4. Defining Product Categories and Products

You may offer your customers a variety of financial services such as Vehicle Mortgages, Home Mortgages, Personal Mortgages, and so on. The different types of mortgages can be different ‘Product Categories’. A product category is used to distinguish between the various mortgage services offered by the bank. Each of these mortgages are totally different and hence the need to categorize them.

Under a product category, you may have mortgages that may vary in features such as pricing, tenor, amount etc. Each variation of these services can, therefore, be considered as ‘Products’.

At the time of capturing a mortgage application, you would specify details such as Mortgage Amount, Tenor, and Asset Class etc. The system automatically resolves the Product Category and Product applicable based on the application details. Hence, the Mortgage Account is created under the appropriate product.

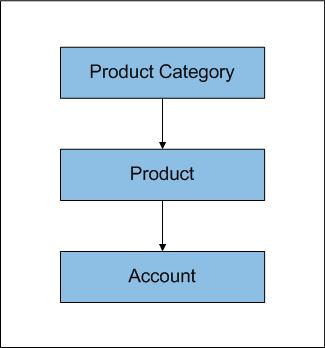

The Mortgages Module will have an inheritance hierarchy as follows:

This chapter explains the procedure for setting up product categories and products.

This chapter contains the following sections:

- Section 4.1, "Product Categories"

- Section 4.2, "Processing of IRR application on Mortgages"

- Section 4.3, "Customized Products"

4.1 Product Categories

This section contains the following topics:

- Section 4.1.1, "Maintaining Product Categories"

- Section 4.1.2, "Setting up a Mortgages Product"

- Section 4.1.3, "Defining Other Attributes for a Product"

- Section 4.1.4, "Specifying User Data Elements"

- Section 4.1.5, "Indicating Preferences for a Product"

- Section 4.1.6, "Specify Components Details"

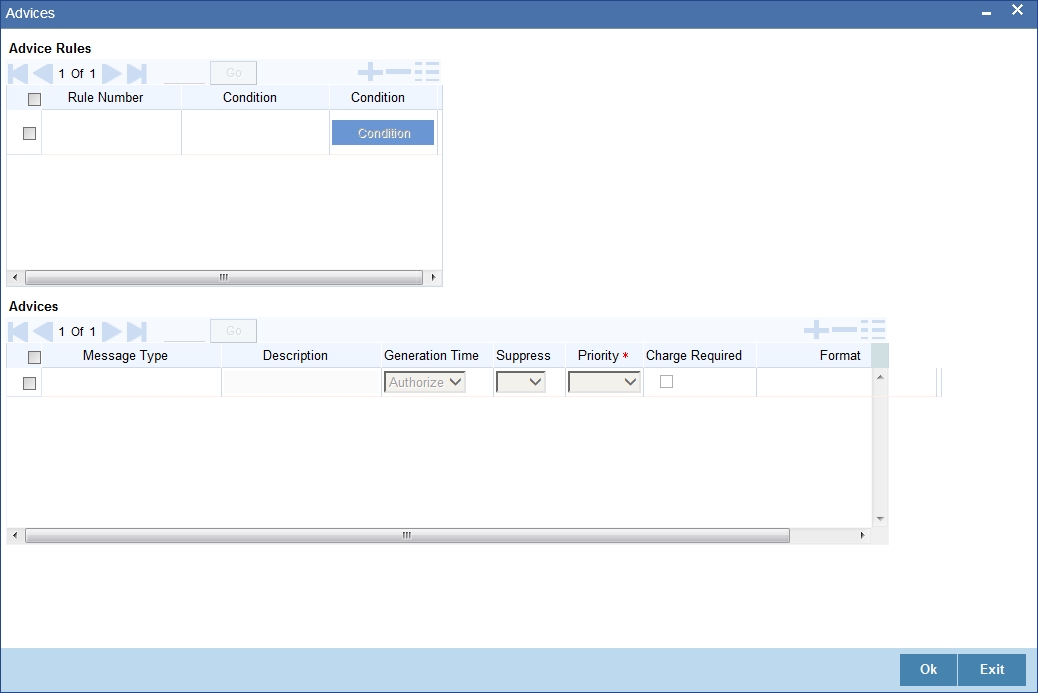

- Section 4.1.7, "Associating Notices and Statement "

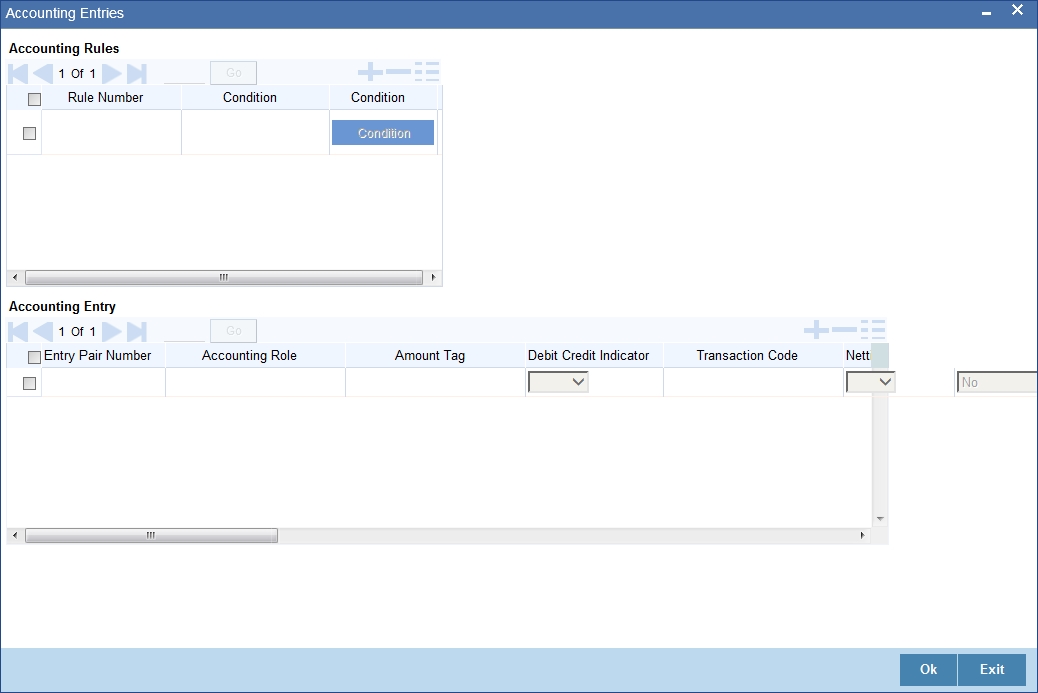

- Section 4.1.8, "Mapping Accounting Roles to Product"

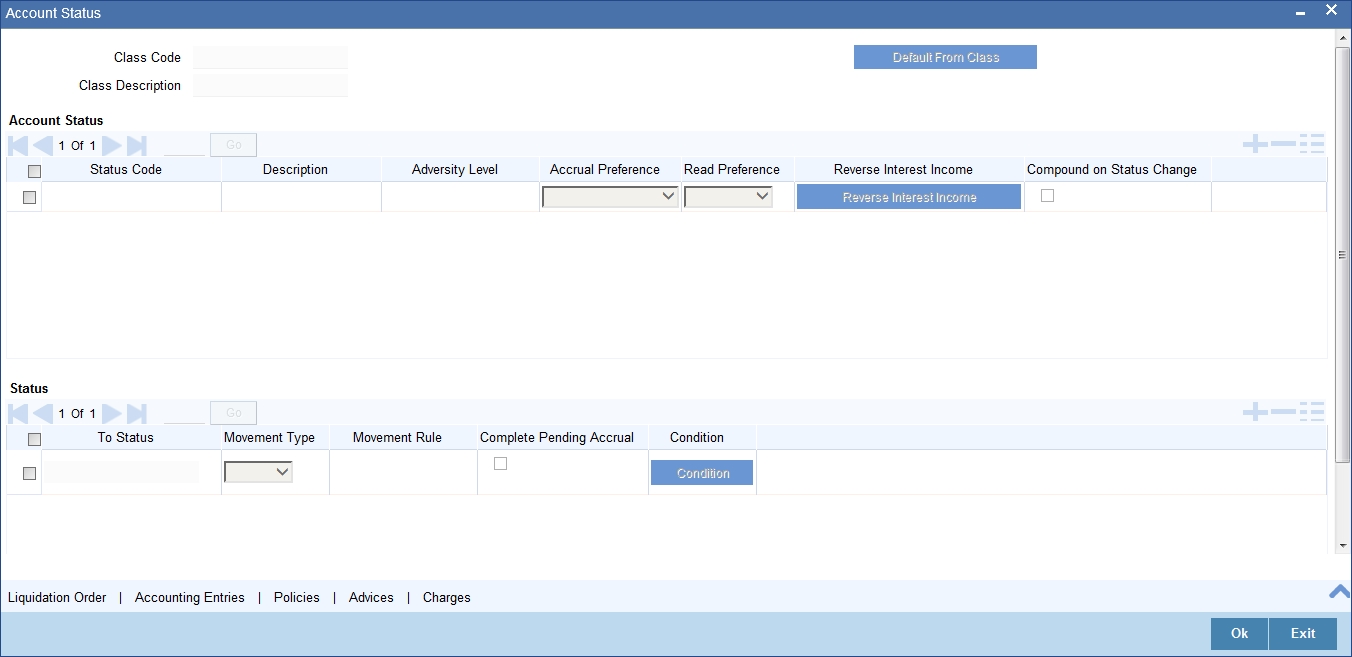

- Section 4.1.9, "Specifying Account Status "

- Section 4.1.10, "Maintaining Event Details"

- Section 4.1.11, "Maintaining Customer Category Restriction"

- Section 4.1.12, "Defining User Defined Fields "

- Section 4.1.13, "Specifying Top up Details"

- Section 4.1.14, "Viewing Mortgage Product Summary "

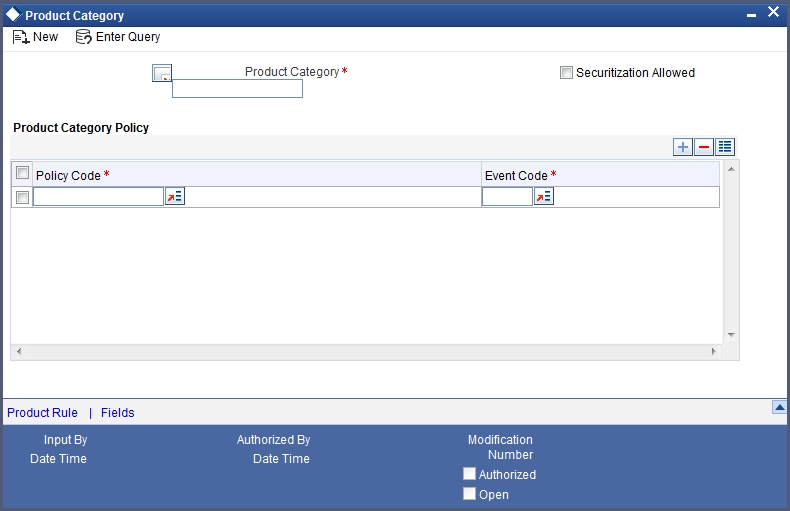

4.1.1 Maintaining Product Categories

You can define the attributes for a Product Category in the ‘Product Category’ screen.

You can invoke this screen by typing ‘CLDPRCMT’ in the field at the top right corner of the Application tool bar and clicking on the adjoining arrow button.

The following details have to be captured in this screen:

Product Category

You have to specify the name of the mortgage service which will identify the category uniquely in the system. For example: Home Mortgage, Vehicle Mortgage etc. The category name can consist of a maximum of 20 alphanumeric characters. The categories maintained through this screen become available for creating products under it (in the ‘Consumer Lending Product’ screen).

Product category is mandatory to save the record in the system.

Policy Code and Event Code

To the category being defined, you have to associate a policy code. The policies maintained in the ‘User Policy’ screen are available in the option-list provided.

You have to associate an event code to each policy selected. Whenever the event is triggered, the associated policy gets executed.

4.1.2 Setting up a Mortgages Product

As mentioned at the beginning of this chapter, within a category you may have mortgages that differ in amount, tenor or other preferences.

These may be categorized into products. The mortgage product is derived from the product category based on the product rule that it satisfies.

Product Categories and Products are created at the Head Office (HOB) and you can create accounts under the products at branch level.

The branches that can offer the products are further determined by the branch restrictions defined for the products.

You can capture product details in the ‘Product Maintenance’ screen.

You can invoke this screen by typing ‘MODPRMNT’ in the field at the top right corner of the Application tool bar and clicking on the adjoining arrow button.

In this screen, you can enter basic information about a product such as the Product Code, the Description, etc.

Specify the following details:

Product Code and Description

The code you enter for a product identifies it throughout the module. You can follow your own conventions for devising the code. However, it must have a minimum of four characters.

When defining a new product, you should enter a code. This code is unique across the CL modules of Oracle FLEXCUBE. For instance, if you have used VA01 for a product in this module, you cannot use it as a product code in any other module.

You should also enter a brief description of the product. This description will be associated with the product for information retrieval.

Product Type

Select the type of consumer Lending product that you are creating. The options available are:

- Mortgage – Select this option if you want to create a mortgage product

- Commitment – Select this option if you want to create a commitment product

Product Category

Products can be categorized into groups, based on the common elements that they share. For example Vehicle Mortgages, Personal Mortgages, Home Mortgages, and so on. You must associate a product with a category to facilitate retrieval of information for a specific category.

The categories defined through the ‘Product Category Maintenance’ are available in the option-list provided.

Product End Date

A product can be defined to be active for a specific period. When you create a product, you specify an End Date for it. The product can only be used within the specified period i.e. within the Start Date (the date on which the product is created) and End Date.

