5. Account Creation

Mortgage Accounts in the Mortgages module represent the receivable accounts that you create while disbursing a mortgage. These accounts derive their feature from the Mortgage Product. Mortgage Accounts are mapped to the Asset GL through the accounting Role MORTGAGE_ACCOUNT. This role has to be mapped to the respective Asset GL of the Bank. You can override some product features at the account level.

The system allows you to do the following actions on the Mortgage accounts:

- Account Main Details Maintenance/Light Mortgages

- Liability details and UDE Values Maintenance

- Account Preferences/Defaults

- Account Component schedules

- Charges Maintenance and Settlement details

- Linkages Information

- Events, Events Due and Events Overdue

This chapter contains the following sections:

- Section 5.1, "Mortgage Account"

- Section 5.2, "Generating a Loan Account"

- Section 5.3, "Calculating Exponential Interest for Loans"

- Section 5.4, "Maintaining Financial Operations Tax (IOF)"

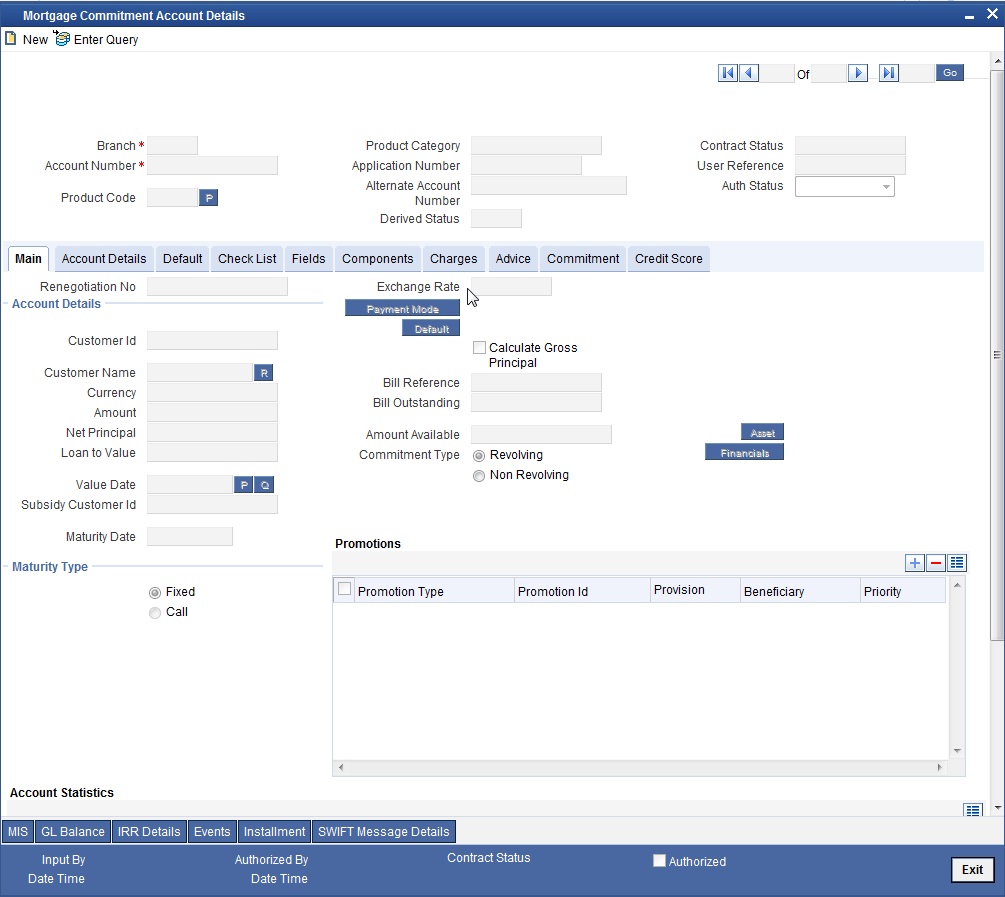

- Section 5.5, "Commitment Account"

- Section 5.6, "Saving and Authorizing Mortgage/Commitment Account"

- Section 5.7, "Multilevel Authorization of an Account"

- Section 5.8, "Manual Confirmation by Notary"

5.1 Mortgage Account

This section contains the following topics:

- Section 5.1.1, "Creating a Mortgage Account"

- Section 5.1.2, "Main Tab"

- Section 5.1.3, "Preferences Tab"

- Section 5.1.4, "Holiday Preference Tab"

- Section 5.1.5, "Check List Tab"

- Section 5.1.6, "Fields Tab"

- Section 5.1.7, "Components Tab"

- Section 5.1.8, "Charges Tab"

- Section 5.1.9, "Linkages Tab"

- Section 5.1.10, "Advices Tab"

- Section 5.1.11, "Credit Score Tab"

- Section 5.1.12, "Specifying Other Applicants Details"

- Section 5.1.13, "Capturing Asset Details"

- Section 5.1.14, "Repayment Holiday for Amortized Mortgages"

- Section 5.1.15, "Viewing Mortgage Account Summary"

5.1.1 Creating a Mortgage Account

The account screen accepts the Customer, Currency and Amount Financed and creates a Light Mortgage. This is a default Mortgage that takes all other details from the defaults the product provides. For creating simple accounts in the Mortgages module, you can follow this simple process. These Mortgages are called Light Mortgages in the Mortgages module. You can create a mortgage account using the ‘Account Details’ screen. You can invoke this screen by typing ‘MODACCNT’ in the field at the top right corner of the Application tool bar and clicking the adjoining arrow button.

You can specify the following generic details in the Account Details screen:

Branch

The system displays the Branch Code of the branch into which the user has logged in, for which the UDE values are maintained.

Account Number

Based on the parameters that setup at the branch level, the account number would be either auto generated or would have to be captured in this field.

Product Code

Click the option list to select a Product Code from the list of values. Double click on a Product Code to select a particular code. The product codes are maintained in the Product Definition screen.

Product Category

The system displays the product category in this field

Application Number

The system displays the Application Number in this field.

Note

This is applicable only if the origination of the mortgage is in Oracle FLEXCUBE or is interfaced

Version Number

The system displays the current Version Number of the account. A new version number is created when changes like Roll over, Amendment are made to a mortgage. This is displayed in the top right corner of the ‘Account Details’ screen.

Alt Acc No

Specify the alternate account number in this field. It can be an account number in the existing system from which the account has migrated to Oracle FLEXCUBE.

User Defined Status

The system defaults the value of CIF status as available in the ‘Customer Maintenance’ screen. This status is the worst status among all the mortgages, savings accounts and current accounts for the customer in the current branch.

Note

This is done if you have opted for status processing at the ‘Group/CIF’ level as part of your branch preferences.

Derived Status

The system defaults the status of the individual mortgage account here.

User Reference Number

A 16-digit User Reference Number is autogenerated and displayed here if the ‘Auto Generate User Ref No’ option is checked in the Branch Parameters. The format of the user reference number is BranchCode + ProductCode + Sequence number. You are allowed to modify the auto-generated User Ref No.

If the ‘Auto Generate User Ref No’ in Branch Parameters is not checked then the User Ref No will be blank by default and you have to specify it manually. Validations are done by the system not to save the account if an unsuppressed payment message is present which has the User Ref No as blank.

5.1.2 Main Tab

The following details regarding the mortgage account are captured here:

Account Details

The following details are captured here:

Amount Financed

Specify the total mortgage amount of the mortgage in this field. On saving the transaction after entering all the required details in the system, the system validates the value of the transaction amount against the following:

- Product transaction limit

- User Input limit

If the transaction currency and the limit currency are different, then the system converts the amount financed to limit currency and checks if the same is in excess of the product transaction limit and user input limit. If this holds true, the system indicates the same with below override/error messages:

- Number of levels required for authorizing the transaction

- Transaction amount is in excess of the input limit of the user

Note

If Calculate Gross Principle is checked, then the amount financed is the gross principal.

Currency

To select a currency, click the LOV button. A list of currencies is displayed. Double click to select a currency.

Net Principal

The Net Principal is the actual principal amount financed. It is system calculated and excludes any other funded components.

Customer Name

Specify the customer name here.

Value Date

Select the Value date of the mortgage in this field using the date button.

Click ‘Product Default’ button after entering product code, customer ID, currency and amount financed. The system defaults other details maintained for the selected product. The system also defaults the schedule definitions from the product and computes the detailed schedules. After clicking the ‘Product Default’ button, you cannot change the product code. Also, the system prompts you to click the ‘Product Default’ button once again if you change ‘Customer ID’, ‘Currency’ or ‘Amount Financed’ fields.

Settlement Sequence Number

The system displays the settlement sequence number during product default. The default value displayed will be zero. You can select a different value from the adjoining list of values.

Customer ID

To select a customer ID, click the option list. A screen called ‘Find Customer Details’ is displayed. You can enter search criteria in this screen. For example, you can enter the customer name or number and click on the ‘Search’ button. The system then fetches you all the details corresponding to the Customer name or account. Once you find all the details, double-click on the record to return to the account details screen.

