and set the product preferences respectively.

Product Type

The product type identifies the basic nature of a product. An options product that you create can either be an Interest Rate option or a Currency option. You will need to specify the product preferences depending on the product type.

4.1.2 Indicating Exchange Rate Variance

For a special customer, or in special cases, you may want to use an exchange rate (a special rate) that is greater than the exchange rate maintained for a currency pair. The variance is referred to as the Exchange Rate Variance.

When creating a product, you can express an Exchange Rate Variance Limit in terms of a percentage. This variance limit would apply to all contracts associated with the derivatives product.

The Override Limit: If the variance between the default rate and the rate input varies by a percentage that is between the Override Limit and the Rate Stop Limit, you can save the deal (involving the product) by providing an override.

The Rate Stop Limit: If the variance between the default rate and the rate input varies by a percentage greater than or equal to the Rate Stop Limit, you cannot save the deal.

Rate Code: While settling charges for cross currency settlements, you can choose to debit the customer by applying the mid rate or by using the buy/sell spread over the mid-rate.

Rate Type: In addition to specifying the Rate Code you have to indicate the Rate Type which should be picked up for exchange rate conversions involving settlement of charges for cross currency deals. You can maintain any one of the following as the Rate Type:

- Swaprate

- Spot

- Money

- Bills

- Standard

For further information on the generic attributes that you can define for a product, please refer the following Oracle FLEXCUBE User Manuals under Modularity:

- Product Definition

- Settlements

4.1.3 Specifying OTC Product Preferences

Preferences are the options available, for defining the attributes of a product. The instruments categorized under a product will inherit the preferences that are defined for it.

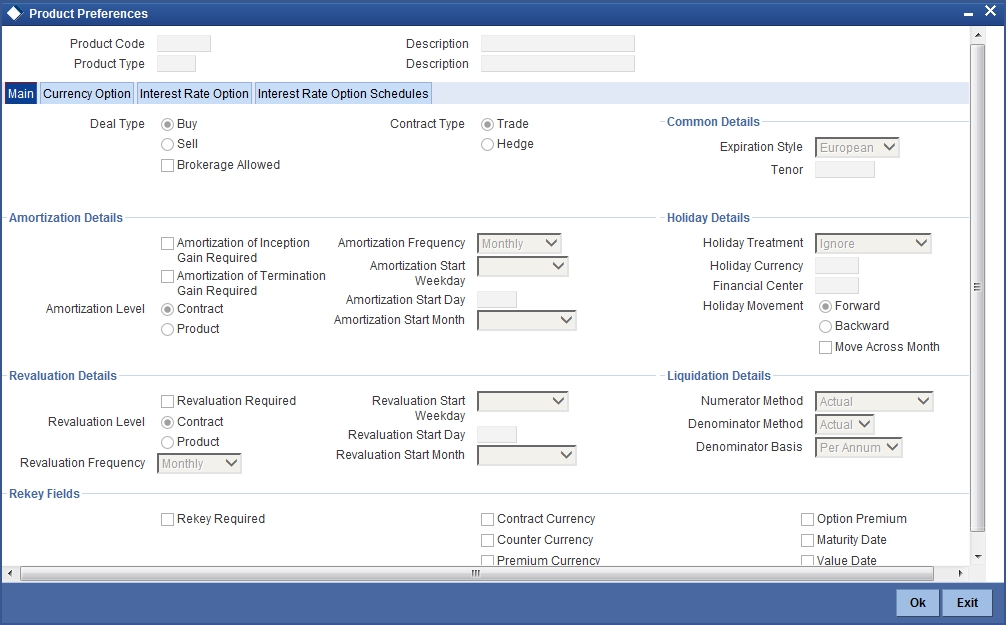

Click ‘Preferences’ button to invoke the ‘OTC Product Preferences’ screen. Through this screen you can define preferences for the product you are creating.

You will notice that the preferences screen gets displayed based on the product type. In case of an Interest rate Option product, the screen is classified into three sections:

- Main – wherein you specify the common preferences applicable to both IRO

- Interest Rate Option – wherein you can specify the attributes specific to an Interest Rate option

- Interest Rate Option Schedules – wherein you can define schedule for the IRO

However, in case of a currency option product, the screen has only two tabs:

- Main - wherein you specify the common preferences applicable to Currency options.

Currency Option - wherein you can specify the attributes specific to the currency options.

Each of the preferences has been documented in detail in the subsequent sections.

4.1.4 Specifying Main Details

The common features or attributes of the product that you need to capture in this tab are as follows:

Deal Type

Indicate whether the product caters to options wherein your bank is buying or selling options. You will be allowed to change this preference for a particular option.