If you do not specify an end date for a product, it can be used for an indefinite period and the product becomes open-ended in nature.

Remarks

When creating a product, you can enter information about the product intended for your bank’s internal reference. This information will not be printed on any correspondence with the customer.

Slogan

You can enter a marketing punch line for every product you create. This slogan will be printed on all advices that are sent to customers who avail of the product.

4.1.3 Defining Other Attributes for a Product

After specifying the basic details of a product, you can define the other finer attributes for a product in the appropriate sub-screens provided. From the ‘Mortgage Product’ screen, you can move to the sub-screen of your choice to define these details. Click on the buttons provided at the bottom of the screen for this purpose.

Each buttons is explained briefly in the table below:

Button Name |

Description |

User Date Elements |

To define the UDEs and Components relating to the product |

Preferences |

To indicate your preferences specific to the product |

Components |

To specify the component details, schedule definition and formulae for the product |

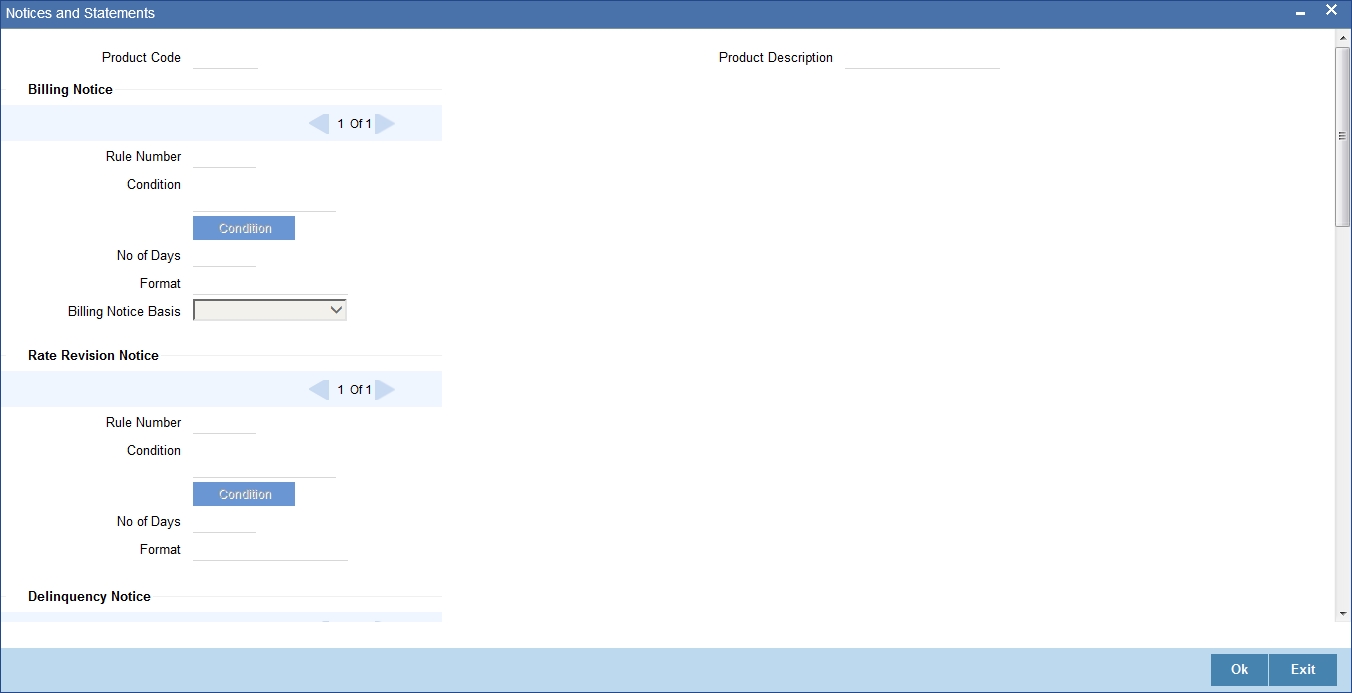

Notices and Statements |

To specify details of account statements and notices to be issued to customers. These have to be generated for different events in the life cycle of a loan |

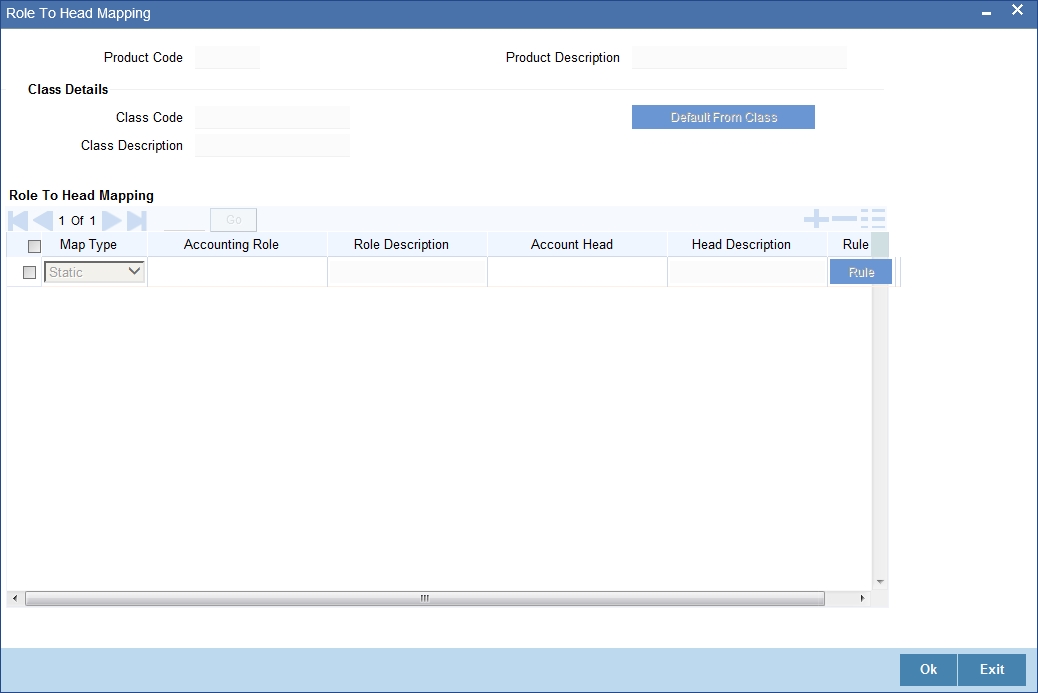

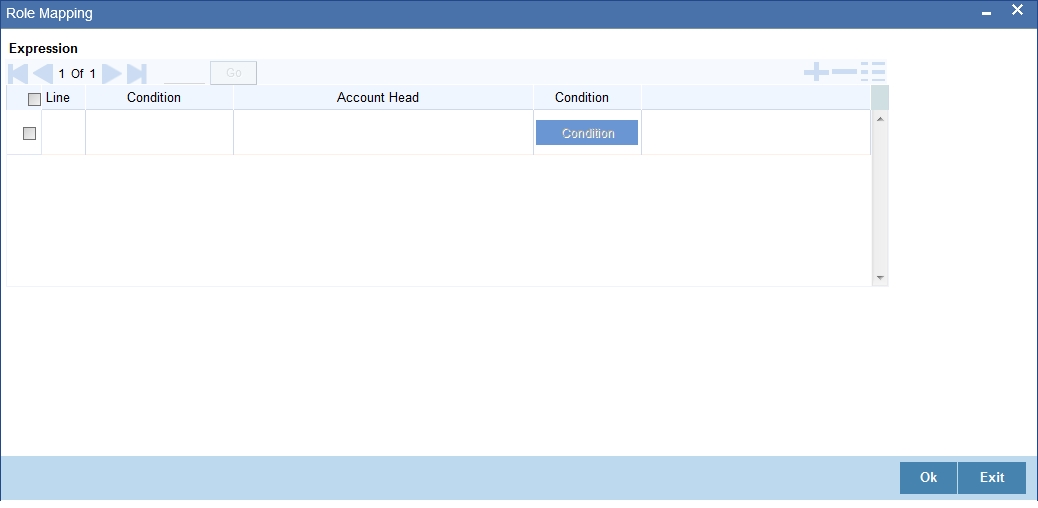

Role to Head |

To specify accounting roles and account heads for the product. (The concept of accounting roles and heads is explained later) |

Account Status |

To indicate the status preferences for the product |

Events |

To specify events |

Branch/Currency Restriction |

To define the branch and currency restrictions for the product |

Customer Category Restriction |

To Define the Customer Category Restrictions and Customer Access Restrictions for the Product |

Fields |

To associate User Define Fields (UDFs) i.e. Character Fields, Number Fields and Date Fields, with the product |

Minimum Amount Due Method |

To define the MAD formula for OLL product |

Product Fields |

To define Product fields |

MIS |

To define MIS details |

Note

There are some fields in the product definition screens, to which input is mandatory. If you try to save a product without entering details in these fields, the product will not be saved.

When you save a product that you have created, your user-id will be displayed in the ‘Input By’ field and the date and time at which you saved the product in the ‘Date/Time’ field. The Status of the product will be updated as ‘Unauthorized’. A product is available for use only after it has been authorized by another user.

4.1.4 Specifying User Data Elements

You can capture the user data elements details of a product by clicking the ‘User Data Elements’ button. The screen is displayed below:

The main details include the definition of ‘Used Data Elements and Components

To define a User Data Element (UDE), you have to specify the following details:

User Data Elements ID and Description

Data elements like the rate at which interest has to be applied, the tier structure based on which interest needs to be computed etc. are called User Data Elements (UDEs). These are, in effect, elements for which you can capture the values. You have to specify a unique ID to identify the UDE in the system. For instance, you can have a UDE ‘SUBSIDY_RATE’ to indicate the rate to be used for calculating the subsidy interest amount. The UDE maintained here will be available for defining product rules.

You can also provide a brief description of the UDE being defined.

User Data Elements Type

UDE Type will describe the nature of the UDE. An UDE can fall into one the following types:

- Amount

- Number

- Rate

- Rate Code

Rate Basis

Select the rate basis from the drop down list. The list displays the following values:

- Null

- Per Month

- Per Annum

User Data Elements Ccy

If the UDE type is ‘Amount’, you should specify the currency of the UDE. The currencies maintained in the ‘Currency Definition’ screen are available in the option-list provided. You can select a currency from this list.

Minimum User Data Elements Value

You need to specify the floor limit for the UDE value. This means that the actual UDE value cannot be less than the rate specified here. Note that this amount has to be less than the maximum UDE value. The system will throw an error message if the minimum UDE value is greater than the maximum UDE value.

Maximum User Data Elements Value

You need to specify the ceiling limit for the UDE value. This means that the actual UDE value cannot be greater than the rate specified here. Note that this amount has to be greater than the minimum UDE value. The system will throw an error message if this value is less than the minimum UDE value.

The UDE names alone are captured here. To capture the values for the UDEs defined for a product, you have to use the ‘UDE Values’ screen.

Refer the section titled ‘Providing UDE Values’ in the ‘Maintenances and Operations’ chapter of this User Manual for more details.

Rate Change Restricted

On checking this option, the system validates if the changes done to the UDE is done during rate plan change window. If this field is unchecked, then the system will not put any restriction on the amendment of the UDE based on rate plan change window.

Note

System will validate that either all the parameters for rate plan change is input or every parameter is null at the time of product input/amendment.