Subsidy Customer ID

Specify the unique identifier of the agency or the third party included in the subsidy mortgage contract.

Loan to Value

Specify the accepted value of the mortgaged property. For example, if the mortgaged property’s actual value is 100,000, then the mortgage value of the property will be 80,000.

The system calculates the amount to be financed based on ‘Loan to Value’, the rate of interest, fees and charges are charged at the time of defaulting.

On schedule regeneration, system calculates the Annuity amount for each disbursement schedule. Effectively disbursed amount will be credited to the customer’s account and it will be called Equal Monthly Payment (Annuity).

System does not allow making any payment schedule other than bullet schedule for principal and interest components.

On maturity of reverse mortgage , if the borrower is alive then the contract is rolled over using special rollover with normal Retail Lending mortgage product. This special rollover is done manually.

VAMI can be done on the RML contracts like normal mortgage contracts i.e. user can do amendment of schedules/rate of interest from VAMI screen. On change of schedules/rate, system recalculates the annuity amount, effective the date of the VAMI.

Maturity Date

Select the maturity date in this field using the date button.

If you are not sure of the maturity date, enter the tenor of the mortgage in either days or months or years as say 3M for 3 Months etc. The system automatically calculates the date on tabbing-out of the tenor.

Maturity Type

Select the Fixed or Call option to specify the type of mortgage maturity.

Note

The system by default selects the option Fixed. For the Call option, the maturity date will not be computed upfront.

If you choose the ‘Call’ option, IRR processing will not be applicable to the account

Index Exch Rate

Specify the exchange rate for index currency here

Calculate Gross Principle

Check this box if you want the system to calculate the gross principal for the mortgage. If you have checked this box and have entered the amount financed then system takes the amount financed as the gross principal.

Bill Ref No

Select the reference number of the export bill against which you want to link the mortgage, from the option list. The option list displays all active and authorized export bill contracts with non zero positive outstanding amount. You can link multiple mortgages to as bill. However, the sum total of all mortgages linked with an export bill should not exceed the outstanding amount for the export bill.

Note

This is enabled only for those Mortgages products for which the ‘CL against Bill’ option is selected at the product preference level.

Bill Outstanding

The outstanding amount of the bill selected is displayed here

Packing Credit

The system populates this check box by default for all contracts under the ‘Packing Credit Product’. However you can uncheck it leaving such contracts to be unavailable for selection in BC towards Packing Credit Mortgages .If you check this box without flagging the Packing Credit product option under Mortgages Products, the system throws an error on attempting to save the contract.

Note

Repayment of Mortgages in the case of CL Accounts created with ‘Packing Credit Product’ flags is through Bullet Schedules only.

For more details on Pre-Shipment Financing refer section ‘Specifying Purchase Details’ in chapter ‘Processing Bills’ of the ‘Bills and Collections’ manual.

Commitment Type

Select the type of commitment contract that you want to create. The options available are:

- Revolving - In case of revolving mortgages the amount available is reinstated whenever there is a payment against a mortgage linked to it. So the paid amount is again available for reutilization. The reinstatement happens only if the payment is done before the validity period of the commitment contract.

- Non-Revolving - In case of non revolving mortgages the amount repaid against a mortgage is not reinstated.

Book Date

In this field, the current date when the mortgage details were entered is defaulted and cannot be modified.

Installment Start Date

Enter the original start date of the mortgage in this field. This will be defaulted to the Mortgage Value date at the time of Mortgage creation.

Note

For rolled over contract, the system populates the new start date in the Value Date field and this field remains unchanged and will hold the original start date.

Total Principal Outstanding

Total Principal Outstanding inclusive of the compounded interest or penalty is defaulted here.

Promotions

The following details are captured here:

Promotion Type

The system displays the Promotion type to which the original mortgage is linked. It could be any of the following:

- CONVENIOS

- PROMOTION

- CORFO

- FOGAPE

Promotion ID

The system displays the promotion ID in this field

Beneficiary

The system displays the beneficiary CIF in this field

Priority

The system displays the priority assigned to the promotion

Account Statistics

Once you select an Account Number, the system displays the following details pertaining to the current status of the account:

- Component Name

- Expected

- Overdue Amount

- Outstanding Principle

- Advance Amount

- Currency

The Account creation and any other change to an account is updated the audit trail of the record. In the audit trail, the Account status details are also displayed. An Account can be active or uninitiated. Once it is active, it can be reversed, deleted or liquidated based on the operations on it. This is displayed on the screen.

Securitization status

The system displays the securitization status. It can be anyone of the following:

- Blank – if the account is not involved in securitization or is not a part of the securitization pool

- Marked for securitized –if the loan account, which is part of securitization contract (on batch), and the securitization batch is not yet executed

- Securitized –if the batch process (post securitization) is successfully completed

Effective Date

You can specify the following detail here:

Effective Date

The effective date is used to pick the UDE value. The system displays this date from the General UDE maintenance screen.

For a product + currency combination, if the UDE values are not maintained for the effective date, then the system defaults “0” which the user can then edit.

UDE Values

The UDE values for each Account are maintained here. The UDE values default from the UDE values maintenance for the Product, Currency, effective dates combination. These can be overridden by providing account level UDE values. However the UDE are only those defined at the product level.

The system checks whether the UDE values fall within the minimum and maximum limits specified for the UDEs linked to the product. If a UDE value falls outside the permissible limits, the system will throw an error message,

If there are no product level UDE values maintained, the system will default the UDE value to Zero. However, at the time of saving, if UDE values are zero or any invalid value, then an override will be raised with an appropriate error message. If required this can be configured as an error message. In case of an ERROR, you will have to give a valid value. While if it is an OVERRIDE, you can overlook the message and continue and if it is for an ONLINE AUTHORIZATION the parameter should be authorized appropriately.

The system displays the UDE values from that of the UDE values maintenance screen. These values can be overridden by providing account level UDE values. However, the value can be maintained only for those UDEs defined at the product level. No New UDEs can be introduced at the account level.

You can specify the following details for the UDE values:

UDE ID

To select a UDE Id, click the option list. A list of UDE Ids is displayed. Double click to select a UDE Id.

UDE Values

Specify the Actual Value for the UDE based on the effective Date in this field. The value specified here should fall within the minimum and maximum limits maintained for the UDE linked to the underlying product.

Note

Mandatory if a UDE is maintained.

Rate Code

Select the code for the Floating Rates if any and the spread on it applicable in this field by clicking the option list. A list of values is displayed. Double click on a value to select it.

Code Usage

Select the Code usage which can be periodic or automatic in this field

Rate Basis

The system displays the rate basis from maintenance or product level. You can select and modify the value from the drop down list. The list displays the following values:

- Null

- Per Annum

- Per Month

- Quote Basis

Note

- The rate basis will be defaulted as Quote Basis if the rate code attached to the UDE has a quote basis other than ‘Per Annum’. If the quote basis is per annum, then the same will be defaulted here.

- If TD account number is selected as ‘Rate Code’, then the system will update the ‘Rate Basis’ as ‘Per Annum’.

Resolved Value

This denotes the final value of a UDE. Resolved value = Rate code value taken from Floating Rate Maintenance + the spread [UDE Value]

5.1.3 Preferences Tab

The defaults are maintained by the bank. Depending upon the combination of various preferences, the bank can have various account preferences. The defaults primarily are based on product definition and can be overridden.

You can specify the following details here:

Amend Past Paid Schedule Allowed

This preference determines if you can modify any feature such as interest rate, installment amount which affects already paid schedules. If you select this option then the paid schedules are recalculated and liquidations on them are recognized as pending as appropriate.

Liquidate Back Valued Schedules

If this flag is turned on, during initiation, when a mortgage is input back dated and if there are any installment dues, then all those schedules with a due date less than the system date will be liquidated on initiation

Maximum Renegotiations

Specify the maximum number of renegotiation allowed for the account.

Note

If maximum renegotiation is not maintained, system will perform renegotiation without any restrictions. If the maximum renegotiation value is given as ‘zero’, system will raise override in the first renegotiation itself.

Renegotiation No

The system displays the renegotiation count. This is the number of renegotiations that are already performed on the loan account.

Stop Disbursement

Check this option to stop the disbursement of annuity for the mortgage loan in case of any legal or compliance issues.

Note

Last n annuities are not disbursed in a given reverse mortgage loan contract if the 'Stop Disbursement' option is checked or 'Till Date' is not updated due to lack of information or proof. And, if the ‘Stop Disbursement’ option is unchecked in Value dated amendment or 'Till Date' is changed to some future date, then the system will disburse all n annuities in the EOD or BOD.

Notary Pre Confirmed

Check this box to indicate that you have already got confirmation from the notary, before creation of the mortgage.

If the value date of the account is on or before the application date, then ‘NCON’ will trigger INIT and DSBR event for auto disbursement product, else user will need to trigger manual disbursement post the notary confirmation.

