The definition of a Product Characteristics rule is part of the Create or Edit Product Characteristics rule process. When you click Save in the Create Product Characteristics rule process, the rule is saved and the Product Characteristics rule summary page is displayed. However, Product Characteristic assumptions have not yet been defined for any of your products at this point. Typically, you would start defining your Product Characteristic assumptions for product-currency combinations before clicking Save.

Defining Product Characteristics Using Node Level Assumptions

Node Level Assumptions allow you to define assumptions at any level of the Product dimension Hierarchy. The Product dimension supports a hierarchical representation of your chart of accounts, so you can take advantage of the parent-child relationships defined for the various nodes of your product hierarchies while defining rules. Children of parent nodes on a hierarchy automatically inherit the assumptions defined for the parent nodes. However, assumptions directly defined for a child take precedence over those at the parent level.

Performing basic steps for creating or editing a Product Characteristics rule

From the Assumption Browser screen, select the product(s) and the currency for which you want to define Product Characteristics and select the “Add New” button to launch the Product Characteristic Details screen.

To define a Product Characteristics rule, complete the following steps:

1. Choose the Currency.

Note To define assumptions for all currencies with the selected product, choose the “Default Currency”. |

2. From the Assumption Browser, choose the product or products that you want to define.

3. Select the Add Assumption icon.

4. Type a value for each mandatory field. Mandatory input fields are marked with a red asterisk.

Note You can optionally select one of the seeded Product Profile templates or a user defined Product Profile to pre-populate the appropriate Product Characteristic fields. |

5. From the File menu, select Save.

Hint Using the default currency to setup assumptions can save data input time. At run time, the calculation engine uses assumptions explicitly defined for a product currency combination. If assumptions are not defined for a currency, the engine uses the assumptions defined for the product and the default currency. If the assumptions are the same across some or all currencies for a specific product, you can input assumptions for the default currency. Be careful using this option on screens where an Interest Rate Code is a required input. In most cases, you will want to use a currency specific interest rate curves for pricing instruments within each specific base currency. The Default Currency option, if used will apply a selected Interest Rate Code across all currencies. |

Assumption List Tab is present next to the Assumption Browser in all the screens which have assumption browser. This tab provides search capability with the help of five fields:

· Dimension Member Code

· Dimension Member Name

· Dimension Member Description

· Dimension Member Status

· Is Leaf

Dimension Member Code, Name and Description provide filter criteria for search such as: Contains, Starts With, Ends With, Exactly Matches.

Dimension Member Status is a drop-down list containing values such as: Defined, Not Defined, Inherited, Defined and Inherited, and All.

Is Leaf is a checkbox which can be toggled.

Search button initiates search on the assumption browser based on the filter criteria provided in the above mentioned fields. Reset restores default search criteria.

The search results will flatten the hierarchy and display all of the products that meet the input criteria. Use the pagination widget to display the number of products per page (up to a maximum of 99). You can proceed to edit or create new rules in the assumption list tab.

The details screen has three input tabs.

· All Business

· New Business

· Model Integration

Note The Model Integration tab will be available only if Moody's structured cashflow library integration is done with BSP. |

Assumptions made on the All Business tab apply to both current position data and new business balances.

The common Product Characteristic fields listed on the ALL Business tab are as follows:

Field |

Behavior |

Option Adjusted Spread |

The option adjusted spread is used during stochastic processing only. It is an adjustment to the stochastic discount factor used in calculating market value and value at risk. Valid values for this spread are between -5.000% and 5.000%, but a value less than 2.00% is recommended for best results. For more information about the calculation of discount factors, see the Oracle Financial Services Cash Flow Engine Reference Guide.

Note: BSP does not support stochastic processing. |

Model with Gross Rates |

If your institution has outsourced loan serving rights for some of your assets (most typically mortgages), the rates paid by customers on those assets (gross rates) will be greater than the rates received by your bank (net rates). For these instruments, both a net and gross rate will be calculated within the cash flow engine and both gross and net rate financial elements will be output. The gross rate is used for prepayment and amortization calculations. The net rate is used for income simulation and the calculation of retained earnings in the auto-balancing process.

Note: Modelling with gross rates is not supported in BSP. |

Interest Credited |

This option allows interest payments to be capitalized as principal on simple/non-amortizing instruments. |

Percent Taxable |

Percent Taxable specifies the percent of income or expense that is subject to the tax rates defined in the active Time Bucket rule. This is used with the Auto-balancing option in the ALM Process rules. Percent taxable should be setup for each product and reporting currency or product and default currency combination.