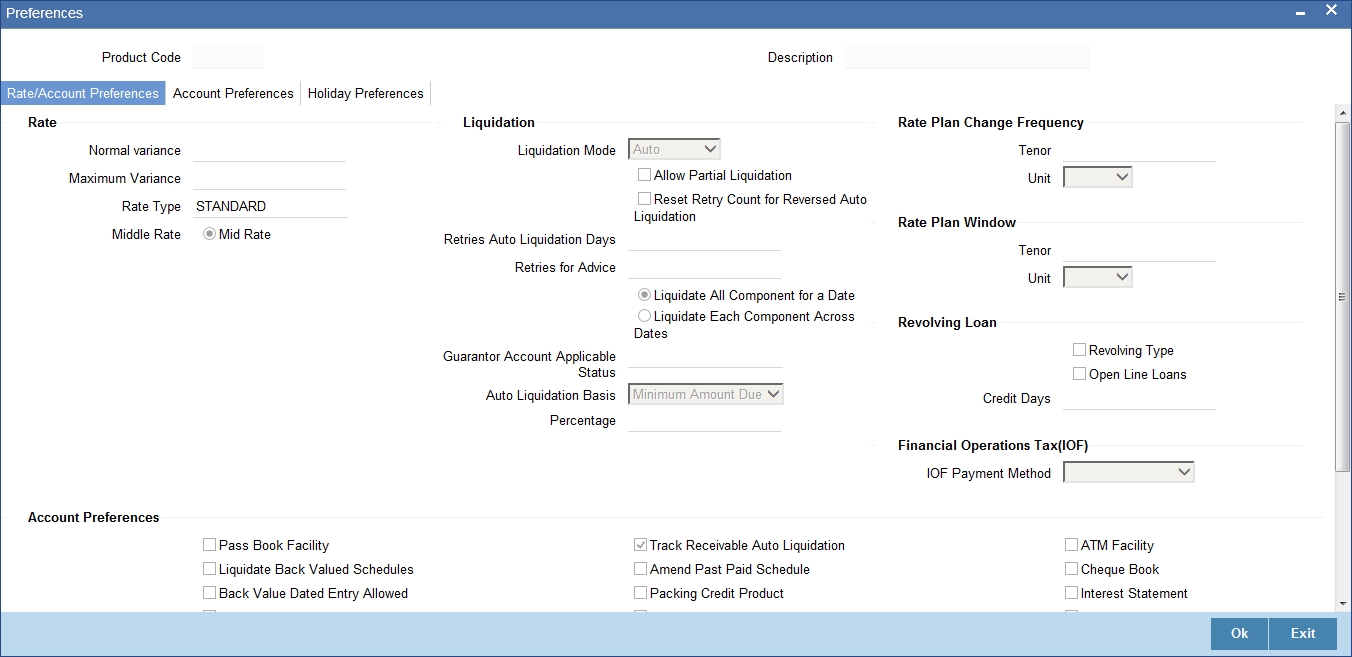

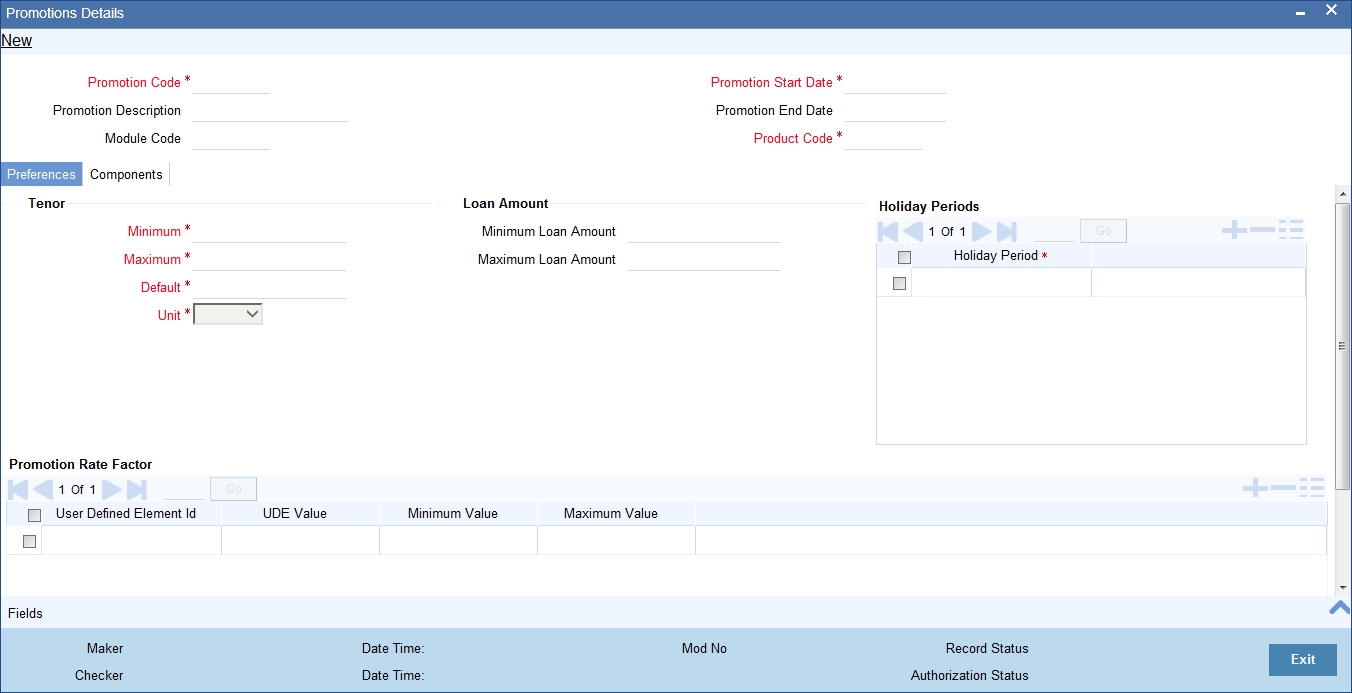

4.1.5 Indicating Preferences for a Product

Preferences are the options that are available to you for defining the attributes of a mortgage account product. These could be:

- The manner in which the system should handle schedules falling due on holidays

- Whether rollover should be automatic or with user intervention (manual)

- The tenor details for the mortgage

- Whether receivables should be tracked for the mortgage account etc.

The options you choose, ultimately, shape the product. These details are used for mortgage account processing.

Click ‘Preferences’ button in the ‘Product Definition’ screen.

You should maintain the following preferences for the mortgage product:

4.1.5.1 Rate/Account Preferences Tab

The exchange rate preferences include the following:

Rate

You have to indicate the exchange rate applicable for the product you are maintaining. The available options are:

- Mid Rate

- Buy/Sell Rate

By default, the Buy/Sell Rate is used.

Rate Type

You have to select the code that should be used for the product from the option list provided. The ‘Rate’ and ‘Rate Type’ are used in combination to determine the actual rate applicable for currency conversion.

The default value for Rate Code is ‘STANDARD’. This means that, if you choose ‘Mid Rate’, the mid rate maintained for the STANDARD code is used for the mortgages created under the product.

Maximum Variance

When creating a product, you can capture the maximum limit for rate variance. This is expressed in percentage. The variance between the exchange rate (specified for the product) and the rate captured for a mortgage (at the account level) should not be greater than the value specified here. If the exchange rate exceeds the maximum variance that you have defined for the product, the system will not allow you to save the mortgage. The transaction is rejected.

This value should be greater the value for ‘Normal Variance’.

Normal Variance

You also need to specify the minimum/normal variance allowed for the rate. If the exchange rate variance between the exchange rate (specified for the product) and the rate captured for a mortgage exceeds the value specified here, the system will display an override message before proceeding to apply the exchange rate. The normal variance should be less than the maximum variance.

For back valued transactions, the system applies the rate on the basis of the exchange rate history. The variance will be based on the rate prevailing at that time.

Account Preferences

As part of specifying the account preferences, you can indicate the following:

Amend Past Paid Schedule Allowed

This option, if checked, allows you to perform value dated amendments to interest rate, installment amount etc with effective date beyond the last paid schedule. In such a case, the increase/decrease in the interest amount, as a result of the amendment, will be adjusted against the next available schedule after the current system date (date on which the amendment was performed) even if unpaid (overdue) schedules are present for the mortgage.

Back Period Entry Allowed

This option facilitates back valued transactions. If you select this option, you will be allowed to process transactions with a value date less than the current system date.

Interest Statement

You have to select this option to facilitate interest statement generation for the account.

Liquidate Back Valued Schedules

If you select this option, on initiation of a back value dated mortgage, all the schedules with a due date less than the system date will be liquidated.

Special Interest Accrual

If you check this box, accrual of interest is done on the basis of the formula specified for a component. Otherwise, interest accrual will be done based on the number of days in the schedule.

CL Against Bill

Check this box if you want this Mortgages product to be used for mortgages against an export bill. By default this is not checked.

Note

You are allowed to link multiple mortgages against one bill.

Product for Limit

Check this box to indicate that the product is for limits. If you check this option, the product will be available for limits linkage during line creation.

Packing Credit product

Check this box to indicate the possibility of linking CL Accounts to BC when you create them with this product.

Schedule Basis

You should also specify the schedule basis for the rolled over mortgage. The new mortgage can inherit the schedules from the mortgage product or you can apply the schedules maintained for the original mortgage itself.

Rate Plan Change Frequency

You can change the rate plan frequency of a mortgage account in the ‘Preferences’ button of the Product screen.

Tenor

Specify the amount of time to be given to the customer for rate change plan option..

Unit

Select the unit for the specified tenor from the drop-down list. The following options are available for selection:

- Monthly

- Yearly

Rate Plan Window

Tenor

Specify the amount of time that the customer can take to decide on the ‘rate plan’ and intimate the bank about the decision.

Unit

Select the unit for the rate plan tenor from the drop-down list. The following options are available for selection:

- Monthly

- Yearly

Liquidation Preferences

Liquidation preferences include the following:

Liquidation Mode

You can specify the mode of liquidation from the drop-down list. The following options are available for selection:

- Auto

- Manual

- Component

Partial Liquidation

In case of insufficient funds in the account, you can instruct the system to perform partial auto liquidation to the extent of funds available in the account. However, if this option is not selected, the schedule amount due will not be liquidated if sufficient funds are not available in the account.

Reset Retry Count for Reversed Auto Liquidation

If you have maintained a limit on the number of retries for auto liquidation, this option will reset the retries count to zero during reversal of auto liquidation. This will be applicable from the date of reversal of payment. Hence, the system will once again attempt auto liquidation till the number of retries allowed. The system will update the status of the reversed payment to ‘Unprocessed’ after which it again attempts auto liquidation.

Retries Auto Liq Days

Capture the number of working days for which the system should attempt auto liquidation. The number of retries per day will depend on the configuration maintained for the ‘Liquidation Batch Process’ - during BOD, EOD or both. For instance, if the batch is configured for both EOD and BOD, and the number of retry days is ‘1’, then, auto liquidation is attempted twice on the same day i.e. once during BOD and another retry at EOD.

Retries for Advice

Specify number of times you want to retry generation of advice. The number of retries should be less than ‘Retries Auto Liquidation Days’. When auto liquidation fails and advice retry count is reached, the system generates a failure advice and sends it to the customer to initiate an appropriate action for the successful execution of the advice.

Financial Operations Tax (IOF)

The following options are available to specify financial operations tax:k

IOF Payment Method

Select the IOF payment method from the drop down list. The list displays the following values:

- Advance Payment

- Capitalization - This is allowed only for Simple/Amortized reducing loans.

- Null

The default value will be Null.

Note

- The payment method can be defined at product level only. It cannot be modified after first authorization.

- If the IOF payment method is not null, then it is mandatory to have a IOF component. IF a IOF component is linked to a CL product, then method selected cannot be null

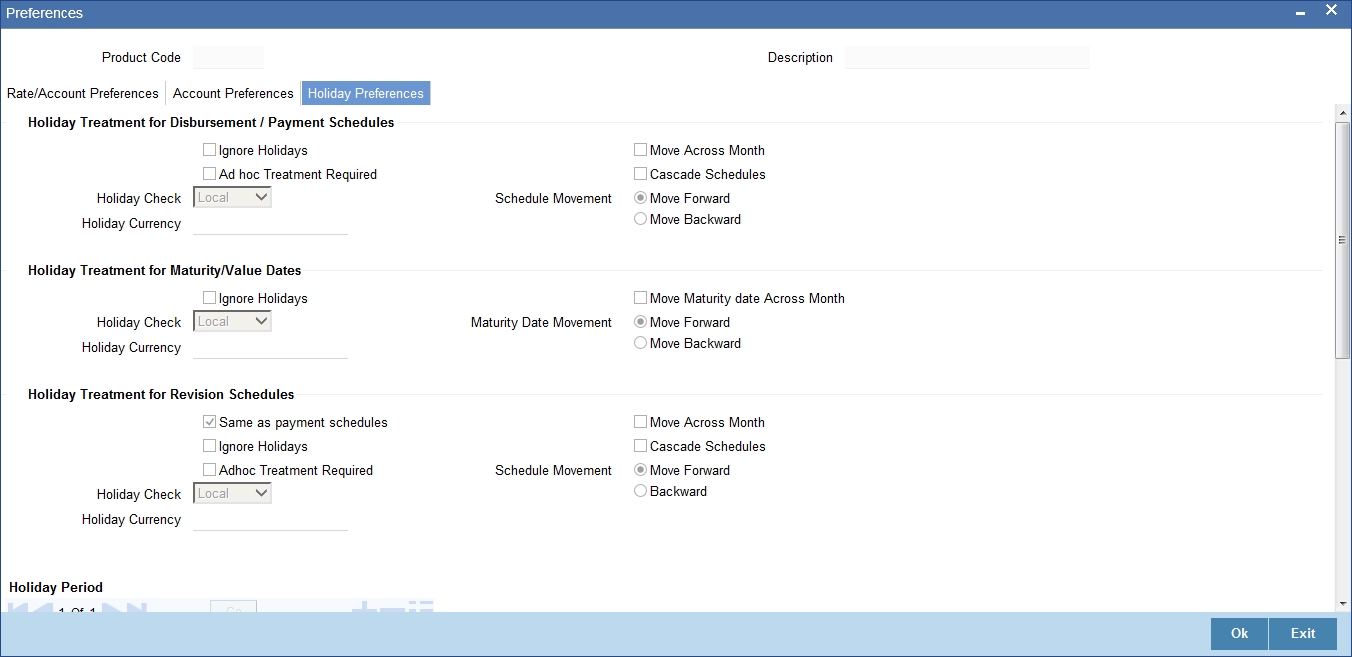

4.1.5.2 Holiday Preferences Tab

The value date, schedule date, revision date or the maturity date of a contract might fall on a local holiday defined for your branch or on a holiday specified for the currency involved in the contract.

Note

The holiday preferences are not applicable for call type of loans

In this tab you can specify the holiday parameters for the following schedules:

- Holiday Treatment for Disbursements/Payment Schedules

- Holiday Treatement for Maturity/Value Dates

- Holiday Treatment for Revision Schedules.

The parameters which can be defined are as following:

Ignore Holidays

If you check this option, the schedule dates will be fixed without taking the holidays into account. In such a case, if a schedule date falls on a holiday, the automatic processing of such a schedule is determined by your holiday handling specifications for automatic processes, as defined in the ‘Branch Parameters’ screen.

Adhoc Treatment Required

Check this option to allow the movement of due dates of the revision schedules that fall on the newly declared holidays.

Note

This option is enabled only if the options, ‘Ignore Holidays’ parameter and ‘Cascade Schedules’ parameter are not checked.

Cascade Schedules

If you check this option, when a particular schedule falls due on a holiday and hence is moved to the next or previous working day (based on the ‘Branch Parameters’), the movement cascades to other schedules too. If not selected, only the affected schedule will be moved to the previous or next working day, as the case may be, and other schedules will remain unaffected.

For example, assume that you have opted to move holiday schedules to the next working day and a schedule falling due on 29th April is moved to 30th April, 29th being a holiday.