If the value date of the loan is beyond the application date, the system will trigger the NCON event online, once the value date is reached the INIT and DSBR events gets fired, if the loan is under an auto disbursement product.

You can also save a mortgage account with this option unchecked. Once you receive the confirmation, you can trigger the ‘NCON’ event manually using the ‘Manual Notary Confirmation’ screen.

Refer the section ‘Manual Confirmation by Notary’ in this chapter to see the steps required for getting confirmation from Notary.

Recalc Annuity on Disbursement

Check this option to indicate that annuity amount /should be recalculated on disbursement.

Partial Block Release

Check this box to indicate whether the partial release of term deposit should be done as part of loan repayment.

Loan Statement Required

The system defaults the status of this checkbox based on the preferences maintained for the MO product. However, you can modify the default value. Check this box to indicate that the loan statement should be generated.

If this field is checked and the loan statement maintenance is not done at product level, the system will display an error at the time of saving the contract.

Note

The system maintains ‘CLST_DETAILED’ message for DSBR event, to generate Loan Advice on each disbursal in loan account authorized at product event level.The system maintains the ‘Loan Statements’ message types in ‘Notices and Statements’ tab at product level.

Liquidation

You can maintain the following liquidation preferences:

Liquidation Mode

The system defaults the mode of liquidation from the product level. However you can modify the same to indicate the mode of liquidation that you are maintaining. You can select one of the following options:

- Manual

- Auto

- Component

Auto Liqd Reversed Pmt

If auto liquidation has been reversed in an account, it will be retried depending upon the status of this field. If this option is selected, then the auto liquidation is retried.

Partial Liquidation

If you select this option, system will perform partial auto liquidation

Retries for Auto liquidation

When auto liquidation option is chosen and funds are not available, the number of times the system can retry auto liquidation is determined by this field

If blank, the number of retries is infinite

Retries Advice Days

Number of retries for an advice is defaulted here from the product maintenance level; however, you can modify if needed. The value should be less than the value maintained for ‘Retries Auto Liquidation Days’.

Track Receivable

If Track receivable option is checked for an account, it tracks the amount to be liquidated as a receivable if funds are not available. So upon any subsequent credit, the receivables are blocked and allocated to the pending liquidation.

Auto Liquidation

Select this option to indicate that the Track receivable option is for Auto Liquidations. You can modify this during VAMI/rollover/renegotiation.

Note

This is defaulted from the product level

On schedule liquidation if there are insufficient funds in the settlement account to satisfy the liquidation and if both the product and the account are marked for receivable tracking then system initiates tracking of receivable.

If the account is marked for Partial liquidation, then liquidation happens to the extent of available funds, and the remaining amount is tracked.

If the account is not marked for partial liquidation, and the amount available in the settlement account is less than the due amount, then system won’t do any liquidation and starts tracking the full due amount.

Whenever there is a credit to an account, the tracking process checks if the account has any receivable against it and if it does then the relevant amount is blocked as a receivable and the corresponding amount is marked to be used for settlement during subsequent ALIQ for the account. This process happens till the amount needed for liquidation is fully available.

The decision of allocating this credit will be based on the preference order of products that has been specified at an account class level. On the following EOD/BOD, batch liquidation tries to liquidate the schedule. The amount receivable is made available for the liquidation, and liquidation happens to the extent of receivable amount.

Manual Liquidation

Select this option to indicate that the Track receivable option is for Manual Liquidations.

Note

By default, the system selects this option

UDE Rate Plan

Start Date

The start date from which the rate plan change can be done is displayed here. However, you can modify this value at mortgage account level.

End Date

The end date till which the rate plan change can be done is displayed here. However, you can modify this value at mortgage account level.

Note

Based on the product maintenance, the ‘Rate Plan Change’ details are defaulted to the mortgage account and this can be modified.

Intermediary Details

You can capture the Intermediary Details at the account level to keep track of the accounts created through Intermediaries.

Intermediary Initiated

Check this box to indicate that the mortgage has been initiated by an intermediary.

Intermediary Code

If you have checked the box 'Intermediary Initiated', you need to specify the code of the intermediary who has initiated the mortgage. The adjoining option list displays all valid intermediary codes maintained in the system. You can select the appropriate one..

Note

Both the fields are disabled after the first authorization of the mortgage. They field cannot be modified during value-dated amendment and rollover operation.

Note that adjustment of commission and charge computed for the intermediary (in the past cycle) should be done manually in case of a reversal of any transaction done by the intermediary post the computation.

Provisioning Preference

You can define the provisioning preference of loan accounts by selecting the required option in Provisioning Mode.

Provisioning Mode

Select the Provisioning Mode preference of loan accounts from the drop-down list. The list displays the following options:

- Not Applicable

- Auto

- Manual

The provisioning mode option will get defaulted from Product level. However, you can switch between Auto to Manual mode or vice versa, but cannot change the mode as “Not Applicable” if defined as either Auto or Manual mode.

It is mandatory to select the provisioning mode as either ‘Auto’ or ‘Manual’ if CL product is created with a provision component. If CL product does not have provision component, then provisioning mode should be selected as 'Not Applicable'.

Loan Statements

You can specify the following details for generation of loan statements:

Start Date

Specify the start date of loan statement generation. Use the adjoining date button to choose a date from the calendar.

Frequency

Specify the frequency of loan statement generation. The drop-down list displays the following frequencies:

- Daily

- Monthly

- Quarterly

- Half Yearly

- Yearly

Choose the appropriate one.

Frequency Unit

Specify the frequency unit for loan statement generation.

If the above preferences are not maintained, the system generates loan statements based on the loan advices maintained in ‘Notices and Statements’ screen at the product level. If Loan Statement details are not maintained at the product level, the system will not allow you to set loan statement preferences for the contract. The system checks the product level preferences during EOD or BOD batches. You can also amend the loan statement preferences using ‘Value Date Amendment’ screen.

Holiday Periods

You can specify the following detail here:

Period

Select the period for which repayment holiday is to be given to the customer. The holiday periods maintained in the system are displayed in the adjoining option list. If the selected repayment holiday period exceeds ‘Interest Only Period’ field in the ‘Product’ screen, the system will display an appropriate error message.

For details on repayment holidays for amortized mortgages, please refer to the section ‘Repayment Holiday for Amortized Mortgages’ in this chapter.

Loan Settlement Notice

The system displays the following loan settlement details based on the values specified at ‘Value Dated Amendments’ level:

- Loan Settlement Request

- Notice Date

- Expected Closure Date

Status Change Mode

Select the status change mode. The options available are:

- Auto

- Manual

The system defaults Auto as the status change mode.

While processing End of Day, the system picks only those accounts with Auto as status change mode. The processing of the accounts which are picked up is based on the status options set at the product level.