Note: Percent taxable is not used in BSP |

Currency Gain/Loss Basis |

Currency Gain/Loss Basis determines how exchange rate fluctuations are reflected in financial element results for each product and currency combination. The choices are: · Temporal · Historical Basis · Current Rate See the Oracle Financial Services Cash Flow Engine Reference Guide for more information on the cash flow calculations associated with currency gain/loss recognition techniques.

Note: Only used in ALM consolidated currency runs; not supported in BSP. |

Pay Equivalent Compounding Convention |

In most cases, interest rates are not adjusted for the differences in pay-basis between the quote basis of the pricing index and the payment frequency of the account to which the index is assigned. Some instruments, notably Canadian Mortgages, follow a convention that the interest rates are adjusted. In this case, the Pay-Equivalent Compounding Convention should be set to Semi-Annual Quoting Convention. For other accounts, the convention should be set to Do Not Adjust. |

Holiday Calendar |

The default value is Blank and is Enabled. This drop-down list contains the list of all holiday calendar definitions defined in the Holiday Calendar UI. |

Rolling Convention |

The default value is Unadjusted and is Enabled, only when Holiday Calendar has been selected in the preceding field. This drop-down list contains four values: Unadjusted Following Business Day Modified following business day Previous business day Modified previous business day Actual/Un-adjusted Payment on the actual day, even if it is a non-business day. Following Business Day The payment date is rolled to the next business day. Modified following business day* The payment date is rolled to the next business day, unless doing so would cause the payment to be in the next calendar month, in which case the payment date is rolled to the previous business day. Previous business day The payment date is rolled to the previous business day. Modified previous business day* The payment date is rolled to the previous business day, unless doing so would cause the payment to be in the previous calendar month, in which case the payment date is rolled to the next business day *Many institutions have month-end accounting procedures that necessitate this. |

Interest Calculation Logic |

There are two options: · Shift Dates Only · Recalculate Payment |

Note The holiday calendar attributes can be applied directly on the instrument records for existing business. If they are not applied on the records, the engine will use the definition from the all business tab to apply holiday calendar for existing and new business. |

Assumptions made on the New Business tab impact forecast business only. These assumptions are used together with the other Forecast Assumption rules including Forecast Balances, Pricing Margins and Maturity Mix to determine the behavior of your forecast instruments. There are five sub-tabs within New Business setup including:

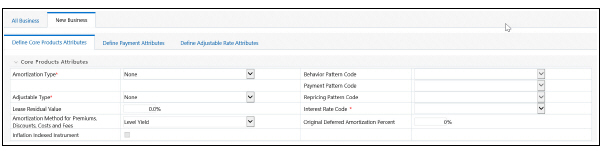

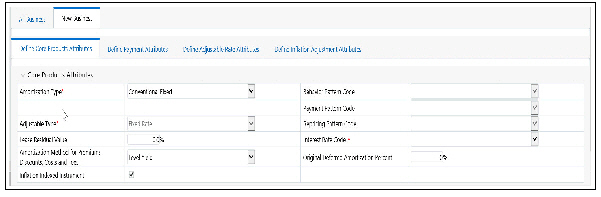

· Define Core Product Attributes

· Define Payment Attributes

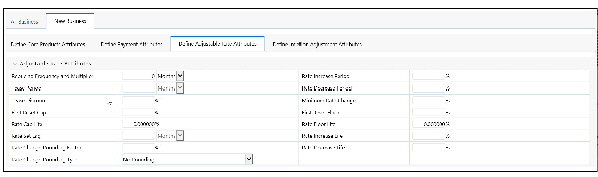

· Define Adjustable Rate Attributes

· Define Negative Amortization Attributes

· Define Other Mortgage Attributes *

· Define Inflation Adjustment Attributes **

Note Note: * This tab will be displayed only if you are mapped to ADCo LDM functionality and currency is selected as USD. ** This tab will be displayed, if Inflation Indexed Instrument option is selected in Define Core Products Attributes tab for New Business. |

There are dependencies built into the tabular structure of this screen. Based on assumptions made in the first two tabs, the remaining two tabs may not be active.