The schedule date for May depends on whether you have chosen to cascade schedules. If you have, chosen to cascade schedules, the schedule date for May will be set as 30th May, since the frequency has been specified as monthly. All subsequent schedules will be moved forward by a day.

If you have not specified that schedules have to be cascaded, the date originally specified will be the date for drawing up the remaining schedules. Even if you move the April schedule from 29th to 30th, the next schedule will remain on 29th May.

However, when you cascade schedules, the last schedule (at maturity) will be liquidated on the original date itself and will not be changed like the interim schedules. Hence, for this particular schedule, the interest days may vary from that of the previous schedules.

Move Across Month

If you have chosen to move the schedule date of a mortgage falling due on a holiday, either to the next or previous working day and the movement crosses over into a different month, then this option will determine whether the movement should be allowed or not.

Holiday Check

Select the holiday check option from the drop down list. The options available are:

- Null- To apply No holiday check.

- Local - To apply holidays based on branch holiday calender.

- Currency - To apply holidays based on Currency holidays.

- Both - To apply both Currency and Branch holidays.

By default the system selects the value as ‘Local’.

Holiday Currency

Specify the holiday currency. Alternatively, you can also select the holiday currency from the adjoining option list. The list displays all valid currencies maintained in the system.

Note

You need to maintain holiday currency only if ‘Holiday Check’ is either ‘Currency’ or ‘Both’.

Maturity Date Movement – Forward /Backward

If you opt to move the maturity date falling due on a holiday across months, you need to specify whether the maturity date should be moved forward to the next working day in the following month or moved backward to the previous working day of the current schedule month itself.

Schedule Movement – Forward /Backward

If you opt to move the schedule date falling due on a holiday across months, you need to specify whether the schedule date should move forward to the next working day in the following month or move backward to the previous working day of the current schedule month itself.

However, if you opt to ignore the holidays and do not select the ‘Move Across Months’ option, the system Ignores the holidays and the due will be scheduled on the holiday itself.

Same as Payment Schedule

Check this box to ignore the holiday preference maintained for revision schedule and use the same holiday preferences maintained for Disbursement /Payment schedule. By default this box is checked.

Note

This option is available only for Holiday Treatment for Revision Schedules. If selected, the system ignores any holiday parameters maintained for it and considers only those maintained for Disbursement/Payment schedules

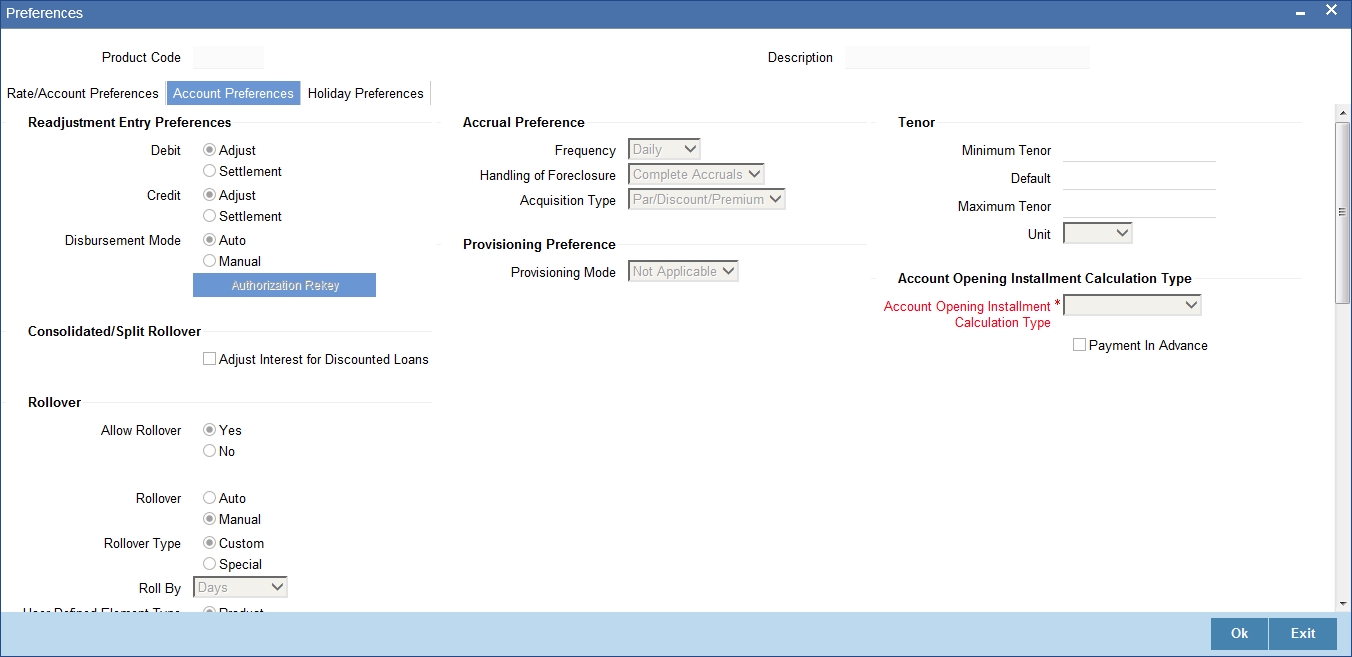

4.1.5.3 Account Preferences Tab

The rollover specifications for a mortgage account will apply to all mortgage accounts opened under the product.

Auto/Manual Rollover

You have the option to rollover the mortgage manually or instruct the system to do an automatic rollover. If you choose the do an auto rollover, then upon maturity of the mortgage, the system will automatically rollover the account.

The rollover will happen as part of the Rollover Batch executed at BOD or EOD, depending on your requirement.

Rollover Type

The following options are available:

- Custom: This determines if the Rolled over amount will include the unpaid components of the product. The option list provided will display the components relevant to the product from which you can choose the components that are to be rolled over.

- Special: Choose this option to indicate that a special amount is to be rolled over. The amount is captured at the account level when the actual rollover is initiated.

Rollover By

This is applicable if you have opted for automatic rollover. You have to specify the unit based on which Rollover will be triggered. The options are:

- Days

- Months

- Quarters

- Semi Annuals

- Years

UDE Type

Here, you need to specify whether UDE Values for the new (rolled over) mortgage should be defaulted from the product or from the original mortgage account/contract that is being rolled over.

Disbursement Mode

The following options are available to make a disbursement:

- Auto - Choose this option to instruct the system for automatic disbursal of mortgage. In this case, disbursement happens based on the disbursement schedule maintained for the product. This is defined in the ‘Components’ button. By default, the system does an auto disbursal.

- Manual – Choose this option to manually disburse the mortgage.

Here, disbursement happens on demand. In this case, disbursement schedules

need not be maintained for the PRINCIPAL component.

The ‘Manual Disbursement’ screen is used for this purpose.

For details, refer the ‘Making Manual Disbursements’ chapter of this User Manual.

Prepayment preferences for amortized mortgages

The following are the preferences based on which prepayment of amortized mortgage should be processed:

Recomputation Basis

Recomputation of amortized mortgages as a result of a prepayment can be based on one of the following:

- Recalculate Installment Amount: In this case the tenor remains constant.

- Recalculate Tenor: Here, the tenor is recomputed while the installment remains constant.

Prepayment Installment Calculation Type

For Prepayment of amortized mortgages, if you have chosen to recompute the Installment Amount keeping the tenor constant, then the Installment calculation can be one of the following types based on future rates:

- Single Installment: A single installment is computed using the future rates.

- Multiple Installments: Multiple EMIs are defined if a future rate change is known upfront.

While giving the UDE values, effective dates can be given based on which the UDE values will become applicable.

Let us say a mortgage is sanctioned on 1.1.2008. The rate of interest is as follows:

- UDE value Effective date is 01.11.2007 - 10%

- UDE Value effective date is 01.04.2008 - 11%

If the option chosen is ‘Multiple installment’ then based on the UDE values, EMI will be calculated depicting a higher EMI from 1.4.2008 at the new rate of interest. So, when ever a prepayment happens it will take into effect the two rates and calculate two different EMIs for these periods.

Prepayment Effective From

You can choose the date on which the prepayment should become effective. The prepayment can come into effect from the value date of the current installment (the day on which the payment is made) or the Next Installment.

Minimum EMI Amount

You can enter the minimum amount that has to be paid as EMI after recomputing the EMI. The recalculated EMI after prepayment should be greater than this amount.

Minimum EMI Ccy

You can enter the currency of the EMI amount to be paid.

Notary Confirmation Required

You can check this box to indicate that the product is a mortgage product that requires confirmation from the notary for disbursing the mortgage.

Partial Block Release

Check this box to indicate whether the partial release of term deposit should be done as part of loan repayment.

Interest Only Period

Specify (in numbers) the duration for which the customer needs to repay only the interest component. This period thereby indicates a holiday period for principal repayment.

Unit

Select the unit of period to be considered for the interest holiday, from the adjoining drop-down list. This list displays the following values:

- Days

- Weeks

- Months

- Years

Note that in Oracle FLEXCUBE, one month is equal to 30 days.

Provisioning Preference

You can define the provisioning preference of loan accounts by selecting the required option in Provisioning Mode.

Provisioning Mode

Select the Provisioning Mode preference of loan accounts from the drop-down list. The list displays the following options:

- Not Applicable

- Auto

- Manual

By default, the provisioning mode will be selected as 'Not Applicable'.

It is mandatory to select the provisioning mode as either ‘Auto’ or ‘Manual’ if CL product is created with a provision component. If CL product does not have provision component, then provisioning mode should be selected as 'Not Applicable'.

Tenor Preferences

You can set the minimum and maximum tenor limits for a product. You can also specify a standard or a default tenor.

Minimum Tenor

You can fix the minimum tenor of a product. The tenor of the mortgage account that involves the product should be greater than or equal to the Minimum tenor that you specify.

Maximum Tenor

Likewise, you can also specify the maximum tenor for a product. The tenor of the mortgage accounts that involve the product should be less than or equal to the Maximum tenor that you specify.

Default Tenor

The ‘default tenor’ is the tenor that is associated with a mortgage account involving this product. The value captured here should be greater than the minimum tenor and less than the maximum tenor. You can change the default tenor applied on a mortgage account during mortgage processing. However, the new tenor should be within the minimum and maximum tenors maintained for the product.

Units

The tenor details that you specify for a product can be expressed in one of the following units:

- Days

- Months

- Year

Recomputation of Amortization Mortgage at Amendments

You have to indicate whether the tenor of the mortgage should be reduced or the installment should be recalculated whenever a maturity date, principal change or a rate change is made against an amortized mortgage.

Recomputation basis for amendments

The possible amendments and the recomputation basis are given below:

- For amendment of maturity date of an amortized mortgage: You can opt to change the tenor, keeping the installment constant..

- For amendment of principal amount: You can affect it either as a Balloon additional amount in the last schedule or apportion it across the installments

- For interest rate change: You can change the tenor keeping the installment constant or vary the EMI and keep the tenor same.

VAMI Installment Calculation Type

For amendments, if the recomputation basis is ‘Change Installment’, then the Instalment calculation can be:

- Single Installment

- Multiple Installment based on multiple future rates

Account Opening Installment Calculation Type

The Account Opening Installment Calculation Type based on future rates can be:

- Single Installment: A single installment is computed using the future rates.

- Multiple Installments: Multiple EMIs are defined as per the future rates.

Readjustment Entry Preferences

You have to specify the manner in which adjustment entries passed due to back dated adjustments should be handled. The options are:

- Settlement: This means that the adjustment is settled directly

- Adjust: In this case, the entries are tracked as a receivable (Cr) or a payable (Dr), to be settled later

4.1.5.4 Prepayment Penalty Component

An SDE, ‘CUR_PREPAID_AMOUNT’ defines the formula of the prepayment penalty component. This indicates the prepaid amount for the current year. This SDE picks its value from CLTB_LIQ_PREPAID table. ‘CUR_PNLTY_COLLECTED’ is an SDE that indicates the prepayment penalty already collected for the financial year. ‘CUR_PRINCIPAL_OUTSTND’ is an SDE that defines the formula of the prepayment penalty component. This indicates the principal outstanding amount at the beginning of the current year.

You can use the following formula to base the ceiling percentage on original disbursement amount:

CUR_PREPAID_AMOUNT>(MAX_PREPAID_PCT*AMOUNT_DISBURSED/100)

You can use the following formula to base the ceiling percentage on the opening principal outstanding amount for the current year:

CUR_PREPAID_AMOUNT>(MAX_PREPAID_PCT*CUR_PRIN_OUTSTND/100)

The result of the above formulae is as follows:

(CUR_PREPAID_AMOUNT-(MAX_PREPAID_PCT*AMOUNT_DISBURSED/100))*(PREPAY_RATE/100)-(CUR_PNLTY_COLLECTED)

After the collection of pre-payment penalty, if there is any additional disbursement to the customer which leads to the increase in limit of the prepaid amount, system will not pass on the benefits back to the customer. However, for subsequent calculations the disbursed amount and the pre-payment penalty paid till date for the financial year is considered based on the formula defined. If SDE ‘CUR_PRINCIPAL_OUTSTND’ is the basis for calculation, the additional disbursement will not be considered in calculation for current year. It is used for calculation only from next year onwards.

4.1.5.5 Calculating NPV Difference

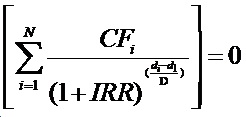

In case of early repayment of mortgages (partial or full), the following method is followed for penalty calculation:

Let us assume that, X% of the total mortgage amount can be paid in one year. Penalty is applicable on anything above X%. This penalty is the difference between the NPV of existing cash flows of the mortgage being paid and the NPV of the cash flows post-prepayment application. Both the NPVs are based on current yield curve i.e. yield rate supplied. This penalty can also be based on percentage of amount being overpaid.