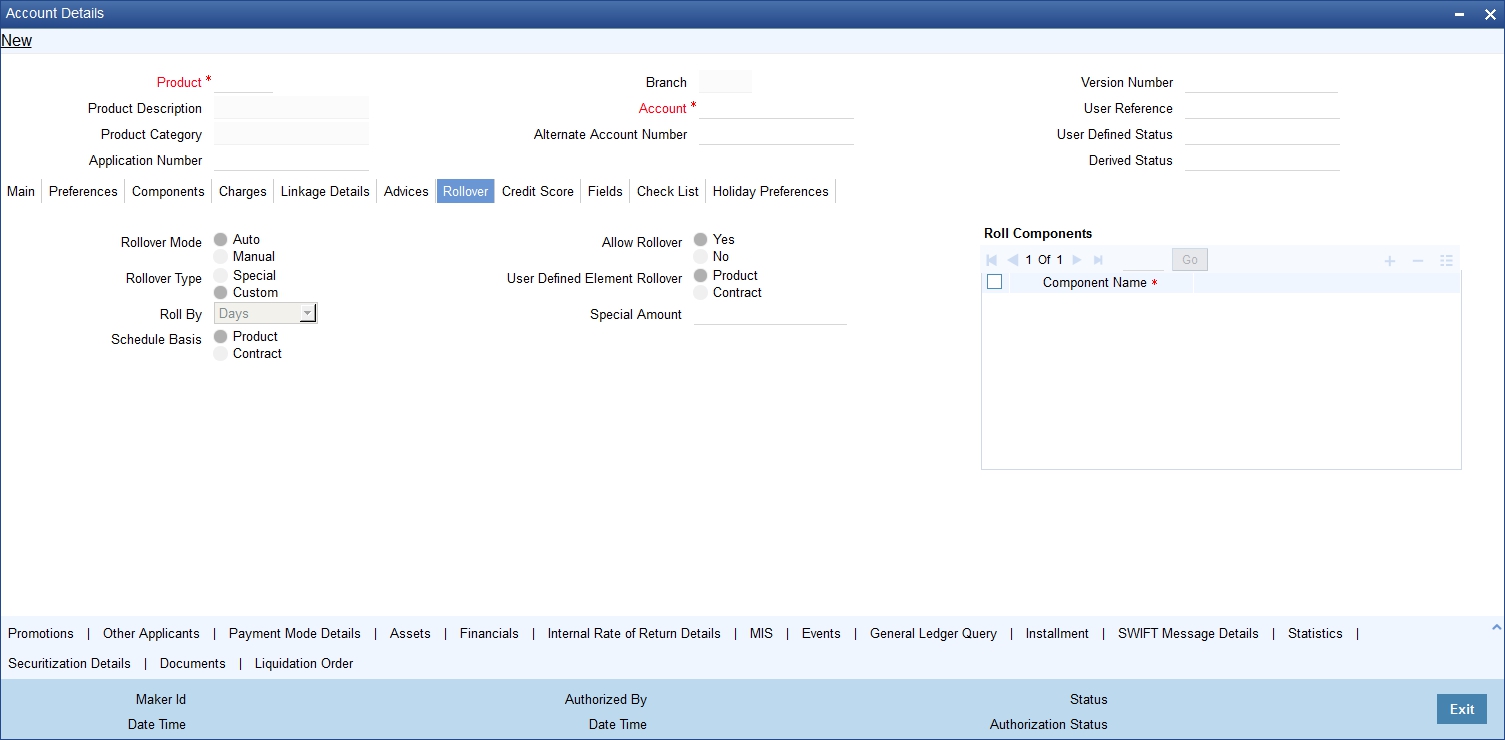

5.1.3.1 Rollover Tab

Click Rollover Tab to specify rollover details.

You can maintain the following details here:

Allow Rollover

Select the required option to indicate if rollover should be allowed for the mortgage or not. The options are:

- Yes

- No

Rollover

This option is used to determine if the Rollover is system driven or not .You can select either of the following options:

- Auto - If you select the option Auto Rollover, then upon maturity, the Account will be rolled over automatically by the system Rollover batch run in BOD.

- Manual - If you select the option Manual roll over, then the system does not perform the auto rollover and you can perform a manual rollover.

Note

By default, the system selects the ‘Auto’ option

Rollover Type

Select either of the following options:

- Special Amount: If your rollover is a special amount, select this option and capture the amount that has to be rolled over

- Custom: If the rollover type is ‘Custom’, then select the ‘Component Names’ that have to be rolled over

UDE Rollover

Select the required option to determine if at the time of rollover the UDE value would be defaulted from the product or from the account /Contract

Note

The system by default does not select the option Contract

Schedule Basis

This flag will determine if at the time of rollover the schedule would be defaulted from the product or from the account/Contract

Note

The system by default does not select the option Contract

Roll By

Specify the basis for rollover. It could be any of the following:

- Days

- Months

- Years

Rollover Components

You can maintain the following detail here:

Component

This option is applicable when Rollover Type is Custom. The option list provided will display the components relevant to the account from which you can choose the components that are to be rolled over.

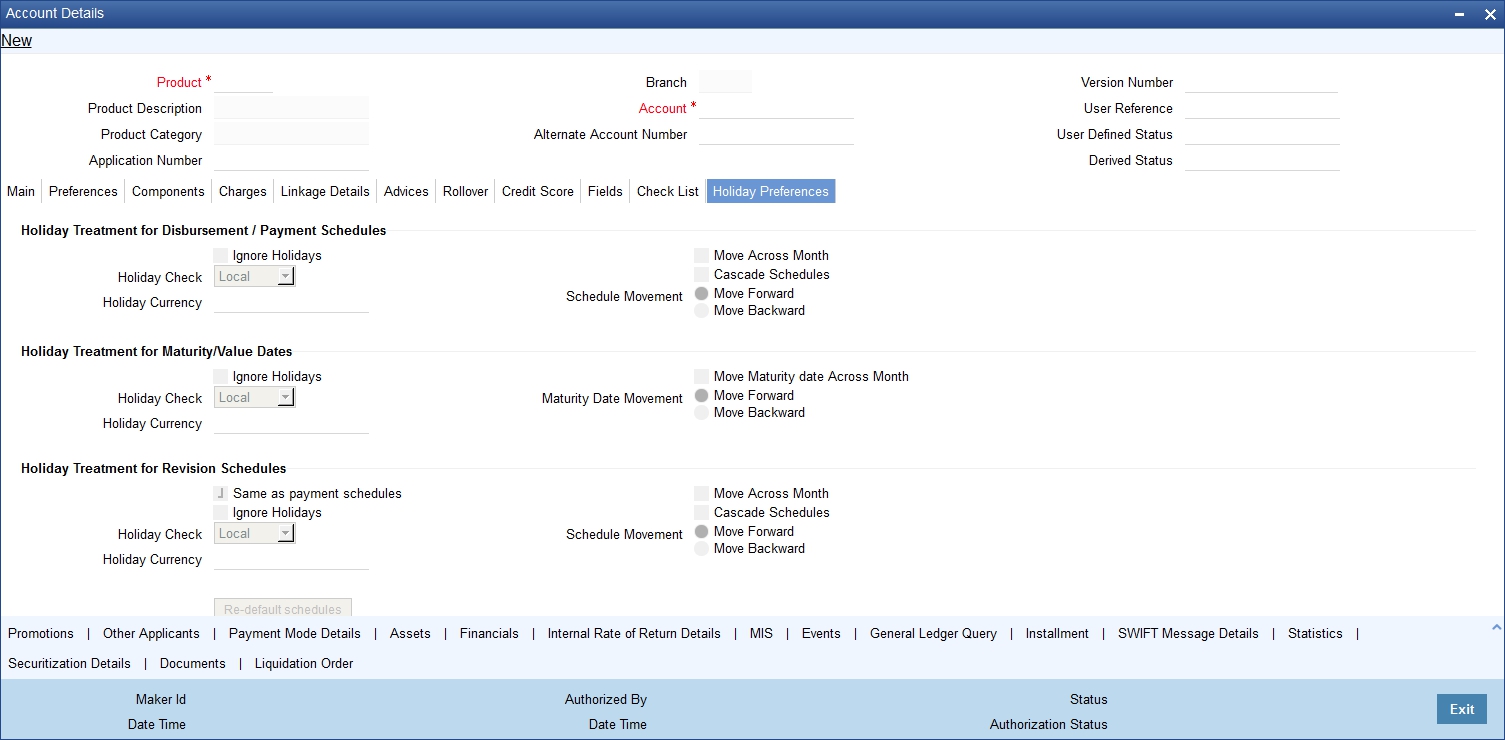

5.1.4 Holiday Preference Tab

Click on the ‘Holiday Preference’ tab to invoke the following screen: ..

You can specify the holiday preferences for Disbursement/Payment Schedule, Maturity/Value dates, and Revision schedules using this screen.

The values here are defaulted from the product screen. You can change the parameters before first authorization. After modifying the holiday parameter, you have to click the ‘Re-default’ button so that the schedule dates are rebuilt by the system.If maturity date is changed due to maturity date related holiday parameters then the system will do a product re-default.

If ‘Ad-hoc treatment required’ option is checked at the product level then ‘Cascade Schedules’ and ‘Ignore Holidays’ cannot be checked at the account level.

For more details on fields in this screen, refer the section titled ‘Holiday Preference Tab’ in Chapter ‘Defining Product Categories and Products’ in this user manual.

5.1.5 Check List Tab

The Check lists are maintained in the ‘Check List Maintenance’ screen and are linked to different events of the contract. The checklist maintained for the BOOK event is available in the Checklist tab at the time of account creation.

The following details are captured here:

Description

The description of the check list maintained for the BOOK event is displayed here

Verified

Check this box to indicate that the check list item has been verified

Remarks

Specify any additional remarks about the check list or the account in this free format text field

5.1.6 Fields Tab

The User Defined Fields are defined at the Product level. These fields are available in the Fields tab at the time of account creation.

The following details are displayed/captured here:

UDF Description

The UDF descriptions defaulted from the Product screen are displayed. The system displays all the UDF descriptions defined at the Product level

UDF Value

Specify the UDF value in this field. This is applicable only if the user input or list of values is defined at the time of creation of the UDF

5.1.7 Components Tab

Clicking against the ‘Components’ tab in the ‘Account Details’ screen invokes the following screen:

You can specify the following details for the components:

Component Name

After you specify the component Name, the system displays the description of the component in the adjacent field.

Component Ccy

The system displays the currency associated with the component in this field. The value is defined at Product level.

Special Interest Amount

Specify the amount for the special interest in this field

Settlement Ccy

Select the settlement currency for the option list. Click the adjoining option list to choose a settlement currency from the list of currencies. Double click on a value to select it.

In case of a subsidy mortgage, the system displays the settlement currency based on the subsidy customer ID specified in the ‘Main’ tab. However you can change it. The settlement currency is maintained as a default for both Credits and Debits.