Contract Type

Indicate whether the product is meant for Trade deals (Speculation on interest rate or spot rate movement) or Hedge deals (Protection against risk due to interest rate or spot rate movement). You will be allowed to change this preference while processing a specific deal.

Brokerage Allowed

Enabling this preference indicates that option deals involving this product can involve brokerage.

4.1.4.1 Specifying Common Details

As part of specifying the common details for Interest Rate and Currency options, you can specify the following details:

Expiration Style

You can choose to specify any one of the following methods for contract expiration:

- European - exercise possible only on maturity date

- American - exercise possible between any pre specified date and the maturity date

- Bermudan - exercise possible only on some pre specified dates before the maturity date and the maturity date itself.

Apart from Swaptions, for all other Interest Rate options, expiration is allowed only on maturity date (European), since the settlement is always done on the Maturity Date if the option is in-the-money.

For Swaptions the expiration style can be American or Bermudan or European. You will have to manually enter into an Interest Rate swap incase of a deliverable Swaption (by specifying the details of the Interest Rate Swap in the ‘DV Contract Online’ screen) and manually exercise the Swaption by entering the settlement amount (Cash settled Swaption)/Swap Value (Physically settled Swaption).

The following expiration styles are allowed for Currency Options:

| Option Style | Expiration Style | ||

|---|---|---|---|

| Plain Vanilla | American, Bermudan, European | ||

| Binary | American and European | ||

| Digital | European | ||

| No Touch | European |

Tenor (Days)

You will also have to indicate the periodicity of the Options deal involving the product. The periodicity is indicated in terms of days and can be changed while processing a specific contract.

4.1.4.2 Specifying Amortization Details

You need to specify the following amortization details.

Amortisation Inception Gain Required

Check this box if you want the inception gain (if any) to be amortized. At the time of inception, Gain is distributed throughout the period of the contract - from Effective Date to Maturity Date.

Amortisation of Termination gain Required

Indicate whether you want to amortize the deferred Termination Gain if an option deal involving the product is terminated prematurely. At the time of termination, Gain is distributed throughout the period of the contract from Termination Date to Maturity Date. This feature is applicable only for hedge deals. In case of termination gain, the amortization will happen from the Date of Termination till the Maturity Date of the contract. Whereas; in case of inception gain, the amortization will happen from the Effective Date till the Maturity Date of the contract.

Amortisation Level

Specify at which level you want the system to perform amortisation. It should be performed either at the Product or at the Contract level. At the product level accounting entries involving all products will be netted and a single entry will be posted for all deals involving the product.

Amortisation Frequency

Specify the frequency of amortization. The options available are Weekly, Monthly, Quarterly, Half Yearly and Yearly.

Amortisation Start Weekday / Start Day / Start Month

In case of a Weekly frequency, you have to specify the day of the week on which amortization should start. If the frequency is fortnightly or monthly, you will have to specify the date on which the amortization should start. Similarly, when the frequency is Half-yearly or Yearly you have to select the month of the year in which the amortization should start.

Note

If you choose to amortize inception gain, the same is amortized over a period from the value date of the option contract till its maturity / termination, irrespective of the date of payment of the premium.

Processing Impact

The system processes contracts involving the product based on the preferences you set. Accordingly, the following activities are performed during processing:

- Amortization is done only for deferred gains (Inception Gain, Time Value in case of hedge deals and termination gains). There will be no amortization of Inception and termination loss and these will be recognized as Expense as and when they are incurred.

- Amortization of Time Value in case of hedge deals is based on the Revaluation parameters (level, frequency etc.) since it is actually the revaluation of the contract.

- The following fields will not be defaulted to the contracts involving

the product:

- Amortize Inception Gain

- Amortize termination gain

- Revaluation required

- Moreover, you will not be allowed to modify your preferences for these options if a contract involving the product are still active.

- If a day which is not present in a month has been selected as the Amortization Start Day or Termination Start Day, the Start Day will be taken as the last day of the current month. For instance, if you have selected 31 as the Amortization Start Day, with the frequency as Monthly, and the processing month is February, the processing will be done on the 28th of the month. Else it will be done on the 29th if it is a leap year.

4.1.4.3 Specifying Holiday Details

Here, you can capture the following holiday details:

Holiday Treatment

Specify the holiday treatment. In Oracle FLEXCUBE, a Maturity Date falling due on a holiday can be treated in any of the following ways:

- Ignore the holiday - In which case the holiday will be ignored and the Maturity Date will be retained as per the frequency.

- Choose to follow the Local holiday - The contract Maturity Date will be defaulted on the Next Working Day or the Previous Working Day, as per your specifications in the ‘Branch Holiday Maintenance’ screen.

- Choose to follow the Currency holiday - The movement of the Maturity Date will be based on the holiday calendars maintained for the currency specified in the Holiday Currency field.