A UDE, ‘YIELD_RATE’ is used for the calculation of penalty based on NPV of current cash flows of mortgage and NPV of new cash flows post-prepayment.

An SDE, XNPV computes the NPV value based on the current cash flows and future cash flows (i.e. post-prepayment application) respectively.

The formula for calculating NPV is as follows:

CUR_PREPAID_AMOUNT > MAX_PREPAID_PCT * PRINCIPAL

The formula above can be used to base the ceiling percentage on original disbursement amount.

You can use the following formula to base the ceiling percentage on the opening principal outstanding amount for the current year:

CUR_PREPAID_AMOUNT > MAX_PREPAID_PCT * CUR_PRINCIPAL_OUTSTND

The result of the formula is as follows:

@XNPVDIFF (XNPV, YIELD_RATE)

Result of the formula can be some percentage of the difference of the NPV as shown below:

@XNPVDIFF (XNPV, YIELD_RATE) * 0.05

The computation of pre-payment penalty is done by the system at the time of allocate. Internally system applies the pre-payment and gets the future schedules. Subsequently, based on the formula defined for XNPVDIFF, system finds the difference between the NPV based on the yield rate and populates the same against the pre-payment penalty component.OLE_LINK2OLE_LINK1OLE_LINK2OLE_LINK1

Note

Penalty based on NPV is supported by the system only when product is amortized.

4.1.5.6 Re-key Preferences

As a cross-checking mechanism to ensure that you are invoking the right mortgage for authorization, you can specify that the values of certain fields should be entered, before the other details are displayed. The complete details of the mortgage will be displayed only after the values to these fields are entered. This is called the re-key option. The fields for which the values have to be given are called the re-key fields.

You can specify the values of a mortgage that the authorizer is supposed to key-in before authorizing the same.

If no re-key fields have been defined, the details of the mortgage will be displayed immediately once the authorizer calls the mortgage for authorization.

The re-key option also serves as a means of ensuring the accuracy of the data captured.

4.1.5.7 IRR Accrual Preferences

If IRR computation is applicable for the product that you are defining, you need to specify the accrual preference for the same. You can do this through the Accrual Preference part of the preferences screen.

Accrual Frequency

Specify the frequency at which IRR accrual should be performed. This can be either Daily or Monthly. Choose the appropriate option from the adjoining drop-down list.

Handling of foreclosure

Specify how foreclosures in respect of the mortgage contracts under the product, must be handled. You can opt for complete accruals or refund. Choose the appropriate option from the adjoining drop-down list.

Note

In case of pre-closure of the mortgage (prepayment of the total outstanding amount), the fund interest will also get liquidated and thus the accrual entries will get reversed.

Acquisition Type

Specify the acquisition type for the product. You can specify any of the following options:

- Par

- Par/Discount

- Par/Premium

- Par/Discount/Premium

Refer the section titled ‘Processing of IRR application on mortgages’ in this chapter to understand the IRR processing for this module.

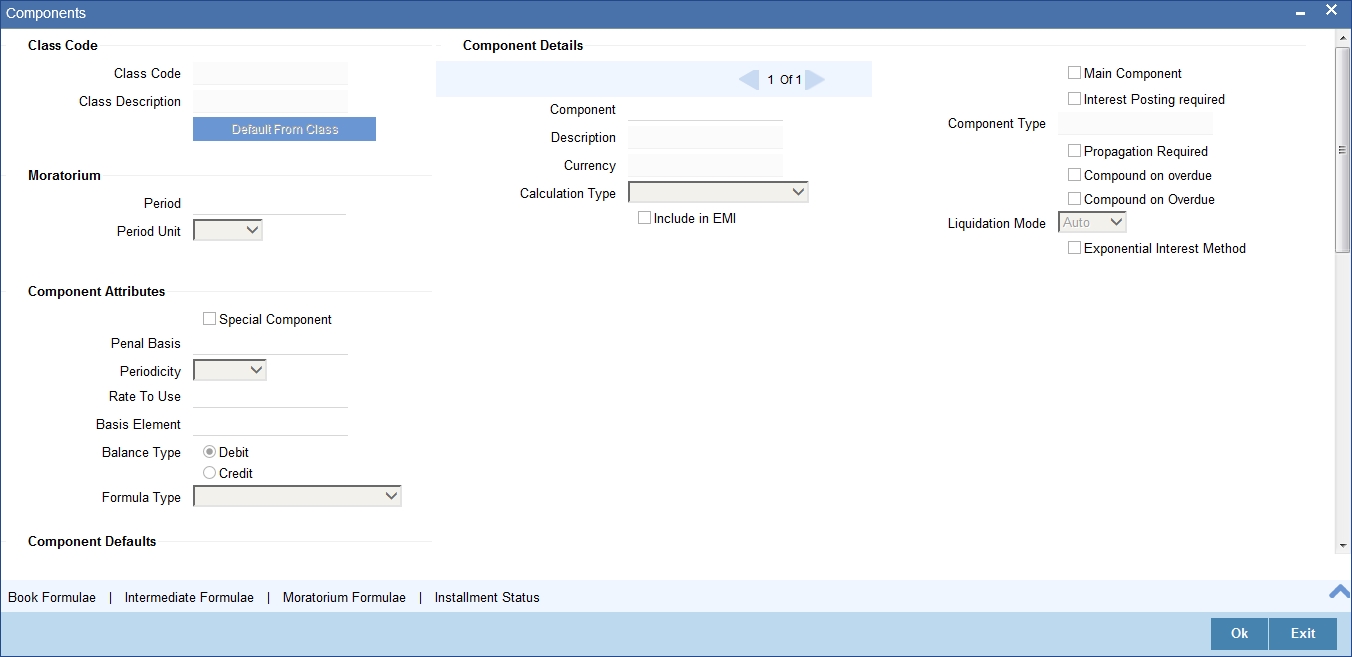

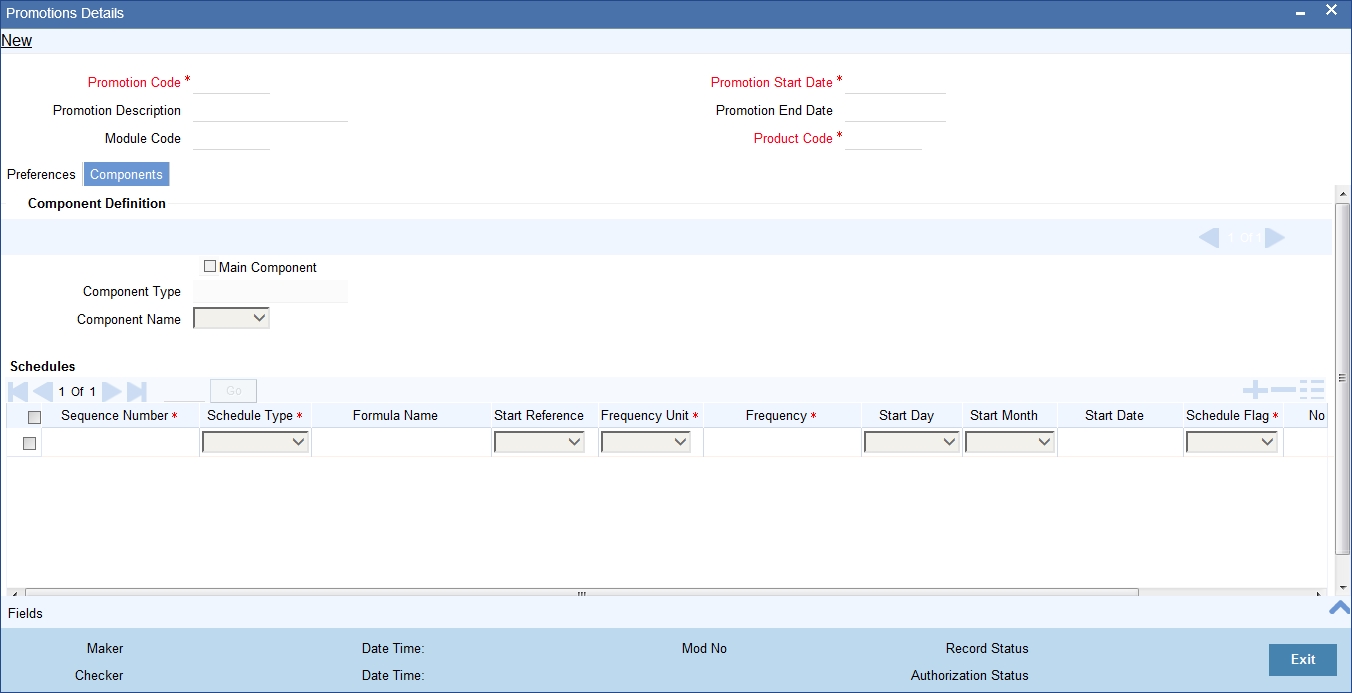

4.1.6 Specify Components Details

You can define the features of the components in the ‘Components’ screen. Invoke this screen by clicking ‘Components’ button. The following screen displays:

Specify the following details:

Class Code

Select a class code from the adjoining option list. The option list displays all the valid classes maintained in the system. One class can have multiple components defined. The system attaches all the components to the product on clicking ‘Default from Class’ button

On authorizing a component class, system will create the required accounting roles and amount tags.

Component Details

The basic information for a component is specified here. This includes the following:

Component

The Component which is selected in the list appears in Component field. For e.g. ‘PRINCIPAL’, ‘INTEREST’, ‘PENALTY’ ‘PROV’ etc. Subsequently, you have to define the parameters for these components in the ’Component’ button of the screen.

For Commitment products, the MAIN_INT component is used for defining periodic fees on the unutilized commitment amount.

Currency

Associate the component with a currency. The component is expressed in the currency selected here. You can select the currency of your choice from the option list provided.

Calculation Type

Specify the manner in which the component should be calculated and liquidated. You can choose one of the following options (the applicable ‘Component Type’ is also provided):

- Formula with schedule (Component Type - Interest)

- Formula without schedule (Charge)

- Penal Interest

- Prepayment Penalty

- Discount

- Schedule without formula (Principal)

- No schedule No formula (Ad Hoc Charges)

- Penalty Charges

- Savings

- Financial Operations Tax (IOF)

Note

- ‘Penalty Charges’ are calculated only once for a ‘Penal Basis’ schedule. ‘Penal Basis’ is explained later in this user manual.

- The component ‘Savings’ is used for interest calculation

on the value dated balance of the savings account. This component needs

to be defined as simple interest component with its basis element as

‘CUSTAC_BAL’, and rate to use as ‘INTEREST_RATE’.

Formula for this component is given below:

@SIMPLE (CUSTAC_BAL, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE) - Select the option in ‘Calculation Type’ as ‘No Schedule No Formula’ for adhoc type component.

Main Component

This option is used to designate a component as the ‘Main’ Interest component. If you enable the ‘Main Component’ option for a particular component, the system treats this component as the main component. Also, you are allowed to define the amortization schedules only for this component.

‘Principal’ is an implicit component that is automatically created for the product

Capitalization

You can indicate whether capitalization is required for all the schedules for various component of the mortgage. At anytime, the outstanding interest will be capitalized on the schedule date at the rate prevalent on that day. You can opt for capitalization at the component level or opt for capitalization/non capitalization for a particular schedule at the ‘Schedule’ level.

You could have more than one type of schedules applicable on a product. In such a case, you can designate one as the capitalized and the other as un-capitalized schedule.

Description

The Description of the component which is defined in Main button for the component will appear in this field once you select the component in component list.

Component Type

Indicate the nature of the component. This is also known as the ‘Reporting Type’. It defines the manner in which the component should be classified for reporting/accounting purposes. A component can be of one of the following types:

- Reimbursement: these are components which have both Dr and Cr mapped to settlement accounts

- Off-Balance Sheet (OBS): An OBS Component will have balances but these need not be zero when an account is closed

- Fund Interest: This indicates the funding component

- Ad hoc Charges

- Charge

- Tax

- Insurance

- Interest

- Provisioning

- Deposit

Note

The fund interest component gets liquidated on schedule even if the customer does not pay the other components.

During EOD, provisioning event is triggered for all mortgage accounts linked to a customer whenever you modify the credit rating of a customer at the customer level. Provisioning amount is calculated based on the formula maintained for the Provisioning Component at the Product level. During EOD batch, PROV event is picked and processed for all the mortgage accounts for which PROV event is to be triggered. As a part of end of day batch accounting entries are passed for the calculated provision amount.

Even though the credit rating changes at customer level, the Provision event will not be triggered for accounts belonging to that CL product level, if the following maintenances are not done:

- Provisioning component maintenance at product level

- Provisioning event (PROV) maintenance at product level

- If Accrual frequency is daily at product level

Exponential Interest Method

Check this box for the system to validate the following for exponential interest method calculation:

- COMPOUND_VALUE SDE is maintained in book formula

- Compound days is maintained as one.

Refer the section ’Calculating Exponential Interest for Loans’ in chapter ‘Account Creation’ of this User Manual for more details on processing loans using the exponential interest method

Propagation is required

Check this option to indicate that the interest amount collected from the borrower should be passed on to participants.

Compound On Overdue

Check this box to compound the interest/penalty interest when it is overdue.

Note

- This check box can be checked only for a single interest and penalty components.

- If you check this box, then the system compounds the overdue interest or penalty computed till the last compounding date, to the principal.

- If this check box is checked and a component schedule is overdue, then the system triggers re-computation on the compounding dates and compound the overdue/penal interest on that date.

Liquidation Mode

You can specify the mode of liquidation of the component from the drop-down list. The following options are available for selection:

- Auto

- Manual

Note

This is applicable only if ‘Liquidation mode’ is selected as ‘Component’ at the product preference level.