Main component

The system selects the component of the mortgage designated as main component in the product level in this field

Verify Fund

You can indicate whether the system should verify the availability of sufficient funds in the customer account before doing auto liquidation of the component

Capitalized

Select this option if the scheduled amounts are to be capitalized

Waive

Select this option to waive the component for the account

Note

The system does not select it by default

Liquidation Mode

The system defaults the mode of liquidation from the product level. However you can modify the same to indicate the mode of liquidation of the component from the drop-down list. The following options are available for selection:

- Auto

- Manual

Note

This is applicable only if ‘Liquidation mode’ is selected as ‘Component’ at the account preference level.

Special Interest option

Select this option to denote if the component is a special Interest type. This implies that the computed value of the component can be overridden with the entered value

Internal Rate of Return Applicable

Check this option to indicate that the component is to be considered for IRR calculation for the account. This field is applicable to interest, charge and fee components. For adhoc charge, charge, penalty and prepayment penalty components, the value will be defaulted from the product level and you will not be able to modify it.

This field will not be available for input if ‘Accrual Required’ and ‘IRR Applicable’ are left unchecked at the product level.

Note

- For bearing type of component formula this option will be enabled only if ‘Accrual Required’ is checked for the component at the product level

- For discounted or true discounted type of component formula this option will be allowed irrespective of whether the ‘Accrual Required’ option is checked or not at the product component level

- If the option ‘Accrual Required’ is unchecked and ‘IRR Applicable’ is checked, then discounted component will be considered as a part of total discount to be accrued for Net Present Value (NPV) computation

- If both ‘Accrual Required’ and ‘IRR Applicable’ are checked, then discounted component will be considered for IRR computation

- Upfront Fee component will be considered for IRR only when ‘Accrual Required’ and ‘IRR Applicable’ both are checked

- For upfront fee component, if ‘IRR Applicable’ is checked, then ‘Accrual Required’ has to be checked

Funded During Initiation

This field indicates if the component can be funded during the INIT event.

Funded during Rollover

Select this option if the component can be funded during the rollover process.

Exponential Interest Method

Check this box for the system to validate the following for exponential interest method calculation:

- COMPOUND_VALUE SDE is maintained in book formula

- Compound days is maintained as one

Penal basis Comp options

The system displays the Penal basis for calculating penalty component in this field.

Service Branch

Click the option list to select the branch that services the customer account

Double click on a value to select it

Service Account

Click the option list to select the account in the service branch.

Double click on a value to select it.

All modes except CASA needs service account. Adjustments etc. will be settled through this account.

Schedule Definition

Click ‘Explode’ button to view the following Schedule details:

Schedule Number

The system generates and displays a sequential schedule number for installments

Due Date

The system displays the due date of the payments and disbursements in this field

Amount Settled

The system displays the settlement amount for the schedule in this field

Amount Due

The system displays the amount due for the schedule in this field

EMI Amount

The EMI that should be repaid in this schedule is displayed in this field

Amort Prin Details

The system displays the principal that has to be amortized in this field. This field will be relevant for the Interest component that is being amortized.

Accrued Amount

In this field, the system displays the amount accrued for the component for the schedule

Capitalize

The flag is used to display that the schedule installment is capitalized

Waive

Select this option to indicate if this particular amount which is due will be waived or not

Click ‘Edit’ to make any change to the scheduling and after you have made changes, click ‘Explode’ to see the changes made

If you select any component and click ‘Edit’ you can make changes to the schedules which are defaulted from the product to the account.

If you select the ‘Explode’ button, other components will get adjusted according to change made to any of the attribute.

For more details on ‘Schedule Summary’, refer section ‘Schedule Summary Definition’ under ‘Components Tab’ in ‘Account Creation’ Chapter of Retail Lending User Guide.

5.1.7.1 Viewing Rate Revisions

Select a component which has rate revision defined. To view the details of the Rate revision schedule, click the ’Revisions’ button. This lists the details of the revisions done on the Components.

This lists the revision date against the component name. This also has an application option which displays if the revision was applied or not.

You can check the details of the name of the component that is revised and the date when it has been revised from the field Component name and Revision date respectively.

5.1.7.2 Maintaining Payment Mode Details

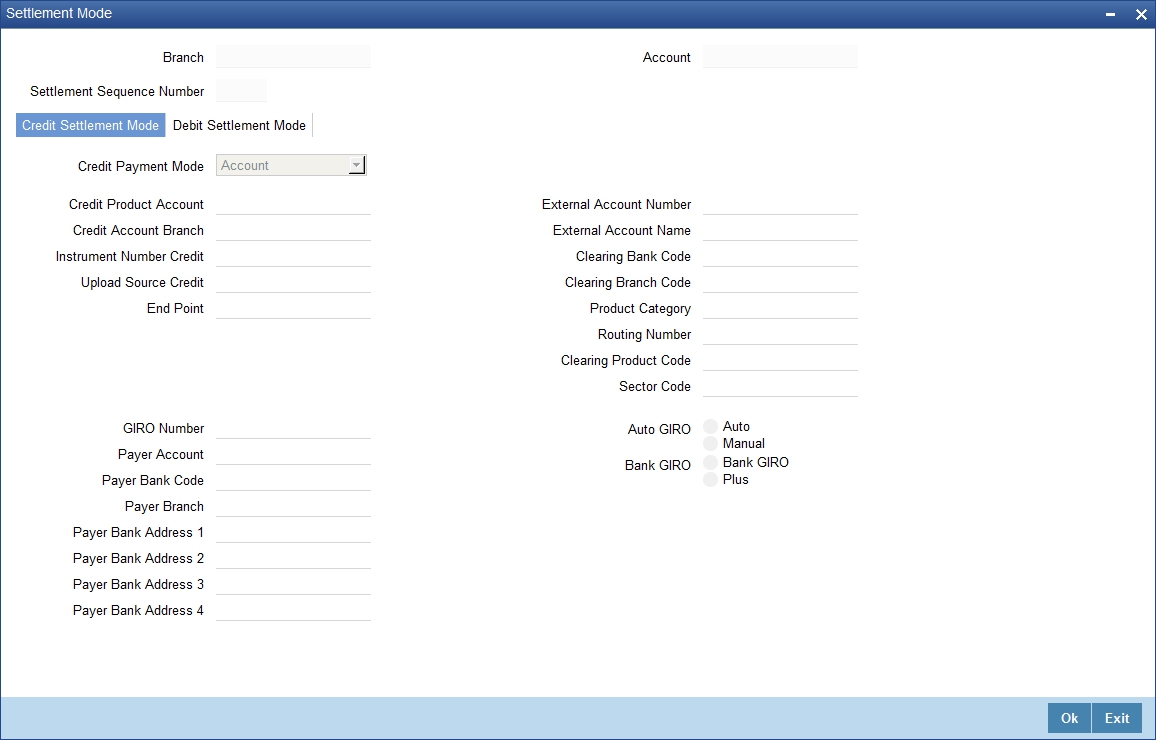

You can specify the details of payment mode in the ‘Settlement Mode’ screen. To invoke the screen, click ‘Payment Mode Details’ button under ‘Components’ tab in the ‘Account Details’ screen.

Here you can specify the following details:

Branch

Specify the branch in which the customer account resides.

Account

Specify the unique number of the account in the specified branch.

Settlement Sequence Number

The system displays the settlement sequence number during product default. You can change the value from the adjoining list of values.

If the sequence number is altered, click on Re-default Settlement button for settlement account to get re-defaulted. If re-defaulting is done for principal component, then the message details will also be modified based on the new sequence number chosen.

Note

During product default, payment mode is defaulted as ‘Account’ in case of multiple settlement sequence number.

Select the payment mode from the option list. The options for debit mode are CASA, Credit Card, Debit Card, Clearing, External Account, Electronic Pay Order, Internal Check, Instrument, GIRO and Cash/Teller.

The options for credit mode are CASA, Clearing, External Account, Instrument, and Cash/Teller.

The values in these modes are:

- CASA:

- Branch: Click the option list to choose the branch in which the customer account resides. . Double click on a branch to select it.

- Account: Click the option list to choose the account in the branch

selected. Double click on an account to select it. Credit Card / Debit

Card

- Card Number: This field captures either the Credit No or the Debit No details based on the selection.

The card must be a valid card whose number can be checked with a modulo logic or maintenance file.

- Clearing Network

- Clearing Bank Code: Click the option list to select the bank code as per clearing maintenance. Double click on a bank code to select it.

- Clearing Branch Code: Click the option list to select the clearing bank branch. Double click on a branch code to select it.

- Instrument No: Enter the number on the instrument presented for clearing in this field. Double click on a value to select it.

- Routing No: Enter the routing number of the branch selected for clearing in this field.

- Clearing Product Code: Click the option list to choose a product code if the clearing is using an Oracle FLEXCUBE clearing product. Double click on a branch to select it.

- End Point: This field picks up the end point maintained in the clearing system.

- Sector Code: Click the option list to choose the clearing sector code. Double click on a sector code to select it.