Holiday Currency

If you have chosen the holiday treatment as Currency, indicate the currency code in this field. Resultantly, the movement of the Maturity Date will be based on the holidays maintenance for the currency code that you identify in the Holiday Currency field.

Financial Center

Here, you can indicate that the holiday treatment needs to be governed by the Financial Center. In such a case, the movement of the Maturity Date will be based on the holidays maintenance for the financial institution (Clearing House) that you identify in the Financial Center field.

If you choose to follow either the currency holiday or the holiday calendar maintained for the financial center, you need to specify the currencies/financial institutions for deals involving the product. In the event, a Maturity Date falls due on a holiday, the system computes the next maturity date based on the combination of holiday calendars maintained for all the currencies/financial institutions that you have specified for the contract. Therefore, in effect, the next maturity date for a contract will be a working day in all the calendars involved in the contract.

Holiday Movement

Occasionally the preferred holiday treatment, the branch holiday, the currency holiday or the holiday governed by the financial center may in turn fall on a holiday. In such a situation you have to indicate the movement of the maturity date. Whether it is to be moved forward to the next working day or whether it should be moved backward to the previous working day.

Moving the Maturity Date across Months

If you have chosen to move the Maturity Date falling due on a holiday either forward or backward, such that it falls due on a working day, and it crosses over into another month, the maturity date will be moved into the next month only if you so indicate. If not, the maturity date will be kept in the same month.

4.1.4.4 Specifying Revaluation Details

Here, you can capture the following details:

Revaluation Required

You have to indicate whether a contract involving the product needs to be revalued. Check this box if you need the product to be revalued.

Revaluation Level

If you enable this preference you have to specify the level at which revaluation is to be performed. At the product level, revaluation entries are netted and passed for all deals involving the product.

Revaluation Frequency

Select the frequency at which revaluation is to be performed from the adjoining drop-down list. The list displays the following values:

- Daily

- Monthly

- Quarterly

- Half yearly

- Yearly

Revaluation Start Weekday / Start Day / Start Month

Depending upon the revaluation frequency that you have set, i.e. monthly, quarterly, half yearly or yearly revaluation, you should specify the date on which the revaluation should be done during the month. For example, if you specify the date as ‘30’, revaluation will be carried out on that day of the month, depending on the frequency.

If you want to fix the revaluation date for the last working day of the month, you should specify the date as ‘31’ and indicate the frequency. If you indicate the frequency as monthly, the revaluation will be done at the end of every month -- that is, on 31st for months with 31 days, on 30th for months with 30 days and on 28th or 29th, as the case may be, for February.

If you specify the frequency as quarterly and fix the revaluation date as 31, the revaluation will be done on the last day of the month at the end of every quarter. It works in a similar fashion for half-yearly and yearly revaluation frequency.

If you set the revaluation frequency as quarterly, half yearly or yearly, you have to specify the month in which the first revaluation has to begin, besides the date on which the revaluation should be done.

Processing Impact

For Hedge deals amortization of Time Value is performed only if the Revaluation Required option has been enabled.

If the Amortize Inception Gain option has not been enabled, Inception Gain, if any will be treated as income directly on inception of the options deal. Also termination gain for hedge deals will be amortized only if the Amortize Termination Gain option has been enabled for the product, else any termination gain will be treated as income on termination and will not be amortized.

4.1.4.5 Specifying Liquidation Details

While setting up Interest Rate option products you have to specify the liquidation parameters which include the following:

Numerator Method

Select the method that is used to calculate the number of days between the schedule start and end dates for calculating the settlement amount from the adjoining drop-down list. The list displays the following values:

- 30 EURO

- 30-US

- 30-ISDA

- 30-PSA

- Actual

- Actual-Japanese

Denominator Method

Select the method that is used to calculate the number of days in a year for the calculation of the settlement amount from the drop-down list. The list displays the following values:

- Actual

- 365

- 360

Denominator Basis

It is used to determine whether the difference between the Strike Rate and the Reference Rate is to be taken for the whole year or for the schedule period during Settlement Amount calculation. The basis can either be Per Period or Per Annum.

4.1.4.6 Specifying Rekey Fields

When an Option contract is invoked for authorization - as a cross-checking mechanism, you can specify that the values of certain fields should be entered before the contract is authorized. This is called the Rekey option. Check the box ‘Rekey Required’ to enable this option.

While defining the product you have to indicate the fields whose values you need to enter before a contract is authorized. Thus it becomes mandatory for you to enter the values of rekey fields for all contracts linked to the product.

You can specify any or all of the following as rekey fields:

- Contract Currency

- Option Premium

- Counter Currency (applicable only for Currency options)

- Maturity Date

- Premium Currency

- Value Date

If no rekey fields have been defined, the details of the contract will be displayed immediately when the authorizer calls the contract for authorization.

