The assignment of transfer pricing methodologies is part of the Create or Edit Transfer Pricing rules process where assumptions about transfer pricing methodologies are made for product-currency combinations. When you click Save in the Create Transfer Pricing rules process, the rule is saved and the Transfer Pricing rule Summary page is displayed. However, the transfer pricing methodology has not yet been defined for any of your products at this point. Typically, you would start defining your methodologies for product-currency combinations before clicking Save.

The Transfer Pricing rule supports definition of assumptions for combinations of two dimensions: Product and Currency.

You can define transfer pricing methodologies for your entire product portfolio one currency at a time. Suppose your portfolio is comprised of products denominated in two currencies (US Dollar and Japanese Yen) and that you want to specify different transfer pricing assumptions and /or different Transfer Pricing yield curves, for each product group. Using the currency selection drop-down list, you can first define assumptions for the products denominated in US Dollars and then proceed with defining assumptions for the Yen-based products.

Once you have created a Transfer Pricing rule, you can assign transfer pricing methodologies to product-currency combinations in either of the following two ways:

By creating a conditional assumption using conditional logic. See:

· Associating Conditional Assumptions with Prepayment Rules

· Defining Prepayments Using Node Level Assumptions

Directly on the Transfer Pricing methodology page, as described here.

Performing basic steps for creating or updating a Transfer Pricing rule

This table describes key terms used for this procedure.

Term |

Description |

Yield Curve Term |

Defines the point on the yield curve that the system references to calculate transfer rates. |

Historical Range |

Specifies the period over which the average is to be taken for the Moving Averages method. |

Lag Term

|

Specifies a yield curve from a date earlier than the Assignment Date for the Spread from Interest Rate Code method. |

Rate Spread |

The fixed positive or negative spread from an Interest Rate Code or Note Rate, used to generate transfer rates in the Spread from Interest Rate and Spread from Note Rate methods. |

Model with Gross Rates |

This option allows you to specify whether modeling should be done using the net or gross interest rate on the instrument. This option is only applicable when the Net Margin Code is also set to one, for example, Fixed. Gross rates are typically selected while modeling the effect of serviced portfolios where the underlying assets have been sold but the organization continues to earn servicing revenue based on the original portfolio. |

Assignment Date |

This is the effective date of the yield curve. |

Percentage/Term Points |

The term points that the system uses to compute the Redemption Curve method results. A percentage determines the weight assigned to each term point when generating results. |

1. Navigate to the Assumption Browser page.

2. Select a Product Hierarchy

3. Select a Currency

Note The list of currencies available for selection is managed within Rate Management, and reflects the list of "Active" currencies. Expand the hierarchy and select one or more members (leaf values and/or node values) from the product hierarchy. |

4. Click the Add icon to begin mapping Transfer Pricing methods to the list of selected product dimension members. The system displays a list of all the products (for which you can define assumptions) or currencies (that are active in the system).

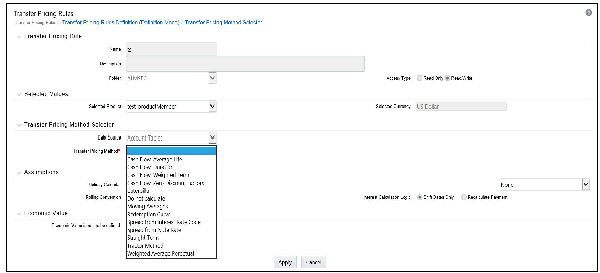

5. In the TP Method selector page, Account Table data source is selected by default and disabled.

6. Select the Transfer Pricing method for the selected product member.

Tip The Transfer Pricing methodologies available depend on the selected data source. Depending on the transfer pricing method selected, certain required and optional parameter fields are displayed. You can update these fields as required. |

7. Click Apply.

At this point you can:

§ Continue defining additional methodologies for other product-currency combinations contained in your selection set, by repeating the above procedure.

§ Complete the process by clicking Cancel or by answering to NO to the confirmation alert after applying assumptions for each Product / Currency combination in your select set.

8. From the Assumption Browser page, click Save.

9. The new assumptions are saved and the Transfer Pricing rule selector page is displayed.

Note Oracle Balance Sheet Planning provides you with the option to copy, in total or selectively, the product assumptions contained within the Adjustments, Transfer Pricing, and Prepayment rules from one currency to another currency or a set of currencies or from one product to another product or a set of products. |

Guidelines

Availability of Transfer Pricing Methodologies

The availability of transfer pricing methodologies depends on the data source that you select: Account Table or Ledger Table. In BSP, by default, only Account Table data source is selected and is disabled. The following table describes the Transfer Pricing Methodologies available for the Account Table Data Source and displays whether that methodology requires the selection of a Transfer Pricing Interest Rate Code.

Note The Interest Rate Code LOV is filtered by the selected Currency. Child nodes for which no assumptions have been specified automatically inherit the methodology of their closest parent node. So if neither a child node nor its immediate parent has a method assigned, the application searches up the nodes in the hierarchy until it finds a parent node with a method assigned, and uses that method for the child node. However, if no parent node has a method assigned then the application triggers a processing error stating that no assumptions are assigned for the particular product/currency combination. |

Transfer Pricing Methodology |

Interest Rate Code |

|

Data Source: Account Table |

Cash Flow: Average Life |

Yes |

Yes |

|

Cash Flow: Duration |

Yes |

Yes |

|

Cash Flow: Weighted Term |

Yes |

Yes |

|

Cash Flow: Zero Discount Factors |

Yes |

Yes |

|

Moving Averages |

Yes |

Yes |

|

Straight Term |

Yes |

Yes |

|

Spread from Interest Rate Code |

Yes |

Yes |

|

Spread from Note Rate |

|

Yes |

|

Redemption Curve |

Yes |

Yes |

|

Required Parameters

You cannot define a transfer pricing methodology successfully, unless you specify the required parameters. The following table displays the parameters associated with each transfer pricing method and specifies whether they are required or optional. The optional parameter fields display default values. However, you may decide to change the values for the optional parameters.

Transfer Price Method |

Yield Curve Term |

Historical Range |

Lag Term |

Rate Spread |

Assignment Date |

Term Points |

|---|---|---|---|---|---|---|

Cash Flow: Average Life |

|

|

|

|

|

|

Cash Flow: Weighted Term |

|

|

|

|

|

|

Cash Flow: Duration |

|

|

|

|

|

|

Cash Flow: Zero Discount Factors |

|

|

|

|

|

|

Moving Averages |

Required |

Required |

|

|

|

|

Straight Term |

|

|

|

|

|

|

Spread from IRC |

Required |

|

Required |

Required |

Required |

|

Spread from Note Rate |

|

|

|

Required |

|

|

Redemption Curve |

|

|

|

|

Required |

Required |