- External Account

- Clearing Bank Code: Click the option list to choose the external bank code as per clearing maintenance

- Clearing Branch Code: Click the option list to choose the external bank branch used for clearing

- Ext Acc No: Enter the external account number in this field

- Ext Acc Beneficiary Name: Enter the name of the beneficiary of the external account in this field

- GIRO

- Auto/Manual GIRO – Select Auto GIRO for automatic direct debit or else select Manual

- Bank/Plus GIRO – Select the GIRO clearing system used, which can be either Bank or Plus

- GIRO Number – This is applicable only for corporate customers and not for individual customers. You have to enter the GIRO number

- Payer Bank Name – Specify the name of the bank from which the amount is paid.

- Payer Branch - Specify the branch from which the amount is paid

- Payer Account - Specify the account from which the amount is paid

- Payer Bank Address - Specify the address of the bank from which the amount is paid

- Instrument / Cash / Teller

- AC Branch: Click the option list to choose branch where the account is serviced. Double click on a branch to select it

- Product or Account: If the payment mode is Account, this field specifies the CASA / GL account to be debited. If the payment is through Instrument / Cash, it denotes the teller product to be used

Credit Settlement Mode Tab

You can specify the credit settlement details under the ‘Credit Settlement Mode’ in the ‘Settlement Mode’ screen.

Here you can specify the following details:

Credit Payment Mode

Select the credit payment mode from the adjoining drop-down list. The list displays the following values:

- CASA

- Credit Card

- Clearing

- Debit Card

- External Account

- Electronic Pay Order

- GIRO

- Internal Cheque

- Instrument

- Cash/Teller

Credit Product Account

Specify the account number of the credit product.

Credit Account Branch

Specify the name of the branch in which the credit account should be maintained.

Instrument Number Credit

Specify the instrument number that should be used for credit payment.

Upload Source Credit

Specify the upload source that should be used for credit payment.

End Point

Specify the end point maintained in the clearing system. The adjoining option list displays all valid end points maintained in the system. You can choose the appropriate one.

External Account Number

Specify the external account number.

External Account Name

Specify the name of the beneficiary who is holding the external account.

Clearing Bank Code

Specify the code of the external bank that should be used for clearing maintenance. The adjoining option list maintains all valid banks maintained in the system. You can choose the appropriate one.

Clearing Branch Code

Specify the branch code of the specified external bank that should be used for clearing. The adjoining option list displays all valid codes maintained in the system. You can choose the appropriate one.

Product Category

Specify the category of the product. The adjoining option list displays all valid products maintained in the system. You can choose the appropriate one.

Routing Number

Specify the routing number of the specified branch for clearing.

Clearing Product Code

Specify the product code that should be used for clearing. The adjoining option list displays all valid code maintained in the system. You can choose the appropriate one.

Sector Code

Specify the code of the sector that should be used for clearing. The adjoining option list displays all valid codes maintained in the system. You can choose the appropriate one.

Giro Number

Specify the GIRO number of the corporate customer.

Payer Account

Specify the account from which the amount should be paid.

Payer Bank Code

Specify the code of the payer’s bank that should be used for the payment of amount.

Payer Branch

Specify the branch of the specified payer’s bank that should be used for the payment of amount.

Payer Bank Address 1-4

Specify the address of the bank that should be used for the payment of the amount.

Bank Giro

Indicate the type of bank giro that should be used for corporate customers. You can select one of the following:

- Bank GIRO

- Plus

Auto Giro

Indicate the type of the Auto GIRO for automatic direct debit. You can select one of the following values:

- Auto

- Manual

Original Exchange Rate

The base or actual exchange rate between the account currency and settlement currency gets displayed here.

Exchange Rate

For a customer availing any Relationship Pricing scheme, the customer specific exchange rate derived by adding the original exchange rate and the customer spread maintained for the relationship pricing scheme gets displayed here.

You can change the defaulted rate provided the change is within the variance level maintained for the underlying product.

If Relationship Pricing is not applicable, Exchange Rate will be the same as the Original Exchange Rate.

For more details on customer specific exchange rates, refer the section titled ‘Specifying Pricing Benefit Details’ in Relationship Pricing user manual.

Negotiated Cost Rate

Specify the negotiated cost rate that should be used for foreign currency transactions between the treasury and the branch. You need to specify the rate only when the currencies involved in the transaction are different. Otherwise, it will be a normal transaction.

The system will display an override message if the negotiated rate is not within the exchange rate variance maintained at the product.

Negotiation Reference Number

Specify the reference number that should be used for negotiation of cost rate, in foreign currency transaction. If you have specified the negotiated cost rate, then you need to specify the negotiated reference number also.

Note

Oracle FLEXCUBE books the online revaluation entries based on the difference in exchange rate between the negotiated cost rate and transaction rate.

Debit Settlement Mode Tab

You can specify the debit settlement details under the ‘Debit Settlement Mode’ in the ‘Settlement Mode’ screen.

Here you can specify the following details:

Debit Payment Mode

Select the Debit payment mode from the adjoining drop-down list. The list displays the following values:

- CASA

- Credit Card

- Clearing

- Debit Card

- External Account

- Electronic Pay Order

- GIRO

- Internal Cheque

- Instrument

- Cash/Teller

Debit Product Account

Specify the account number of the debit product.

Debit Account Branch

Specify the name of the branch in which the debit account should be maintained.

Instrument Number Debit

Specify the instrument number that should be used for debit payment.

Upload Source Debit

Specify the upload source that should be used for debit payment.

End Point

Specify the end point maintained in the clearing system. The adjoining option list displays all valid end points maintained in the system. You can choose the appropriate one.

External Account Number

Specify the external account number.

External Account Name

Specify the name of the beneficiary who is holding the external account.

Clearing Bank Code

Specify the code of the external bank that should be used for clearing maintenance. The adjoining option list maintains all valid banks maintained in the system. You can choose the appropriate one.

Clearing Branch Code

Specify the branch code of the specified external bank that should be used for clearing. The adjoining option list displays all valid codes maintained in the system. You can choose the appropriate one.

Product Category

Specify the category of the product. The adjoining option list displays all valid products maintained in the system. You can choose the appropriate one.

Routing Number

Specify the routing number of the specified branch for clearing.

Clearing Product Code

Specify the product code that should be used for clearing. The adjoining option list displays all valid code maintained in the system. You can choose the appropriate one.

Sector Code

Specify the code of the sector that should be used for clearing. The adjoining option list displays all valid codes maintained in the system. You can choose the appropriate one.

Payer Account

Specify the account from which the amount should be paid.

Payer Bank Code

Specify the code of the payer’s bank that should be used for the payment of amount.

Payer Branch

Specify the branch of the specified payer’s bank that should be used for the payment of amount.

Payer Bank Address 1-4

Specify the address of the bank that should be used for the payment of the amount.

Giro Number

Specify the GIRO number of the corporate customer.

Bank Giro

Indicate the type of bank giro that should be used for corporate customers. You can select one of the following:

- Bank GIRO

- Plus

Auto Giro

Indicate the type of the Auto GIRO for automatic direct debit. You can select one of the following values:

- Auto

- Manual

Original Exchange Rate

The base or actual exchange rate between the account currency and settlement currency gets displayed here.

Exchange Rate

For a customer availing any Relationship Pricing scheme, the customer specific exchange rate derived by adding the original exchange rate and the customer spread maintained for the relationship pricing scheme gets displayed here.

You can change the defaulted rate provided the change is within the variance level maintained for the underlying product.

If Relationship Pricing is not applicable, Exchange Rate will be the same as the Original Exchange Rate.

For more details on customer specific exchange rates, refer the section titled ‘Specifying Pricing Benefit Details’ in Relationship Pricing user manual.

Negotiated Cost Rate

Specify the negotiated cost rate that should be used for foreign currency transactions between the treasury and the branch. You need to specify the rate only when the currencies involved in the transaction are different. Otherwise, it will be a normal transaction.

The system will display an override message if the negotiated rate is not within the exchange rate variance maintained at the product.

Negotiation Reference Number

Specify the reference number that should be used for negotiation of cost rate, in foreign currency transaction. If you have specified the negotiated cost rate, then you need to specify the negotiated reference number also.

Note

Oracle FLEXCUBE books the online revaluation entries based on the difference in exchange rate between the negotiated cost rate and transaction rate.

5.1.8 Charges Tab

This module is used for calculating and applying charges on an account. To calculate the charges that we would like to levy on an account, we have to specify the basis on which we would like to apply charges. For example, we may want to apply charges on the basis of the debit turnover in an account. When we define a Charge product, we have to specify the Charge basis.

When we apply the charge product on an account or an account class, charges for the account will be calculated on this basis.