Component Attributes

The component attributes include the following:

Periodicity

The periodicity of the component can be either:

- Daily

- Periodic

If you choose the periodicity as ‘Daily’, any changes to UDE and SDE values will result in recalculation of the component. The recalculation happens as and when a change in value occurs. If maintained as ‘Periodic’, the values and calculations of the elements will be refreshed on the last day of the period.

In case of a product having main and subsidy interest components, the schedule periodicity needs to be identical for both components.

Special Component

You can define a component as a ‘Special Interest Component’. You can override such components at the account level. You may need to apply a special interest component as a result of customer negotiations. A special interest component is specified as an amount.

Formula Type

You can specify the type of formula to be used for calculating the component. This formula is applied for the component across all its’ schedules. It can be one of the following:

- User Defined: This can also include a combination of standard formulae for different schedules of the component or can have a completely user defined formula.

- Standard

- Simple

- Amortized Rule of 78

- Discounted

- Amortized Reducing

- True Discounted

- Rate Only

You can choose the option ‘Amortized Reducing’ for subsidy component.

Note

- This is not applicable for the ‘PRINCIPAL’ component

- For a commitment product, the formula type cannot be ‘Amortized’, ‘Discounted’ or ‘Simple’

Penal Basis

You may want to allot the penalty to the recovery of certain components. Once a component is overdue, an appropriate penalty is applied. Therefore, you need to identify the component, which on becoming overdue will trigger the penalty computation. However, the system will calculate the penalty on the component you select in the ‘Basis Element’ field.

Note

For commitment products ‘PRINCIPAL’ is not used for penal basis and for basis amount. In case of EMI products, instalment amount is used for calculating the penalty.

Balance Type

Identify the nature of the balance that the component would hold. This can be represented through this field. For instance, for a mortgage product, the ‘Principal’ component is expected to have a ‘Debit’ balance.

Basis Element

If you select the ‘Standard’ formula type, you have to specify the component upon which calculation should be performed. The component is denoted by an SDE (e.g. PRICIPAL_EXPECTED) and you can select it from the option list provided. For an overdue/penalty component, this is the element on which penalty is applied.

This is not applicable if ‘Formula Type’ is ‘User Defined’

Rate to Use

Here, you need to select the UDE which will define the rate to be used for computing the component. The value of the selected UDE is picked up as per the maintenance in the ‘UDE Values’ screen. For instance, you need to choose the option ‘SUBSIDY_RATE’ for a subsidy interest component.

This is applicable only for components defined with ‘Standard’ Formula Type

Note

The ‘Basis Element’ for computing fund interest will always be ‘Principal Outstanding’ and the ‘Formula Type’ will be ‘Simple’, independent of the main interest component. The liquidation mode for funding component will always be ‘Auto’, independent of the Product / Account Liquidation mode.

Moratorium Preferences

The following parameters have to be specified:

Moratorium Period and Period Units

If you wish to provide a moratorium on a mortgage, you need to mention the moratorium period and moratorium unit for each component. This refers to a repayment holiday at the beginning of the mortgage. When you input a mortgage in Oracle FLEXCUBE, the repayment start date of each component will be defaulted based on your specifications here. The moratorium unit should be in terms of:

- Days

- Months

- Years

Computation Defaults

For computing interest, you have to specify the following:

Days in Year

You can specify the number of days to be considered for a year during computation of a particular component. This could be:

- 360: This means that only 360 days will be considered irrespective of the actual number of calendar days

- 365: In this case, leap and non leap year will be 365

- Actual: In this case, leap year will be 366 and non leap year will be 365

This value corresponds to the denominator part of the interest method

Days in Month

Here, you have to specify the number of days to be considered in a month for component computation. The options available are:

- Actual: This implies that the actual number of days is considered for calculation. For instance, 31 days in January, 28 days in February (for a non-leap year), 29 days in February (for a leap year) and so on

- 30 (EURO): In this case, 30 days is considered for all months including February, irrespective of leap or non-leap year

- 30 (US): This means that only 30 days is to be considered for interest calculation for all months except February where the actual number of days is considered i.e. 28 or 29 depending on leap or non-leap year

The value selected here corresponds to the Numerator part of the Interest method

Interest Method Default from Currency Definition

You also have the option to use the interest method defined for the currency of the component. In this case, the interest method defined in the ‘Currency Definition’ screen (for the component currency) will become applicable to the mortgage. By default, this option is checked.

Grace Days

The grace days refer to the period after the repayment date, within which the penalty interest (if one has been defined for the product) will not be applied, even if the repayment is made after the due date. This period is defined as a specific number of days and will begin from the date the repayment becomes due. However, if the customer fails to repay even within the grace period, penalty will be applied and calculated from the repayment due date.

However, in case a penalty charge is defined for a penal basis component under a retail lending product, the ‘Grace Days’ is defined as part of itself. The schedule due date for the penalty charge is then computed by adding the ‘Grace Days’ to the corresponding schedule due date of the penal basis component.

IRR Applicable

Check this option to indicate that the chosen component needs to be considered for Internal Rate of Return (IRR) calculation. This option is applicable to interest, charge, adhoc charge, prepayment penalty, penalty and upfront fee components.

Note

This option should not be checked for Commitment products.

If a charge component is to be considered for IRR, the charge will be accrued using the FACR (Upfront Fee Accrual) batch.

The following components cannot be considered for IRR calculation:

- Off-balance sheet component

- Provision component

If you check this option, then you have to check the ‘Accrual Required’ option.

For bearing type of component formula, you can check this option only if the ‘Accrual Required’ option is checked.

For discounted or true discounted types of component formula, this option will be enabled irrespective of the whether the ‘Accrual Required’ option is checked or not. If this option is checked and ‘Accrual Required’ is not, the discounted component will be considered as a part of the total discount to be accrued for Net Present Value (NPV) computation. If both ‘Accrual Required’ and ‘IRR Applicable’ are checked, then discounted interest will be considered for IRR computation.

Verify Funds

You can indicate whether the system should verify the availability of sufficient funds in the customer account before doing auto liquidation of the component.

Accruals/Provisioning/Interest Payback

To perform accrual of the components, you have to capture the following details:

Required

You can use this option to indicate that the component has to be accrued and provisioning is applicable. For the components that have been marked for accrual, you need to specify the accrual frequency, start month and start date in the respective fields.

‘Required’ check box should be checked for interest payback component.

Note

If the ‘Calculation Type’ is ‘Penalty Charges’ for a component, the ‘Accrual Required’ option is disabled.

Accrual Frequency

If you have opted for accrual and provisioning for the components, you have to specify the frequency for the same. The frequency can be one of the following:

- Daily

- Monthly

- Quarterly

- Half yearly

- Yearly

The frequency for interest payback component should not be selected as daily.

Accrual Start Month

If you set the accrual/provisioning frequency as quarterly, half yearly or yearly, you have to specify the month in which the first accrual has to begin, besides the date.

Accrual Start Date

In the case of monthly, quarterly, half yearly or yearly frequencies, you should specify the date on which the accrual/provisioning has to be done. For example, if you specify the date as ‘30’, accruals will be carried out on the 30th of the month, according to the frequency that you have defined.

Start month and start date are not applicable for interest payback component if the component type is Interest Payback.

Prepayment Threshold

This includes the threshold amount and currency, explained below:

Amount

Here, you can maintain the minimum limit for allowing prepayment of schedules. If the residual amount after prepayment against a schedule is less than the threshold amount you specify here, the system will disallow the prepayment.

Currency

If you specify the threshold amount, you also have to indicate the currency in which the amount should be expressed. You can select the currency from the option-list provided.

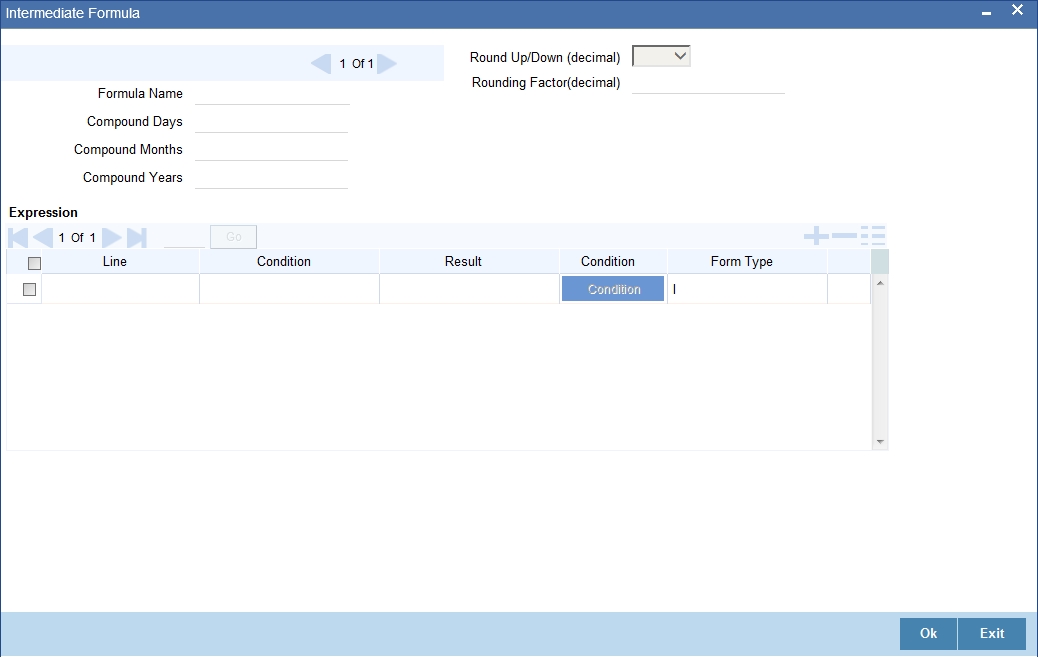

4.1.6.1 Intermediate Formula

Intermediate Formulae are used as building blocks for more complex formulae. An intermediate formula is used to create a Booked/Moratorium formula as an intermediate step. It will not be associated directly to any schedule.

To define an intermediate formula, click ‘Intermediate’ in the ’Components’ button of the screen. The ‘Intermediate Formula - Expression Builder’ screen is displayed.

Formula Name

Specify a suitable name to identify the formula that you are defining. After you specify the name you can define the characteristics of the formula in the subsequent fields. You have to use the name captured here to associate a formula with a schedule. The name can comprise of a maximum of 27 alphanumeric characters.

Round Up To

If you want to round off the results of an intermediate formula, you can indicate the number of digits upto which the results should be rounded-off to. Compound Days/Months/Years

If you want to compound the result obtained for the intermediate formula, you have to specify the frequency for compounding the calculated interest.

The frequency can be in terms of:

- Days

- Months

- Years

If you do not specify the compound days, months or years, it means that compounding is not applicable

Rounding Factor

Specify the precision value if the number is to be rounded

It is mandatory for you to specify the precision value if you have maintained the rounding parameter.

Compound Days

If you want to compound the result obtained for the intermediate formula, you have to specify the frequency for compounding the calculated interest. The frequency can be in terms of days.

Compound Months

If you want to compound the result obtained for an intermediate formula, you have to specify the frequency for compounding the calculated interest. The frequency can be in terms of months.

Compound Years

If you want to compound the result obtained for an intermediate formula, you have to specify the frequency for compounding the calculated interest. The frequency can be in terms of years.

Condition and Result

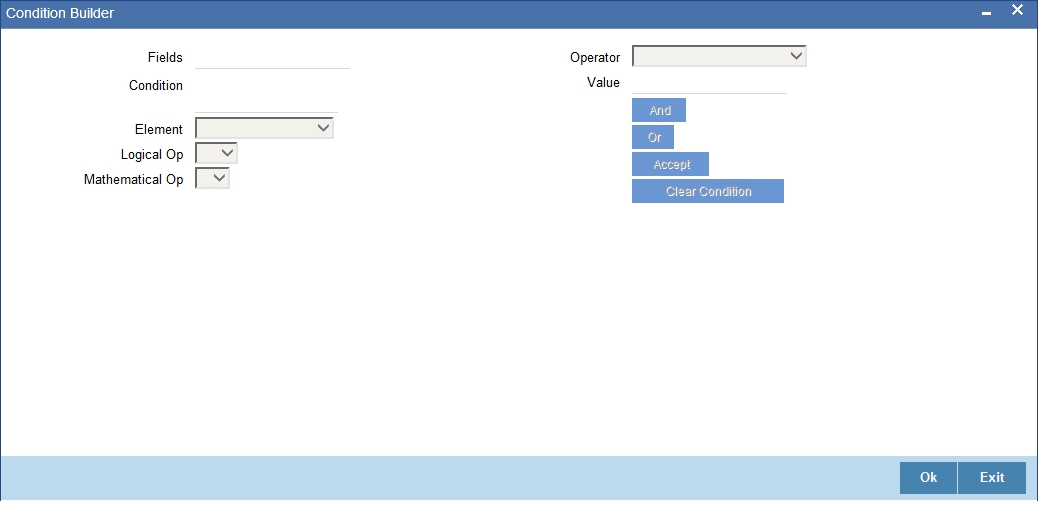

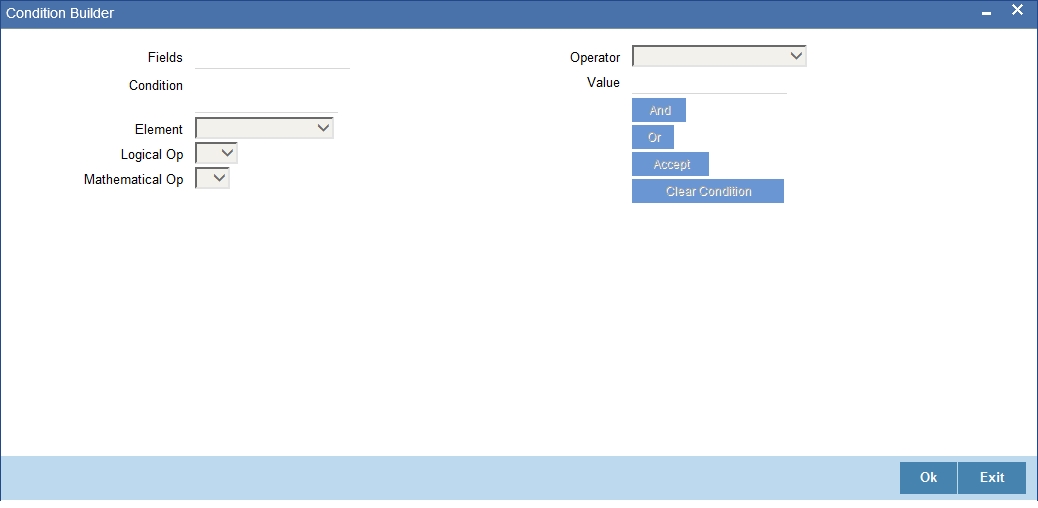

A formula or calcualtion logic is built in the form of expressions where each expression consists of a ‘Condition’ (optional) and a ‘Result’. There is no limit to the number of expressions in a formula. For each condition, assign a unique sequence number/formula number. The conditions are evaluated based on this number. To define a condition, click on ‘Condition’ in the screen above. The following screen is displayed:

In this screen, you can use the elements, operators, and logical operators to build a condition.