Field |

Value |

Behavior |

Amortization Type Code |

Conv. Fixed, Conv Adjust., Adjst/Ng Amrt |

Always interest in arrears, therefore disables Interest Type |

Amortization Type Code |

Conv. Fixed, Rule-of-78's |

No repricing occurs, therefore disables the Define Negative Amortization Attributes and enables the Adjustable Rate Attributes tab. In this case, Rate Change Rounding Type, Rate Change Rounding Factor (when there is Rounding), Rate Floor Life and Rate Cap Life fields will be enabled in the Adjustable Rate Attributes tab. |

Amortization Type Code |

Adjst/Ng Amrt |

Enables Negative Amortization Attributes tab |

Amortization Type Code |

Payment Pattern |

Enables the Payment Pattern drop list |

Amortization Type Code |

Behavior Pattern |

Enables the Behavior Pattern drop list |

Amortization Type Code |

Conv Fixed, Conv Adjust., Level Principal, Non Amortizing |

Inflation Indexed Instrument check box will be enabled |

Adjustable Type Code |

Other Adjustable, Fixed Rate, Floating Rate, or Repricing pattern |

Repricing Frequency is not applicable, or it is defined elsewhere, therefore disables Repricing Frequency and Multiplier. Enables the Adjustable Rate Attributes tab When Adjustable Type Code is Fixed, the Adjustable Rate Attributes tab is enabled. In this case, Rate Change Rounding Type, Rate Change Rounding Factor (when there is Rounding), Rate Floor Life and Rate Cap Life fields will be enabled in the Adjustable Rate Attributes tab. |

Adjustable Type Code |

Repricing Pattern |

Enables the Repricing Pattern drop list. In addition, several of the repricing attributes are defined elsewhere, therefore they are disabled in this rule. Only periodic increase and decrease, rate change min and rounding are enabled |

Repricing Frequency |

"0" |

No repricing occurs, therefore disables Adjustable Rate Attributes |

Model with Gross Rates |

Off |

Net Margin Flag options are only necessary when modeling with different gross rates and net rates, therefore disables Net Margin Flag.

Note: This is not supported in BSP. |

Rate Change Rounding Type |

"No Rounding" or "Truncate" |

Rounding does not apply, therefore disables Rate Change Rounding Percent |

Currency |

|

Allows display of Interest Rate Codes and Transfer Rate Interest Rate Codes for which the selected currency is the reference currency. In Product Characteristics, Default Currency allows all Interest Rate Codes, regardless of currency |

Following is a listing of new business fields used in the Product Characteristics rule > Core Product Attributes tab.

Field |

Description |

Amortization Type |

Method of amortizing principal and interest. The choices consist of all standard OFSAA codes and all additional user-defined codes created through the Payment Pattern and Behavior Pattern interfaces, as given below: · Conventional Fixed · Conventional Adjustable · Balloon Payment · Adjustable Negative Amortization · Non-Amortizing · Rule of 78's · Level Principal · Payment Pattern · Behavior Pattern · Lease |

Adjustable Type |

Determines the repricing characteristics of the new business record. The choices consist of all standard OFSAA codes plus Repricing Pattern. The standard OFSAA codes are as follows: · Fixed Rate · Floating Rate · Other Adjustable |

Lease Residual Value |

For Lease instruments, this value specifies the residual amount as a percent of the par balance. |

Amortization Method for Premiums, Discounts and Fees |

Determines the method used for amortizing premiums, discounts or fees. The available codes are: · Level Yield · Straight Line |

Behavior Pattern Code |

Lists all user-defined behavior patterns created through the user interface. |

Payment Pattern Code |

Lists all user-defined payment patterns defined through the user interface. |

Repricing Pattern Code |

Lists all user-defined reprice patterns created through the user interface. |

Interest Rate Code |

Defines the pricing index to which the instrument interest rate is contractually tied. The interest rate codes that appear as a selection option depend on the choice of currency. The interest rate code list is restricted to codes which have the selected currency as the reference currency. If the default currency is chosen, all interest rate codes are available as a selection. |

Original Deferred Amortization Percent |

The initial deferred balance expressed as a percent of original par balance. |

Inflation Indexed Instrument |

Check box to model instrument as Inflation Indexed. |

Following is a listing of new business fields used in the Product Characteristics rule > Payment Attributes tab:

Field |

Description |

Payment Frequency |

Frequency of payment (P & I), Interest or Principal). For bullet instruments, use zero. |

Interest Type |

Determines whether interest is calculated in arrears or advance or if the rate is set in arrears. There are three interest types: · Interest in Arrears · Interest in Advance · Set in Arrears For conventional amortization products, interest in arrears is the only valid choice. |