The following details are captured:

Component Name

Here, you can add a brief description for the component that you specify for a product

Calculation Type

To specify the manner in which the component should be calculated and liquidated. You can choose one of the following options:

Formula with schedule (Component Type - Interest)

- Formula without schedule (Charge)

- Penal Interest

- Prepayment Penalty

- Discount

- Schedule without formula (Principal)

- No schedule No formula (Ad Hoc Charges)

- Penalty Charges

Component Currency

The system displays the currency associated with the component. The component currency is defaulted from the Product level

Settlement Currency

Click the option list to choose the details of the currency in which the payments are to be made in this field. A list of currencies is displayed. Double click on a value to select it.

5.1.8.1 Maintaining Payment Mode Details

The debit and credit settlement mode details for the account can be maintained in the ‘Settlement Details’ screen. You can invoke this screen by clicking the ‘Payment Mode’ button in the ‘Main’ tab.

Specify the following details:

Dr Payment Mode

Click the option list to choose the details of the mode of payment (For debit payments) in this field. A list of values includes CASA, Cash/Teller, Instrument, External Account, Electronic Pay Order, Internal Check, Clearing, Debit Card and Credit Card.

Dr Prod Ac

Enter the Product / Account to be used for Debit payments in this field

Dr Acc Brn

Click the option list to choose the details of the branch where the Dr account resides. A list of values is displayed. Double click on a value to select it

Cr Payment Mode

Click on list item to choose the mode of payment by which the account is credited. The list of values includes a list of values which includes CASA, Cash/Teller, Instrument, External Account, and Clearing.

Cr Prod Ac

Enter the details of the Product/Account to be used for Credit payments in this field

Cr Acc Brn

Click the option list to choose the details of the branch where the Cr account resides. A list of values is displayed. Double click on a value to select it.

Charge Appl Date

Enter the details of the date from which the charge is applicable in this field

Service Branch

The branch that services the account - Any Valid, Open Branch

Service Account

Denotes valid open account in the service branch. The service account is needed for all modes apart from CASA. The adjustments etc will be settled through this account.

Due Date

The date on which the charge was applied.

Amount Due

Enter the details of the amount due for repayment in this field

Funded during INIT

Select this option if the component can be funded during mortgage initiation

Funded during Rollover

Select this option if the component can be funded during the rollover process

For each component, the following details are displayed:

- Event Code

- Component Name: A component will be of type ‘Charge’

- Amount Due: The amount due for repayment in this field

- Amount Settled: The settled amount in this field

- Schedule Due Date: The scheduled date for repayment in this field

- Waive: If this option is checked, the charge defined for event is waived off

Waiver Flag

Select this option to waive off the charges

Refer ‘Maintaining Payment Mode Details’ section in this User Manual for field explanations.

5.1.9 Linkages Tab

At the time of Mortgage account capture, the Linkages to securities backing the mortgage is captured. They include:

- The reference number of the Local Collateral,Line, Account, Amount block, Commitment, Guarantee Collection Bill is linked

- The amount which is attributed to the particular reference number is also captured

- The account input screen captures the Linkages as shown below

You can link Limit/Commitment to the Mortgage account during CL account creation.

You can specify the following Linkage details:

Linkage Sequence Number

Enter the sequence number for the linkage that you are specifying

Linkage Type

Select a type of linkage to which you need to link the specified account from the adjoining drop-down list. This list displays the following values:

- Facility – Select if you need to link the account to a facility.

- Local Collateral – Select if you need to link the account to local collateral.

- New Collateral – Select if you need to link the account to new collateral.

Linkage Branch

Select the branch of the linkage type

Customer ID

Click on ‘C’ button to choose the ID of the customer to be used for corresponding linkage type. A list of values is displayed. Double click on a value to select it.

A customer can either be the primary applicant or any of the other applicants for which the linkage type has been maintained.

Linkage Ref No

Click on ‘L’ button to choose linkage reference number be used for corresponding field.

Linkage Amount

Enter the linkage amount in this field.

Linked Currency

Specify the linked currency.

Link%

Specify the linkage percentage.

Block Reference No

On save the system displays the block reference number.

Secured Portion

Enter the part of the principal that is backed by some asset in this field.

On save:

- the system validates the linked amount with term deposit available balance. If the term deposit available balance is less than the linkage amount, then the system displays an error message.

- the system marks a lien on the term deposit by the linkage amount with 'Amount Block Type' as 'Loan' and 'Reference No' as Loan account number.

5.1.10 Advices Tab

Advices that may be generated whenever the account level status changes or whenever a particular event is fired can be linked at the Product level. Priorities of the advice can be changed and also a particular advice for an event can be suppressed. Generation of an advice across the life of the account can also be suppressed.

You can specify the following Advice details:

Message Type

The system displays all the advices for all the events for the account. The list will include all the advices that are defined at the product level

Suppress

This field allows the user to suppress the generation of the advice for a particular event. The options are Yes or No

Priority

Click the option list to select the priority of generation. A list of values is displayed. Double click on a value to select it.

The options are High, Medium or Low

Suppress Advices across the Account

The generation of an advice across the life of the account can be suppressed.

Message Type

Click the option list to select the type of advice, the generation of which can be suppressed across the account. A list of values is displayed. Double click on a value to select it.

The list includes advices defined at the product level

You can suppress the Payment Message defaulted in case you do not need a credit through swift message.

The message is automatically suppressed if the Principal Credit Settlement account is changed to a GL or if the receiver in ‘Swift Msg Details’ screen is not valid to receive the message i.e, if the Customer Type of the Receiver party is not a Bank.

Also, if the settlement mode for PRINCIPAL component is anything other than CASA, the swift message is automatically suppressed.

If the Transfer Type is chosen as blank i.e, neither Customer Transfer nor Bank Transfer, then PAYMENT_MESSAGE will become CREDIT_ADVICE by Swift(MT910) if the Receiver is a bank and the credit settlement account is a current account.

5.1.11 Credit Score Tab

Click ‘Credit Score’ tab to specify the details for calculating the credit score.

You need to specify the following details here:

Rule Name

The rule associated with the mortgage product gets defaulted here. You can modify this, if required.

Credit Score

Specify the credit score associated with the customer

Automated Score

The credit score calculated by the system based on the rules maintained at the product level gets displayed here

Agency Code

Select the code of the external agency, to be approached for calculating the score

External Credit Score

The score as calculated by the external agency is displayed here

Click ‘Score’ to auto-generate the credit score for the customer. Click ‘External Score’ to auto-generate the credit score for the Bureau.

5.1.12 Specifying Other Applicants Details

You can maintain the primary and other applicants details in the ‘Other Applicants’ screen. Click the ‘Other Applicants’ button to invoke the screen.

Primary Applicant

You can maintain the following details of the Primary applicants:

Customer ID

This detail is defaulted from the main screen. Enter the Customer ID of the primary applicant in this field

Customer Name

After you enter the Customer ID, the system displays the Name of the primary applicant in this field

Other Applicants

The details of the liability parties to the account are maintained in this field. Other Applicants of a mortgage include Co-signers and Guarantors.

You can specify the following details of the Co-applicants:

Customer ID

To select the customer ID of the co-applicant, click the option list. A list of customer IDs is displayed. Double click to select the customer ID of the co-applicant.

Customer Name

After you enter the name of the Customer, the system displays the name of the customer in this field.

Responsibility

Select the details of the co-applicants and their responsibility as a Co-signer or as a guarantor from the option list. You can enter the details like the guarantor, co-signer, main addressee, advice notice receiver, and borrower etc., who is relevant to a joint account relationship. During initiation of the account, the primary customer is defaulted to ‘Borrower’ with 100% Liability and value date as the effective date. You are allowed to maintain multiple applicants (customer id) for a mortgage with the same responsibility (Borrower).

Note

While there is no processing impact, the difference will become important when the original debtor is absconding and the mortgage is unpaid etc.

Liabilities%

Specify the contribution of the co-applicants to the Mortgage. You can specify the Liability of the co-applicant if any, in case of a Mortgage default. You can also specify the percentage of interest split among different co-applicants. It is not made mandatory to maintain ‘Liability %’ for the responsibility ‘Borrower’. There could be borrowers with 0% liability.

Note

The sum of ‘Liability %’ for all the customers of a mortgage to be equal to 100%

Liability Amount

The system calculates and displays the upper limit of the liability in terms of the amount in this field. You may override the computed value.

Effective Date

This field is used to capture the date from which the % interest split among co-applicants of the mortgage will be taken into consideration. During the initiation of the mortgage, the value date of the mortgage will be defaulted as the effective date. During VAMI, the same effective date will be retained, you can however edit it.

Note

The effective date can not be a date prior to the mortgage initiation date. It is also necessary that there is one record for the initiation date. The effective date for all the applicants is the same.