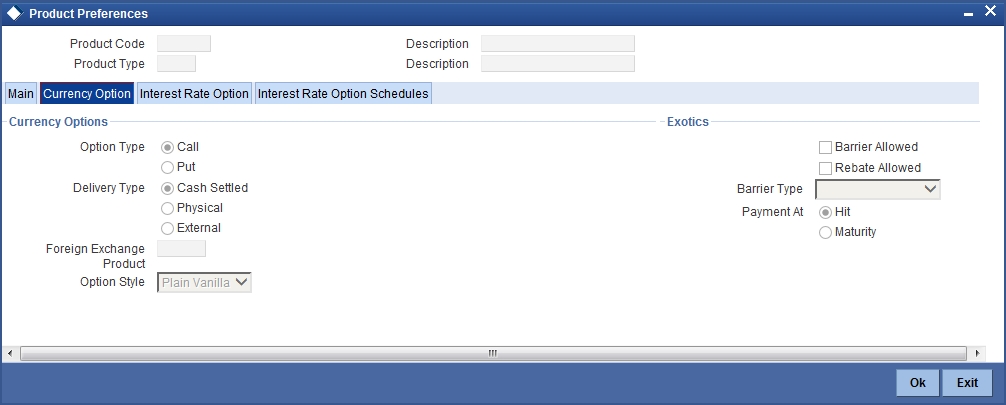

4.1.5 Specifying Currency Option Preferences

Since currency option preferences are specific to currency options the Currency Option tab will be displayed only if you have indicated that you would like to define products meant for Currency Options.

4.1.5.1 Specifying Currency Options

You will need to specify the following attributes about Currency Options:

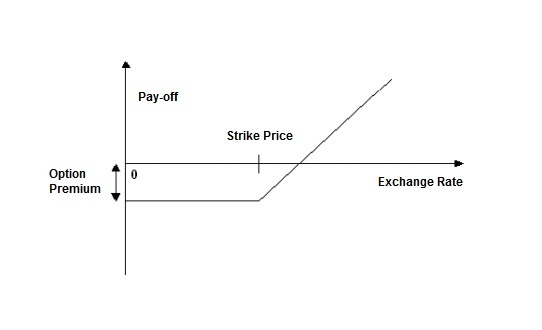

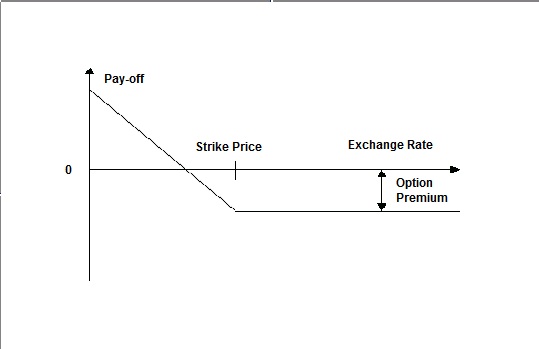

Option Type

Indicate whether the currency option you are defining is a Call option or a Put option.

- A call option gives the buyer the right to buy a specified quantity of a certain currency (contract currency) against another (counter currency) at a specified exchange rate on or before a pre-specified future date. If, on the specified future date, the market exchange rate is lower than the rate specified in the call option, the buyer will not exercise the right and, instead, buy the contract currency at the more favorable market rate.

- A put option gives the buyer the right to sell a specified quantity of a certain currency (contract currency) against another (counter currency) at a specified exchange rate on or before a pre-specified future date. If, on the specified future date, the market exchange rate is higher than the rate specified in the put option, the buyer will not exercise the right and, instead, sell the contract currency at the more favorable market rate.

Currency Options, thus, protect the buyer against adverse exchange rate movements, while giving the buyer the benefit of favorable exchange rate movements.

The buyer’s pay-off for a call option can be graphed as follows:

The buyer’s pay-off for a put option can be graphed as follows:

Delivery Type

Options involved in a product can either be allowed to get into future FX deals (Physical) or you can opt for a net cash agreement on exercise (Cash Settled) or could be external (through uploads). If you choose Physical as the delivery type, you will have to identify the Spot FX product which is to be used to upload an FX contract. If you choose the Cash Settled option, you will have to indicate whether the option style is any one of the following:

- Plain Vanilla - This is a contract which provides the buyer the right but not the obligation to buy or sell the underlying currency at a predetermined rate. The expiration style can be American, European or Bermudan. This is a standard currency option. It becomes a non-standard option if exercised with a barrier.

- Binary - This is an agreement, under which a fixed amount is paid by the option writer to the option holder if a specific condition is met at any time during the exercise period. The payment of the fixed amount can be either at the time when the specific condition is met (in case of American options) or on the expiration date (in case of European options).