Rolling Convention |

Reserved for future use. |

Accrual Basis |

The basis on which the interest accrual on an account is calculated. The choices are as follows: · 30/360 · Actual/360 · Actual/Actual · 30/365 · 30/Actual · Actual/365 · Business/252 * |

Compounding Basis |

Determines the number of compounding periods per payment period. The choices are the following: · Daily · Monthly · Quarterly · Semi-Annual · Yearly · Continuous · Simple · At Maturity |

Net Margin Flag |

The setting of the net margin flag affects the calculation of net rate. The two settings are: · Floating Net Rate - the net rate reprices in conjunction with the gross rate, at a value net of fees. · Fixed Net Rate - the net rate equals a fixed fee equal to the net margin. |

Note * A Holiday calendar selection is required if business/252 accrual basis is selected. Business/252 accrual basis is only applicable to the recalculate option of the holiday calendar rule. If user selects the shift payment dates, the payment will still be recalculated for the non holiday/weekend date. |

Following is a listing of new business fields used in the Product Characteristics rule > Adjustable Rate Attributes tab:

Field |

Description |

Repricing Frequency |

Contractual frequency of rate adjustment |

Tease Period |

The tease period is used to determine the length of tease period. |

Tease Discount |

The tease discount is used in conjunction with the original rate to calculate the tease rate. The tease rate is the original rate less the tease discount. |

First Reset Cap |

This indicates the maximum delta between the initial rate and the first reset for mortgage instruments that have a tease period. This rate will be applicable at the tease end period, prior to the first reset. After this, the periodic and lifetime cap value will be applied. The value of this field will be automatically populated from Product Profile window if the product is mapped to Product Profile and value is defined for First Reset Cap.

For example: Current Rate = 3.5% (from the instrument record) Margin = 0.3 % First Reset Cap = 0.5% (from the instrument record) First Reset Floor = 0.1% (from the instrument record)

Scenario 1: If New Forecasted Rate = 5.1% (Forecast Rates Assumption)

Fully indexed rate (after applying minimum rate change, rounding effects) is higher than the (Current Rate + First Reset Cap). So, the new rate assigned will be 3.5% + 0.5% = 4.0% |

First Reset Floor |

This is the initial minimum value for mortgage instruments that have a tease period. This floor rate will be applicable at the tease end period, prior to the first reset. After this, the periodic and lifetime floor value will be applied. The value of this field will be automatically populated from Product Profile window if the product is mapped to Product Profile and value is defined in for First Reset Floor. |

Rate Cap Life |

Maximum rate for life of the instrument. |

Rate Set Lag |

Period by which the rate lookup lags the repricing event date. |

Rate Change Rounding Factor |

Percent to which the rate change on an adjustable instrument is rounded. |

Rate Change Rounding Type |

Method used for rounding of interest rate codes. The choices are as follows: no rounding, truncate, round up, round down, round nearest. |

Rate Increase Period |

Maximum interest rate increase allowed during the cycle on an adjustable rate instrument. |

Rate Decrease Period |

Maximum amount rate can decrease during the repricing period of an adjustable rate instrument. |

Minimum Rate Change |

The minimum required change in rate on a repricing date. |

Rate Floor Life |

Minimum rate for life of the instrument. |

Rate Increase Life |

Maximum interest rate increase allowed during the life of an adjustable rate instrument, used to calculate rate cap based on forecasted rate scenario. If both rate increase life and rate cap are defined, the process uses the more restrictive rate. |

Rate Decrease Life |

Maximum amount rate can decrease during the life of an adjustable rate instrument, used to calculate the rate floor based on the forecasted rate scenario. If both rate decrease life and rate floor are defined, the process uses the more restrictive rate. |

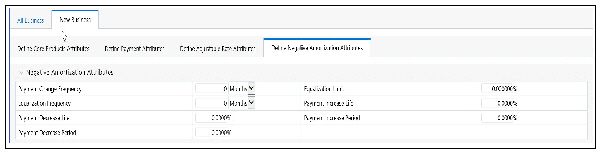

Following is a listing of new business fields used in the Product Characteristics rule > Negative Amortization Attributes tab:

Field |

Description |

Payment Change Frequency |

The frequency at which the payment amount is recalculated for adjustable negative amortization instruments. |

Equalization Frequency |

Frequency at which current payment necessary to fully amortize the instrument is re-computed. |

Payment Decrease Life |

Maximum payment decrease allowed during life of a negative amortization instrument. |

Payment Decrease Period |

Maximum payment decrease allowed during a payment change cycle of a negative amortization instrument. |