Although you can define multiple expressions for a component, if a given condition is satisfied, subsequent conditions are not evaluated. Thus, depending on the condition of the expression that is satisfied, the corresponding formula result is picked up for component value computation. Therefore, you have the flexibility to define a computation logic for each component of the product.

The result of the formula may be used as an intermediate step in other formulae.

4.1.6.2 Using Intermediate Formulae for Amortized Mortgages

You can use intermediate formula in the interest components of amortized mortgage mortgages. To enable this, you need to select the UDE ‘Z_INTRMDT_RATE’ against the field ‘Rate to Use’.

Further, you can set an intermediate formula with a combination of multiple UDEs in the ‘Result’ field. For example, you may specify the following formula:

INTEREST_RATE + MARGIN_RATE

This implies that the result is the sum of two user defined elements viz. ‘INTEREST_RATE’ and ‘MARGIN_RATE’. You may also define different formulae based on the conditions set. Intermediate formulae support the following mathematical functions:

- Plus (+)

- Minus (-)

- Multiplication (*)

- Division (/)

Based on requirements, you may define and set various formulae using the above mathematical functions.

The system calculates the value of the UDE ‘Z_INTRMDT_RATE’ based on the intermediate formula defined. This calculation is handled in the system generated package. Apart from ‘Z_INTRMDT_RATE’, the system will not allow you to define a UDE that starts with ‘Z_’.

Oracle FLEXCUBE uses the following formats to display the derived interest rate:

Formats |

MO_AMD_ADV |

MO_LOAN_DETAIL |

MO_CONTR_STMT |

MO_UDE_ADVC |

MO_RTCH_ADV |

4.1.6.3 Booked Formula

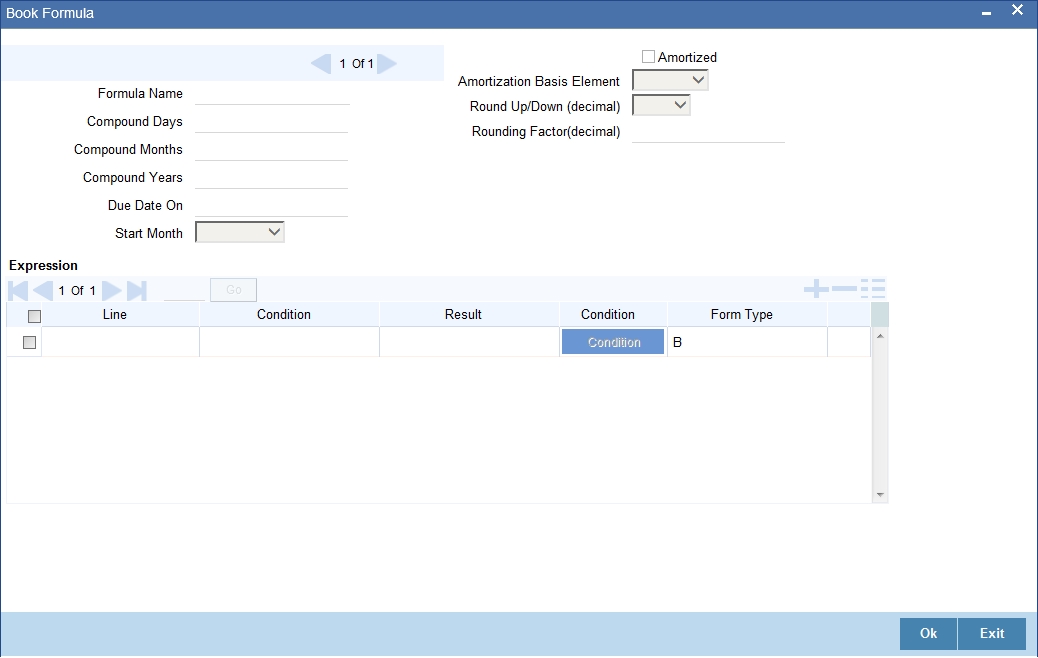

Booked Formula refers to the formula used to compute a component value for a particular schedule. You can use intermediate formulae to create a ‘Booked’ formula. To create the formula, click ‘Book’ in the ‘Component’ button of the screen. The following screen is displayed:

The SDEs available will be shown in the Condition Builder. You can use the relevant ones to build the formula. For instance, you need to use the SDE ‘TOTAL_SCHODUE’ in the formula to compute schedule amount for subsidy mortgage products. The Booked formula so created will be linked to a schedule.

The system uses few specific SDEs to compound the penalty interest on the compounding details. The SDEs and respective value are as follows:

SDE |

Value |

PRINCIPAL_EXP_AND_ODUE_COMP |

If there is compounding defined and is overdue past the subsequent compounding date that follows this schedule, this SDE returns the sum of principal expected for the schedule and the principal that is overdue. |

<COMPONENTNAME>_OVERDUE_COMP |

If there is no compounding defined, this SDE returns the total overdue for the component. If there is compounding defined, this SDE returns the total overdue for a component on a compounding date, and would return the total overdue for a component till the last compounding date, on non-compounding dates. |

<COMPONENT_NAME>_POST_MAT_ODUE |

This SDE returns the total overdue for the component post maturity date of the account. |

These are some of the examples of the formulae generated by the system on its own by choosing the formula type and the basis elements.

- Simple - @SIMPLE(PRINCIPAL_EXPECTED,(INTEREST_RATE),DAYS,YEAR,COMPOUND_VALUE)

- Amortized Reducing - @AMORT_RED(PRINCIPAL_EXPECTED,(INTEREST_RATE),DAYS,YEAR)

- Discounting - @DISCOUNTED(PRINCIPAL_EXPECTED,(INTEREST_RATE),DAYS,YEAR)

- Amortised Rule 78 - @AMORT_78(PRINCIPAL_EXPECTED,(INTEREST_RATE),DAYS,YEAR)

- True Discounted - @TRUE_DISC(PRINCIPAL_EXPECTED,(INTEREST_RATE),DAYS,YEAR)

- Stamp duty-

TOTAL_OUTSTANDING * STAMP_DUTY_RATE - Amortized Formula – Compound on overdue for main interest –

@AMORT_RED (PRINCIPAL_EXP_AND_ODUE_COMP + MAIN_INT_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

- Amortized Formula – Compound on overdue for penalty component –

@AMORT_RED (PRINCIPAL_EXP_AND_ODUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

- Amortized Formula – Compound on overdue for penalty component on principal and main interest –

@AMORT_RED (PRINCIPAL_EXPECTED + PEN_PRIN_COMPNAME_OVERDUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

@AMORT_RED (PRINCIPAL_EXP_AND_ODUE_COMP + PEN_PRIN_COMPNAME_OVERDUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

- Simple – Compound on overdue for main interest –

@ SIMPLE (PRINCIPAL_EXP_AND_ODUE_COMP + MAIN_INT_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

- Simple – Compound on overdue for penalty component –

@ SIMPLE (PRINCIPAL_EXP_AND_ODUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

- Simple – Compound on overdue for penalty component on principal and main interest –

@SIMPLE (PRINCIPAL_EXPECTED + PEN_PRIN_COMPNAME_OVERDUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

@SIMPLE (PRINCIPAL_EXP_AND_ODUE_COMP + PEN_PRIN_COMPNAME_OVERDUE_COMP + PEN_INT_COMPNAME_OVERDUE_COMP, (INTEREST_RATE), DAYS, YEAR, COMPOUND_VALUE)

The parameters required to create a ‘Booked’ formula are similar to the ones explained for an Intermediate formula.

The formula for calculation of ‘Provision Amount’ is defined based on the following conditions:

Line |

Condition |

Result |

1 |

CUSTOMER_CREDIT_RATING=”AAA” |

PRINCIPAL_OUTSTAND*0.0015 |

2 |

CUSTOMER_CREDIT_RATING=”AA+” |

PRINCIPAL_OUTSTAND*0.0025 |

3 |

CUSTOMER_CREDIT_RATING=”AA” |

PRINCIPAL_OUTSTAND*0.0035 |

4 |

CUSTOMER_CREDIT_RATING=”A+” |

PRINCIPAL_OUTSTAND*0.0045 |

5 |

CUSTOMER_CREDIT_RATING=”A” |

PRINCIPAL_OUTSTAND*0.0055 |

6 |

CUSTOMER_CREDIT_RATING=”BBB” |

PRINCIPAL_OUTSTAND*0.0065 |

7 |

CUSTOMER_CREDIT_RATING=”BB+” |

PRINCIPAL_OUTSTAND*0.0075 |

8 |

CUSTOMER_CREDIT_RATING=”BB” |

PRINCIPAL_OUTSTAND*0.0085 |

Amortized

Select this option to specify that the schedules of the component should be amortized

Note

For Commitment products do not select this option

Amortization Basis

If you opt to Amortize the schedules of the component, you have to identify the element based on which the component is amortized. For example, if it is deposit interest, the amortization basis would be ‘Principal’. The components are available in the option list provided.

In case of a subsidy mortgage, amortization is done with both the main interest and the subsidy component. For instance, if the interest rate is x% and the subsidy rate is y%, amortization will be done using net interest rate as x+y%, in the aforesaid scenario. The interest component will be calculated for the main interest and the subsidy component based on the principal expected and the individual rates for the components.

Due Date On

Specify day on which you need to compound the interest.

Start Month

Select month from which you need to compound the interest from the adjoining drop-down list. This list displays the names of the months in year.

Compounding Frequency

Suppose compounding should be processed on the 7th of every month, then the ‘Due Date On’ should be maintained as 7. If it is required that compounding should start from a specific month say March, then the Start Month should be maintained as 3. If the ‘Start Month’ or ‘Due Date On’ are not maintained, then the system will continue to compound based on the loan value date, for the given frequency (in days/months/years).

You can define compounding frequency for a component same as or lesser than its payment frequency, but if the compounding frequency is greater than its payment frequency then there will be no compounding.

For exponential loans, compounding frequency should be set as daily.

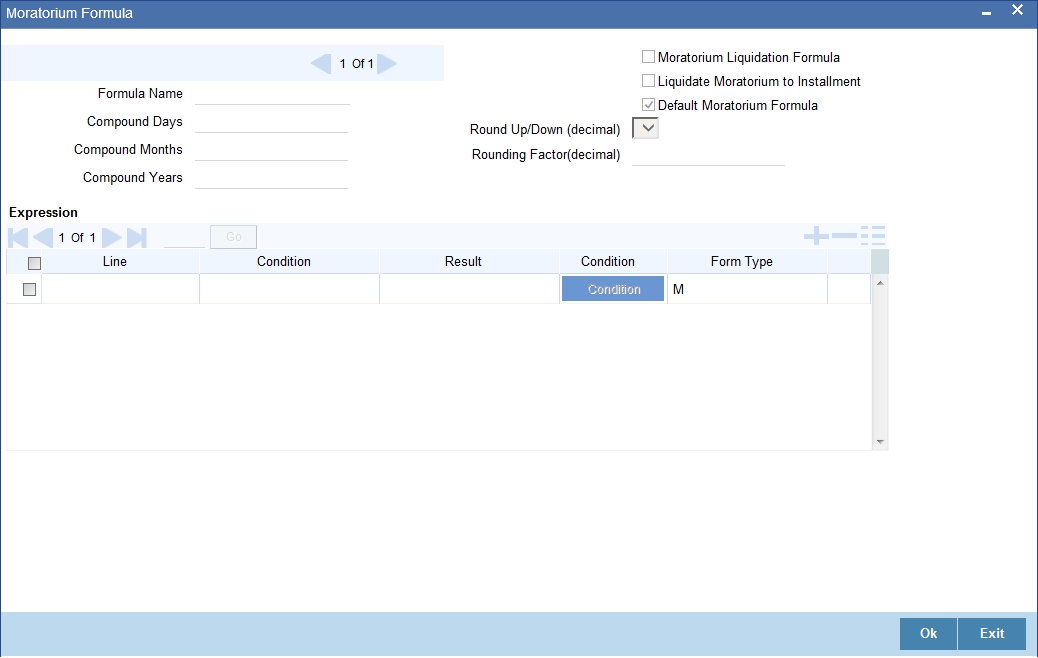

4.1.6.4 Moratorium Formula

Moratorium refers to the repayment holiday given during the period between the value date of the mortgage and the first repayment date. While no repayment will happen during this period, computation will continue. However, you can also have a principal moratorium wherein no principal repayment happens in a certain period; only interest component is repaid. This moratorium may be applied at any stage of the repayment cycle of the mortgage. In case of a principal moratorium, you need to ensure that the tenor given in the formula does not exceed the principal moratorium period. The Moratorium formula is used for the computation of interest for the moratorium period.