- Digital - This is an agreement, under which a fixed amount is paid by the option writer to the option holder if a specific condition is met on the expiration date. In essence, this is a binary option with European expiration style.

- No Touch – This is an agreement, under which a fixed amount is paid by the option writer to the option holder unless a specific condition is met on the expiration date. Only European style of expiration is possible for no touch options. This is similar to a knock-out option, as explained later.

Foreign Exchange Product

If you have chosen the delivery type is 'Physical' it is necessary to provide the details of FX product. Select the appropriate one from the option list.

Option Style

Choose the option style from the drop-down menu which displays the following values:

- Plain Vanilla

- Binary

- Digital

- No Touch

For details on Option Style, refer the explanation on Delivery Type given above.

4.1.6 Exotics

Barrier Allowed

A barrier is a predetermined underlying asset price at which the deal ceases to exist (gets knocked out) or comes into existence (gets knocked in). You can indicate whether a barrier can be used for knock-in or knock-out of an option. If you enable this preference you will have to identify the barrier type. The options available are:

- Single Knock In - A deal comes into existence if a pre specified asset price is met between the start and end of the barrier window.

- Single knock Out - A deal will cease to exist (Knocked-out) if a pre specified asset price is met between the start and end of the barrier window. A pre determined rebate amount is paid in this case.

- Double Knock In - A deal will come into existence if any of the two pre specified underlying asset prices are met between the start and end of the barrier window.

- Double Knock Out - A deal will cease to exist if any of the two pre specified underlying asset prices are met between the start and end of the barrier window. A pre determined rebate amount is paid in this case.

Refer to Annexure B for examples on the various type of exotic currency options.

Rebate Allowed

Enabling this preference indicates whether a rebate can be paid if a contract involving the product gets knocked-out. Rebate is usually given for contracts that are knocked-out before maturity due to a single or double knock-out barrier hit. Banks might want to give a rebate on the option premium to a certain percentage of the premium in case of a knock-out. The amount which is given as rebate can be credited to the counterparty’s account either at Hit or at contract maturity which is determined by the field ‘Payment At’ described below.

Barrier Type

Choose the barrier type from the drop-down menu. Oracle FLEXCUBE allows you to select any one of the following:

- Single Knock In

- Single Knock Out

- Double Knock In

- Double Knock Out

Payment At

Rebate payment for a knock-out option can be made either at Hit or at Maturity. When an option gets knocked-out it is considered a Hit. At the product level you have to indicate whether the Rebate amount has to be paid at Hit or at Maturity.

Although you have set these as preferences at the product level, for a specific Currency Option you will be allowed to change the following details:

- Option Type

- Delivery Type

- Option Style.

- Barrier Type

- Payment At

4.1.7 Specifying Interest Rate Option Preferences

Interest Rate preferences are specific to interest rate options. You will be able to access the Interest Rate tab only if you are defining interest rate products.

The preferences specific to Interest Rate options are as follows:

4.1.8 Specifying Interest Rate Option Schedules Preferences

Here, you can capture the following details:

Interest Rate Options Type

Indicate whether the Interest Rate option product is meant to cater to any one of the following types:

- Caps

- Collars

- Corridors

- Floors

- Swaptions

Caps

A cap is a series of call interest rate options with multiple exercise dates. A cap gives the buyer the right to enter into strips of notional future borrowings at a pre-agreed rate (strike rate), thus protecting him against interest rates moving above this pre-agreed rate.

Floors

A floor is a series of put interest rate options with multiple exercise dates. A floor gives the buyer the right to enter into strips of notional future lending at a pre-agreed rate (strike rate), thus protecting him against interest rates moving below this pre-agreed rate.

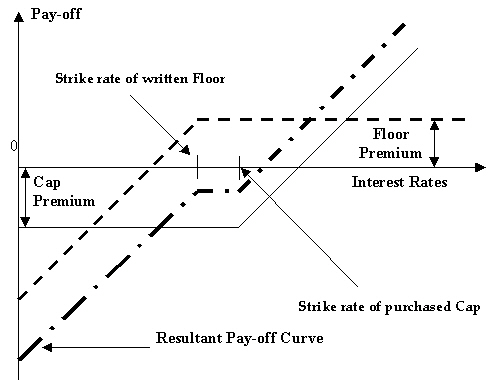

Collars

A collar is a combination of a purchased cap and a written floor. This enables the buyer to lock in to an interest rate band.

For example, a floating-rate borrower buys a cap to protect herself against a rise in interest rates above the strike rate. The price of this protection is the premium she pays for the cap. The cap, of course, allows her to go on enjoying the benefits if market (reference) interest rates remain below the strike rate – in such events, she does not exercise the cap and uses market rates to apply to her borrowings. However, if she has a view that market rates are not likely to fall below a certain rate (which is below the cap strike rate), then she may choose to forgo part of the benefits of low market rates in return for a reduction in the premium that she pays for the cap.