Equalization Limit |

Maximum negative amortization allowed, as a percent of original balance. E.g., if principal balance should never exceed 125% of original balance, this column would equal 125.0 |

Payment Increase Life |

Maximum payment increase allowed during the life of a negative amortization instrument. |

Payment Increase Period |

Maximum payment increase allowed during a payment change cycle on a negative amortization instrument. |

Following is a listing of new business fields used in the Product Characteristics rule > Define Other Mortgage Attributes tab:

Field |

Description |

Customer Credit Score |

The default value of this is 700 and it should be in the range of 300-850. The value of this field will be automatically populated from Product Profile window if the product is mapped to Product Profile and value is defined for Customer Credit Score. |

Original Loan To Value |

The default value of this is 80 and it should be in the range of 1-300. The value of this field will be automatically populated from Product Profile window if the product is mapped to Product Profile and value is defined for Original Loan To Value. |

Issuer |

Select the name of Issuer. The default value is FANNIE_MAE. |

Prepayment Index |

This is the first index value fetched by the UI among the defined ADCo Curves. |

Note: This tab will be displayed if ADCo LDM mapping is done, and if the selected currency is USD and product is of account type “Earning Assets”.

This tab allows you to made the assumptions based on Moody's structured cashflow library integration for All Business and New business balances.

This tab will be displayed only if you have installed Moody's structured cashflow library. Following are the prerequisites to view the “Model Tuning” tab:

· Moody's structured cashflow library installed on the setup

· Moody's structured cashflow library enabled for the specific user

· Product is securitized products or loans

You can tune the model using the Tune option. Select the model from Model Selection drop-down list and click Tune. Following modelling options are available in Model Selection drop-down list:

· None

· Source System Provided

· ADCo

Based on the selected model, the UI parameters will vary.

Field |

Behavior |

Prepayments |

This is the magnitude for prepayment rate. The default value of this is 1, and it should be greater than 0. |

Default |

This is the magnitude for default rate. The default value of this is 1, and it should be greater than 0. |

Recovery |

This is the magnitude for recovery rate. The default value of this is 1, and it should be greater than 0. |

Recovery Lag |

This is the recovery lag applied to each loan. The default value of this is 0, and the value range is 1 to 100. |

Servicer Advancing |

Select the servicer advancing as None, Interest, or Both. The default value of this is None. |

Draw Rates |

This is the magnitude for mortgage Draw rates. The default value of this is 1, and it should be greater than 0. |

Enter values in these parameters if you want to use ADCo LDM integration along with Moody's Structured Cash flow library.

Field |

Behavior |

SMM for Failed Loans |

This is the failed loan's SMM in percentage. The default value of this is 0 and it should be in the range of 0-100. |

MDR for Failed Loans |

This is the failed loan's MDR in percentage. The default value of this is 0 and it should be in the range of 0-100. |

Recovery for Failed Loans |

This is the failed loan's recovery in percentage. The default value of this is 0 and it should be in the range of 0-100. |

Subprime FICO Loans |

Loan is considered subprime if FICO is less than this value ( 620 if not provided). The default value of this is 620 and it should be in the range of 300-850. |

FICO to use(if not available) |

FICO to use for loans which do not have this information. The default value of this is 680 and it should be in the range of 300-850. |

When Inflation Indexed Instrument check box is selected, the Define Inflation Adjustment Attributes tab is enabled. For more information on Inflation Indexed Instrument calculation, refer to Oracle Financial Services Cash Flow Engine Reference Guide.

Note The Define Inflation Adjustment Attributes tab will be enabled if Adjustment type is selected as Conventional Adjust, Conventional Fixed, Level principal, or Non-Amortizing. |

Tab |

Field |

Behavior |

Index Adjustment Attributes |

Index Name |

Lists all Economic Indicator defined through user interface. |

Index Adjustment Attributes |

Capital Protection Category |

Determines Capital protection to be provided to Inflation indexed instruments. The choices are: · No Floor: No Floor does not provide any downside protection. · Floor of 1: Floor of 1 provides protection from downside movement. · Max during Life: Max during life gives maximum advantage using maximum Index factor for calculation. |

Index Adjustment Attributes |

Index Adjustment Type |

Determines type of Index adjustment. The choices are following: · Principal and Interest · Principal Only · Interest Only |

Note For more information on cash flow calculations associated with Inflation indexed instrument, refer to Oracle Financial Services Cash Flow Engine Reference Guide. |