To define the formula, click ‘Moratorium’ in the ‘Component’ button of the screen. The ‘Moratorium Formula – Expression Builder’ screen is displayed:

The procedure for defining the Moratorium formula is as explained for Intermediate and Booked formulae. The following additional fields are also applicable for a moratorium formula:

Formula Name

Here, you specify a suitable name to identify the formula that you are defining. After you specify the name, you can define the characteristics of the formula in the subsequent fields. You have to use the name captured here to associate a formula with a schedule. The name can comprise of a maximum of 27 alphanumeric characters.

Moratorium Liquidation Formula

The formula used for computation of interest for the moratorium period is called ‘Moratorium Formula’. The Interest calculated using the moratorium formula should be liquidated for the lifetime of the mortgage by apportioning it across all the installments. Therefore, you need to maintain a formula for liquidating the moratorium interest.

Check this option to indicate that the formula you have maintained is for Moratorium liquidation.

Liquidate Moratorium to Installment

This option is applicable only if you are defining a ‘Moratorium Liquidation Formula’

If you check this option, the moratorium interest amount is added to the first installment amount and collected along with the schedule on the day the schedule falls due.

If you do not check this option, the moratorium amount is allocated from the Installment due. The principal component of the EMI is liquidated towards the moratorium. Therefore, Principal repayment does not begin until complete settlement of the moratorium amount.

Default Moratorium Formula

If you want to create a default moratorium formula, check this option. By default, the system will attach this formula to a moratorium schedule. You can, however, change it to a different moratorium formula.

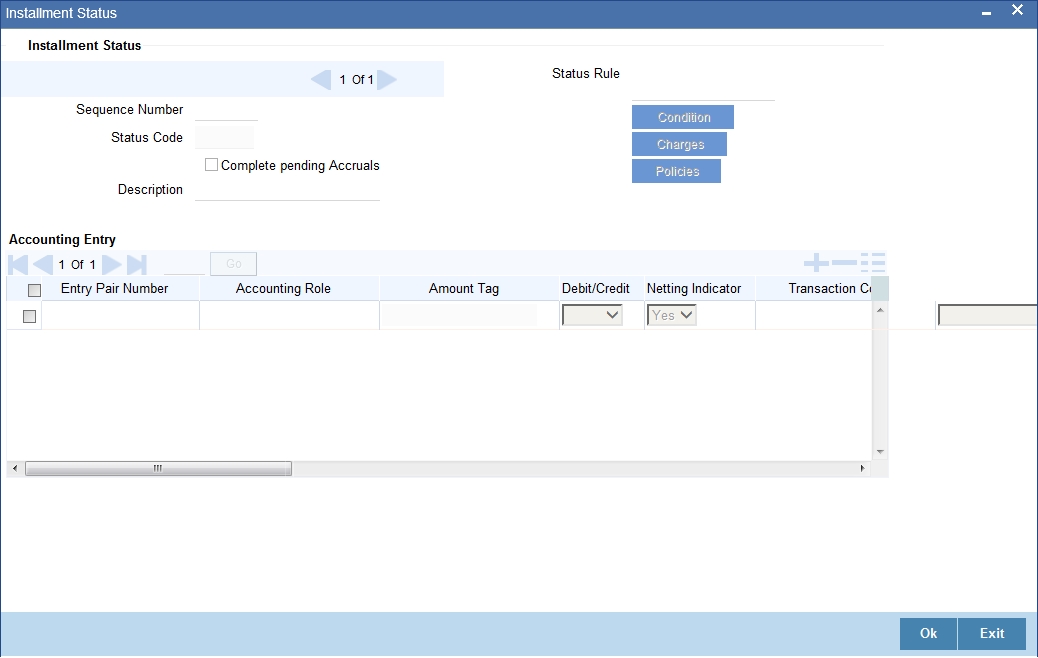

4.1.6.5 Installment Level Status

For a component, you can maintain Schedule/Installment level status change parameters. You can also specify the account Heads and Roles to be used whenever an installment changes from one status to the other.

To define the installment level status change details, click ‘Installment Status’ in the ‘Components’ button of the screen - the ‘Installment Status’ screen is displayed:

The following details have to be captured here:

Sequence Number

The number you capture here is used to identify the adversity level of an installment. It should not overlap with that of an account status, expect for the first factory shipped status ‘NORM’ (Normal).

Status Code

The status that an installment will go through is specified here. The sequence number determines the order when the installment would attain this status. The status codes defined in the ‘Status Codes Maintenance’ screen are available in the option-list provided.

Status Rule

The rule defined here will determine the movement of the installment to the selected status (in the ‘Status’ field). You can build multiple conditions for a rule.

To do this, click on ‘Condition’ in the screen above. The ‘Condition Builder’ is displayed.

You can build the conditions using the elements (SDEs), operators and logical operators available in the screen above.

Some examples of Status Movement Rules are given below:

- NORM TO PDO1 PRINCIPAL_OVR_DAYS > 30 OR MAIN_INT_OVR_DAYS > 30

- NORM TO DOUB PRINCIPAL_OVR_DAYS > 60 OR MAIN_INT_OVR_DAYS > 60

- PDO1 TO NORM PRINCIPAL_OVR_DAYS < 31 AND MAIN_INT_OVR_DAYS < 31

- PDO1 TO DOUB PRINCIPAL_OVR_DAYS > 60 OR MAIN_INT_OVR_DAYS > 60

- DOUB TO PDO1 (PRINCIPAL_OVR_DAYS > 30 AND PRINCIPAL_OVR_DAYS < 61) AND (MAIN_INT_OVR_DAYS > 30 AND MAIN_INT_OVR_DAYS < 61)

- DOUB TO NORM PRINCIPAL_OVR_DAYS < 31 AND MAIN_INT_OVR_DAYS < 31

For details on building a condition using the options available in the screen, refer the section titled ‘Defining UDE Rules’ in the ‘Maintenances and Operations’ chapter of this User Manual.

The installment will move to the status selected if the associated status rule is satisfied.

Complete Pending Accruals

Check this box to indicate if the pending interest accruals need to be completed before the Installment status changes. This is applicable only if Accrual Frequency is any one of the following:

- Monthly

- Quarterly

- Half yearly

- Yearly

This check box will not be enabled if Accrual Frequency in the ‘Consumer Lending Product’ screen is ‘Daily’.

Accounting Entries

For each status of the installment, you can specify the accounting entry preferences. Whenever an installment attains a status, the entries are passed as per the setup maintained for that status. Therefore, the entries will be moved from the active GLs to the status specific GLs. However, when the actual payment occurs, the system will automatically resolve the appropriate GLs.

For more details on setting up accounting entry preferences, refer the section titled ‘Maintaining Event details’ in this chapter.

Processing at Account Level

At the account level, when there is a change in the status, Oracle FLEXCUBE will first check if accrual is required for the components. When the accrual frequency for a component is not ‘Daily’, Oracle FLEXCUBE will validate if the installment status or the account status changes before accrual execution date. If it changes, Oracle FLEXCUBE will trigger catchup accrual for the component till the installment status and the account status change date. Subsequent to this, Oracle FLEXCUBE will process the installment status change and account status change.

Note

- An installment status change will not change the next execution date of unprocessed ACCR events

- A status change is applicable for both manual and automatic account status

- If you delete an account level status change, it will delete the catch up accrual accounting entries also

If you reverse an account level status change, it will reverse the catch up accrual accounting entries as well

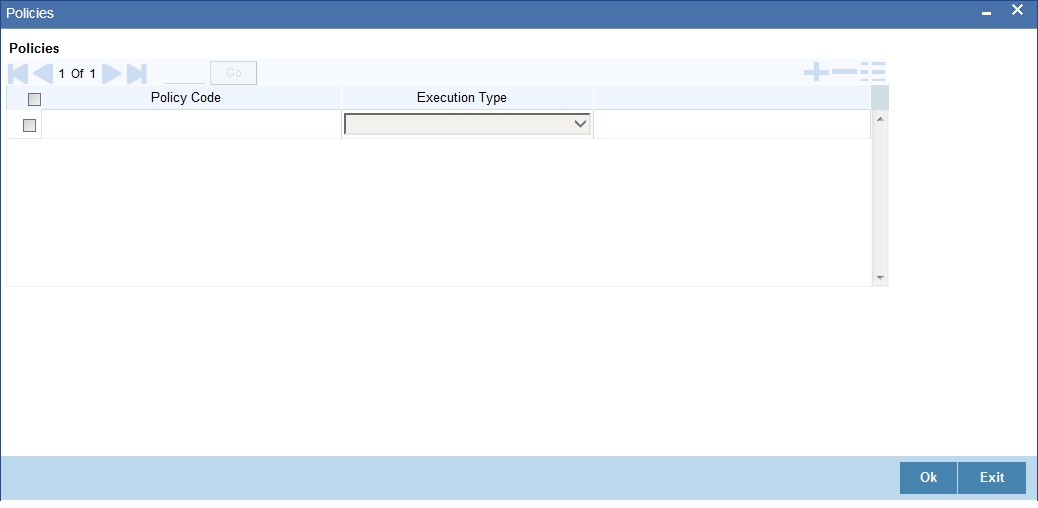

4.1.6.6 Specifying Policy Preferences

You can associate policies at an installment level. Policies are user defined validations that are fired when an event is triggered.

Policy Code

The Standard Policies (defined through the ‘Policy Maintenance’ screen) and the Policies associated with the product category are available in the option list provided. Policies are used to handle special validations and operations on a mortgage.

Execution Type

You can associate a policy at one of the following points in time in a mortgage -event lifecycle:

- Before Event

- After Event

- Both

The policy is executed appropriately.

For details on maintaining policy details, refer the section titled ‘Maintaining User Defined Policies’ in the ‘Maintenances and Operations’ chapter of this User Manual.

Schedule Preferences

In the ‘Component’ section of the screen, you need to maintain the applicable schedule details for each component:

Sequence Number

You can define more than one schedule for a component. The sequence number determines the order in which the individual schedule should be applied on a component. For instance, you can define a schedule structure consisting of a moratorium schedule and a normal schedule. The moratorium schedule, if defined for a component, should necessarily be the first schedule. You cannot have moratorium schedules in between normal schedules.

Type

This is the kind of schedule you want to define. The options are:

- Payment: This is used to define a repayment schedule. You can capitalize a payment schedule. If the ‘Capitalized’ option (under Component Definition) is checked, the ‘Capitalized’ option at the schedule level will also be checked for payment schedules. You can, however, uncheck/check this option for a schedule.

- Disbursement: You can maintain a disbursement schedule for mortgage disbursal if the ‘Disbursement Mode’ is automatic (this is maintained on the ‘Preferences’ button). For auto disbursement, you have to maintain at least one disbursement schedule.

- Rate Revision schedules: This will capture the schedule at which the rates applicable to the component should be revised.

Start Reference

This is used to capture the reference to arrive at the due date of the schedule. The options are:

- Calendar: If you select this option, you should also specify the ‘Start Date’ for the schedule. For example, if an account is created on 15th Sept with a ‘Monthly’ schedule frequency and the Start Date is 1st, then the schedule due dates would be 1st Oct, 1st Nov and so on.

- Value Date: If you select value date, the schedule due dates will be based on the Value Date of the account. For instance, if an account is created on 15th Sept and the schedule frequency is ‘Monthly’, then the schedule due date would be 15th October, 15th Nov and so on.

For a component, you can define schedules based on both value date and calendar date.

Frequency Unit

Here, you have to capture the unit to define the schedule. The unit can have the following values:

- Daily

- Weekly

- Monthly

- Quarterly

- Half Yearly

- Yearly

- Bullet

If the schedule unit is ‘Weekly’, you should also capture the ‘Start Day’. Similarly, for units ‘Quarterly’, ‘Half Yearly’ and ‘Yearly’, you should also specify the ‘Start Month’.

Frequency

This is used in combination with ‘Unit’ explained above, to define non-standard frequencies. For instance, a ‘Monthly’ unit and frequency 2 implies that the schedule is bi-monthly (occurring every two months).

Start Day

If the schedule unit is ‘Weekly’, you should specify the start day to initiate the schedule. The drop-down box lists the days of the week

Start Month

This is applicable if the schedule unit is one of the following:

- Quarterly

- Half Yearly

- Yearly

The drop-down box lists the months in a year

Start Date

Here, you can specify a value between 1 and 31. This is applicable if the schedule unit is ‘Monthly’

Due On

You can use this to define a schedule on a particular date of the month. A value between 1 and 31 can be used for this purpose. If you specify a value here, the system will build the schedules based on this date even if you have indicated the ‘Start Date’ for the schedule.

Formula

You have to select the formula applicable for component value calculation. The Booked and Intermediate formulae defined for the component are available in the option list. With a user-defined formula maintained through the rule builder, you can define a schedule with multiple formulae.

Flag

You can define a non-repayment schedule or a repayment schedule. This field is used to identify the schedule type:

- Normal: This refers to a repayment schedule. Repayment happens as and when the schedule falls due

- Moratorium: This refers to a non-repayment schedule or a repayment holiday during the repayment cycle of a mortgage

Number of schedules

The value captured here determines the number of times a schedule frequency should recur. For example, a 12 monthly schedule would have a ‘Monthly’ unit and number of schedules as 12.

Capitalized