She achieves this by simultaneously writing a floor, the strike rate of which is lower than the strike rate of the cap that she has purchased. She is of the view that market interest rates are unlikely to go below the strike rate of the floor and, therefore, the floor has little probability of being exercised by the counterparty. The premium that she receives on the floor partially offsets her premium outgo on the cap.

The above set of deals are bundled in a collar. Suppose Bank A buys a collar from Bank B. This means that Bank A has purchased a cap from Bank B and written a floor favoring Bank B. The following outcomes are possible, depending on various interest rate scenarios:

| Interest rate scenario | Outcome | ||

|---|---|---|---|

| Market interest rate is more than the cap strike rate | Bank B pays to Bank A for the difference between market rate and cap strike rate. | ||

| Market interest rate lies between the floor strike rate and the cap strike rate or is equal to either of them | No payment is exchanged. | ||

| Market interest rate is less than the floor strike rate | Bank A pays to Bank B for the difference between the floor strike rate and the market rate. |

The pay-off for the buyer of a collar is shown in the diagram below:

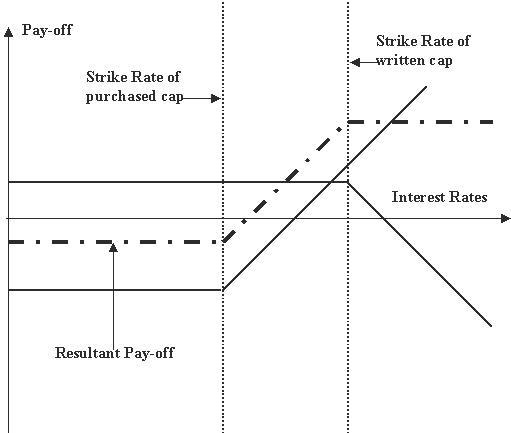

Corridors (also called Bull Spreads)

A corridor or a bull spread is a combination of a cap purchased at a certain strike rate and another (otherwise equivalent) cap written at a higher strike rate. Like a collar, a corridor is also a premium mitigation strategy.

An entity with floating-rate borrowings buys a cap to protect itself against interest rates rising above the strike rate of the cap. However, it also feels that there is a limit to the possible rise in interest rates. Therefore, it is willing to sacrifice part of its gains arising from high market interest rates – that is, opportunity gains arising from having purchased the cap -- in return for a reduction in the premium that it pays for the cap. It achieves this by selling a cap with a strike rate higher than that of the original cap, the premium income on the sold (written) cap partially offsetting the premium outgo on the purchased cap.

The above sets of deals are bundled in a corridor. Suppose, Bank A buys a corridor from Bank B. This means that Bank A has purchased a cap – say, cap 1 - from Bank B and written a cap – say cap 2 -- favoring Bank B. The strike rate of cap 1 is lower than that of cap 2.

The following outcomes are possible, depending on various interest rate scenarios:

| Interest rate scenario | Outcome | ||

|---|---|---|---|

| Market interest rate is equal to or more than the strike rate of cap 2. | Bank B pays Bank A for the difference between the strike rates of cap 1 and cap 2. | ||

| Market interest rate lies between the strike rates of cap 1 and cap 2. | Bank B pays Bank A for the difference between market interest rate and cap 1 strike rate. | ||

| Market interest rate is equal to or less than the strike rate of cap 1. | No payment is exchanged. |

The pay-off for the buyer of a corridor is shown in the following figure:

Swaptions

A swaption is an option on a swap. It gives the buyer, on payment of an advance fee, the right, but not the obligation, to enter into an interest rate swap at a specified future date, at a particular fixed rate and for a specified term.

Refer to the Derivatives manual for details on Interest Rate Swaps (IRS).

The terms of a swaption that the buyer and the seller agree on are:

- The strike rate

- The length of the swaption period (which usually ends on the starting date of the swap if the swaption is exercised)

- The notional amount for the underlying swap

- The frequency of settlement under the underlying swap

- Other terms of the underlying swap

Maximum Spread

Indicates the maximum spread over and above the Reference Rate. You can specify the spread in terms of a percentage.

Payment Method

The payment method can either be in Advance or in Arrears. If you select Advance, payment will have to be made at the beginning of a schedule. If you select Arrears, settlement will be done at the maturity of a schedule.

Allow External Rate Revision

Check this box to indicate that for the contracts linked to this product, you can allow rate revision based on the rates uploaded from an external system.

4.1.9 Specifying Rate Fixing Details

Here, you can capture the following details:

Rate Fixing Lag (Days)

Indicate the number of days before or after the schedule maturity or schedule start date for the reference rate reset to be done.

Reset Date Basis

Indicate whether the reference reset lag is with reference to the Period Start Date (schedule begin date) or the Period End Date (schedule maturity date).

Reset Date Movement

The reset lag for the reference rate can be fixed before (Backward) or after the period start or begin date (Forward).

4.1.10 Specifying Swaption Details

Here, you can capture the following details:

Swaption Style

Indicate whether the product you are defining is meant for actual interest rate swaps (Physical) or for cash settled swaps or for external swaps (if this product is to be used for uploaded contracts).

For physically settled Swaptions, there will be an underlying derivatives swap deal which will get initiated once the Swaption contract is exercised.

For cash settled Swaptions, the swap value of the contract needs to be calculated outside the system and the same needs to be entered during manual exercise of the Swaption deal.

Swap Product

Specify the swap product. This is applicable in case of actual interest rate swaps. You will have to identify the swap product which will be used to default the details of the Derivatives contract.

Processing Impact

The processing impacts are given below.

- While specifying the common preferences if you have selected Hedge as the Contract Type, you will not be allowed to specify Collar as the IRO Type.

- If you have chosen Advance as the Payment Method, then you have to necessarily specify Backward as the Reset Date Movement and Period Start Date as the Reset Date Basis.

- You will not be allowed to upload Derivative contracts for physically settled swaptions. To save an interest rate swap, you will have to invoke the ‘Derivatives Online’ screen from the ‘Contract Online’ screen.

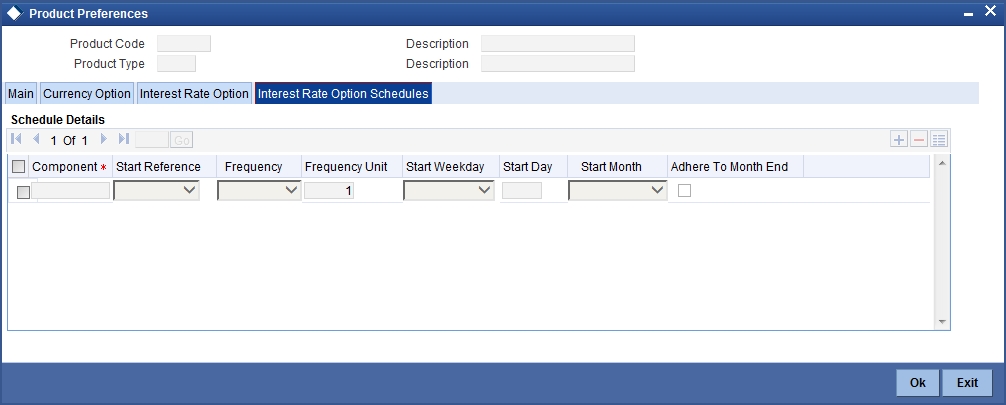

4.1.11 Defining Interest Rate Option Schedules

For an Interest Rate option product, in addition to specifying Interest Rate preferences, you will have to define the default schedules for the payment of settlement amount at maturity. Click on the Interests and Rate Option Schedules tab in the ‘Options Product Preferences’ screen.

The Settlement Amount (SETTLE_AMT), which is the component for which the schedule is to be defined, is displayed in this screen. You will not be allowed to change it. You can define the schedules for this component by capturing the following details:

Start Reference

This can either be the Value Date or the Calendar Date. If you specify Value Date as the Start Reference, the settlement schedule will be calculated using the frequency and frequency units with reference to the contract value date. If the start reference is Calendar date, the settlement schedule will be calculated based on the frequency, frequency units, start day, start weekday and start month (whichever is applicable).

Frequency

The Frequency of the schedule can either be Daily, Weekly, Monthly, Quarterly, Half Yearly or Yearly.

Frequency Units

The number of frequency units after which a schedule should repeat. For example, a monthly frequency with a frequency unit of 2 is effectively a bi-monthly schedule.

Start Weekday

This is the day of the Week on which a schedule should start. You will need to specify the Start Weekday only if the Frequency is Weekly. You can select any day from Sunday to Saturday.

Start Day

This is the day on which a schedule should start. You can select any day of the month from the 1st to the 31st. You need not indicate the Start Day if the Frequency selected is Daily or Weekly.

Start Month

This is the month from which a schedule should start. You will need to indicate the Start Month only in case of Quarterly, Half-yearly and Yearly frequencies.

Adhere to Month End

This indicates whether a schedule should adhere to month ends if the maturity date is a day less than the month end date. For example a quarterly schedule starting on 31st January will have schedule maturity on 30th April, 30th July and 30th October if you have failed to enable this option. But if you enable this option, the schedule maturity will be performed on the 30th of April, 31st of July and 31st of October.

Note

It is mandatory to visit the ‘Schedules’ screen and add an empty row. The system will default 'SETTLE_AMT’ as a component in that.

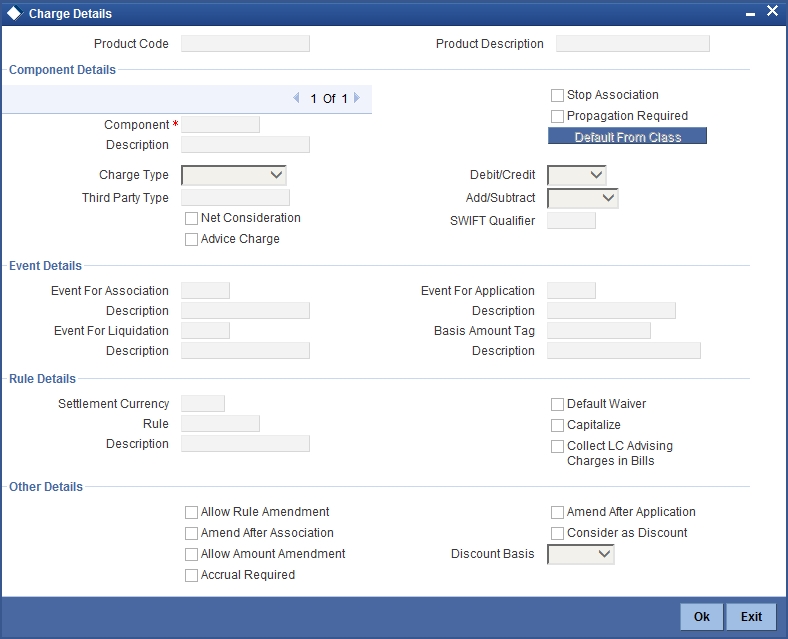

4.1.12 Defining Charge Components for a Product

A charge ‘class’ is a specific type of component that you can build with certain attributes. You can build a charge class, for instance, with the attributes of a specific type of charge component, such as ‘Charge for Manual Exercise’.

You can specify the different charge components for a product, in the ‘Product Charge Definition’ screen, by associating the product with the different charge classes you have built.

Click ‘Charges’ button to invoke the ‘OTC Product Charges’ screen.

In this screen, you can define the charges for the product that you are creating.

To associate a charge class to a product that you are defining, choose the ‘Default From Class’ button. A list of the classes that you have defined specifically for the OTC Interest Rate/Currency options module will be displayed. Choose the class (or classes) that you would like to associate with the product.

Charges for the portfolios maintained under the product will be calculated on the basis of the associated charge classes.

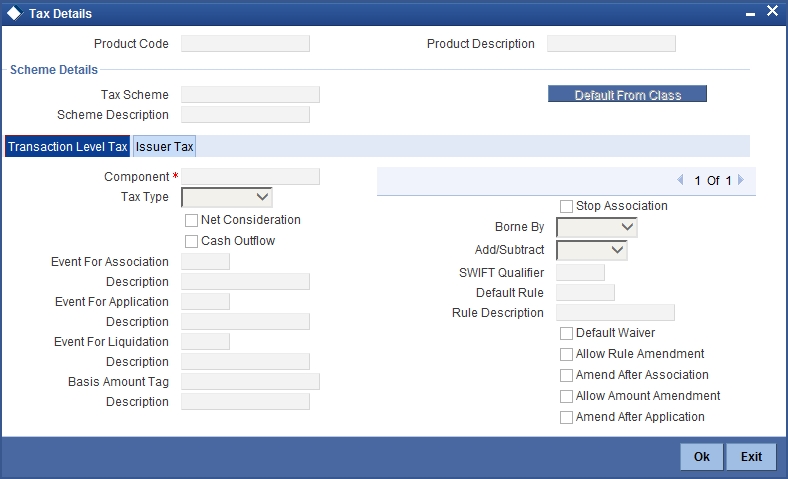

4.1.13 Defining Taxes for Product

A tax ‘class’ is a specific type of component that you can build with certain attributes. You can build a tax class, for instance, with the attributes of a specific type of tax, such as ‘Options tax’. You can group several tax classes into a Tax Scheme Class.

You can specify the taxes for a product, in the ‘Product Tax Definition’ screen, by associating the product with a tax scheme class you have built. (Please note that you cannot define a tax component specific to a product.)

To associate a tax scheme class with a product that you are defining, choose the ‘Default From Class’ button. A list of the tax scheme classes that you have defined specifically for OTC Interest Rate/Currency options module will be displayed. Choose the class that you would like to associate with the product.

Taxes for the portfolios maintained under the product will be calculated on the basis of the associated tax scheme classes.