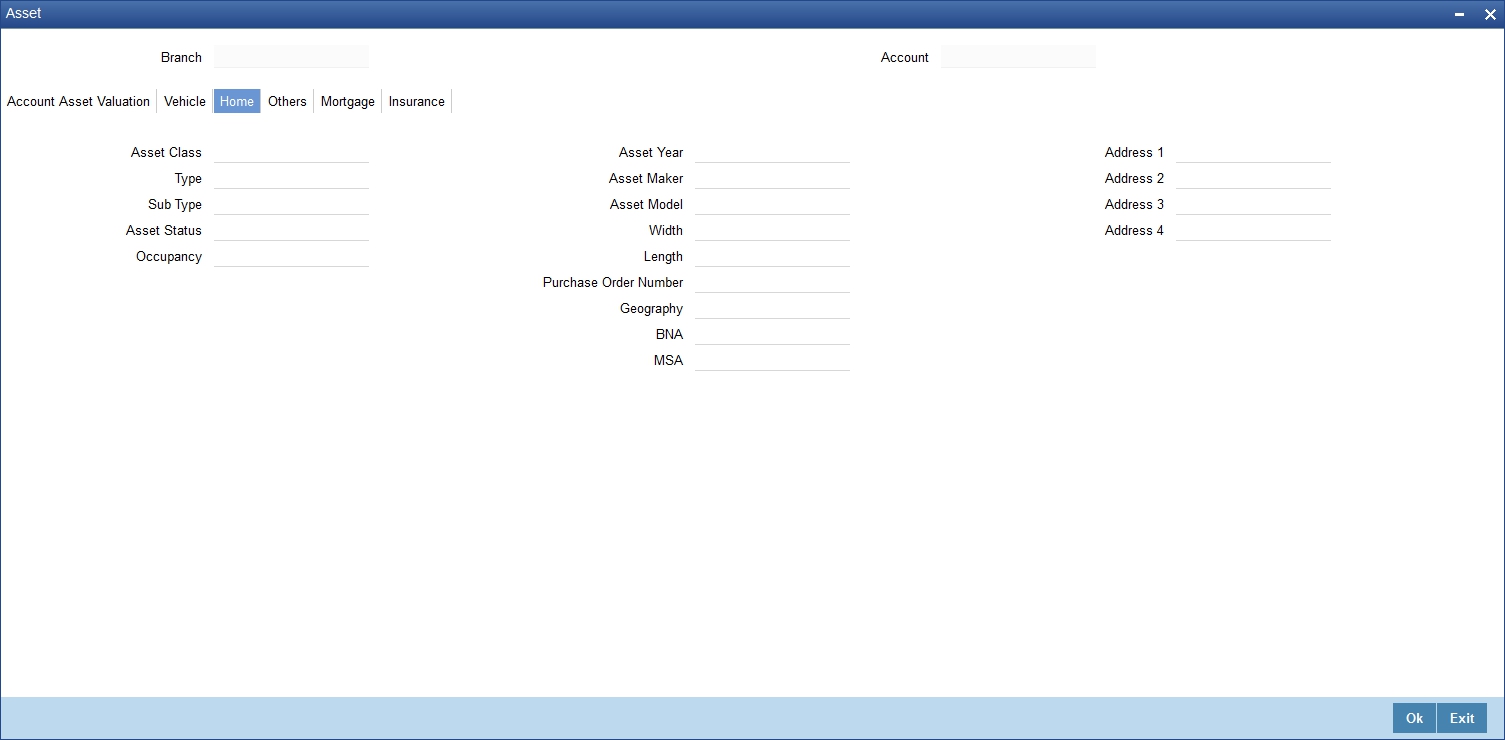

5.1.13 Capturing Asset Details

You can capture the details corresponding to the collateral being provided for the current mortgage in the ‘Assets’ screen. To invoke this screen, click ‘Assets’ button in the ‘Account Details’ screen.

5.1.13.1 Valuations Tab

You can capture valuation details of the asset in this tab:

Here, you can specify the following details related to your assets like vehicle, home, etc.

Assets

Select the type of asset from the drop-down list. The following values are provided for selection:

- Vehicle

- Home

- Others

Valuation Dt

Specify the valuation date for the selected asset, or select the date by clicking the ‘Calendar’ button.

Source

Specify the source associated with the asset selected

Supplement

Specify the supplement of the valuation source used for the valuation

Edition

Specify edition of the valuation source used for the valuation

Wholesale

Specify the wholesale rate associated with the asset selected

Retail

Specify the retail rate associated with the asset selected

Usage

Specify usage level at the time of the valuation

Usage Value +

Specify the initial usage value

Total

Specify the total usage of the asset

5.1.13.2 Vehicle Tab

You can capture details regarding the asset of type ‘vehicle’ in this tab.

You can specify the following common details associated with asset of type vehicle:

Class

Select the class associated with the asset selected, from the option list. The following options are provided:

- New

- Used

Status

Select the status of the asset selected, from the option list. The following options are provided:

- Active

- Inactive

- Inventory

- Undefined

Type

Specify the type of the selected asset here

Sub Type

Specify the subtype associated with the asset, if any

Year

Specify the year of association with the selected asset

Make

Specify the make of the selected asset. For vehicle, you can specify the manufacturing company name and for home you can specify the name of the builder or developer.

Model

Specify the model of the selected asset

Address

Specify the address associated with the asset

You need to specify the following details additional related to vehicle type of asset:

Body

Specify the body number associated with the vehicle

Id Number

Specify the unique identification number associated with the vehicle

Reg. Number

Specify the registration number of the vehicle

5.1.13.3 Home Tab

You can capture details regarding the asset of type Home in this tab.

You can specify the following additional details for home type of asset:

Occupancy

Specify the number of people occupying the house

Width

Specify the width associated with the selected asset

Length

Specify the length associated with the selected asset

PO #

Specify the post office number of the location of the property

GEO

Specify the property GEO code (Geospatial Entity Object Code) for the asset

BNA

Specify the census tract/BNA code (Block Numbering Area) for the asset

MSA

Specify the metropolitan statistical area (MSA) code for the asset

Click ‘Ok’ to save the details.

5.1.13.4 Others Tab

You can capture other asset details here.

Specify the following details:

- Asset Class

- Type

- Sub Type

- Asset Status

- Asset Year

- Asset Make

- Asset Model

- Asset Body

- Identity Number

- Register Number

- Address

5.1.13.5 Mortgage Tab

You can capture other asset details here.

Property Name

Specify the name of the property of the mortgage loan.

Collateral Category

Specify the type of the collateral offered to the bank.

Property Age (In Years)

Specify the age details of the property of the mortgage loan.

Country

Specify the name of the country where the property is located.

Co-owner

Specify the name of co-owner of the property.

Offset Margin

Specify the offset margin of the mortgage property.

Lendable Margin

Specify the lendable margin of the mortgage property.

Valuation Currency

Specify the currency in which the property has to be valued. This adjoining option list displays all valid currencies maintained in the system. You can choose the appropriate one.

Valuation

Specify the actual value of the property.

Property Address

Specify the address details of the property. You can use four address fields to capture the complete address.

Project Details

You can specify the project details in the following fields:

Developer Code

Specify the code that identifies the developer of the property.

Project Name

Specify the name of the project under which the property was constructed.

Project Description

Specify a brief description of the specified project.

Evaluator

Specify the name of person who evaluates the property.

Evaluation Value

Specify the worth of the property that is evaluated by the evaluator.

Evaluation Date

Specify the date on which the evaluation is done by the specified evaluator.

Requested Amount

Specify the amount that is requested by the customer.

Property Usage

Specify the usage of the property.

Mortgage Degree

Specify the degree of the mortgage.

Lot Number

Specify the lot number of the property.

Property Type

Specify the type of the property. The following are the different types of properties:

- Land

- Apartment

- Villa

Property Status

Specify the status of the property.

Title Deed Number

Specify the deed number of legal document on the purchased property.

Title Deed Issue Date

Specify the date on which the legal document is issued.

Title Deed Issue From

Specify the name of the authority who issued the legal document on the property.

Building Name

Specify the name of the building.

Building Compound Name

Specify the name of the building compound.

Contact Person

Specify the name of the contact person.

Contact Number

Specify the contact number of the developer.

Wing Name

Specify the portion name of the property.

Asset Finance Amount

Specify the finance amount of the property asset.

Property Value

Specify the worth of the property.

Down Payment

Specify the amount that should be paid as down payment.

Market Value

Specify the current market value of the property.

Sale Value

Specify the sale value of the property that should be used for the secondary market purchase.

Registered Name

Specify the name of the person to whom the property should be registered.

Registration Number

Specify the registration serial number of the property.

Registration Date

Specify the date on which the property should be registered.

Completion Date

Specify the date on which the project should be completed.

5.1.13.6 Insurance Tab

You can capture details regarding the asset of type Insurance in this tab.

Here you can specify the following details:

Policy Number

Specify the insurance policy number.

Policy Type

Specify the type of the policy. The following are the different types of polices:

- Property Insurance

- Life Insurance

Insurer

Specify the name of the insurance company.

Insurer Address 1 to 4

Specify the address of the insurance company. You can use four address fields to capture the complete address.

Insurance Expiry

Specify the date on which the insurance policy expires. Click the date button to choose a date from the calendar.

Customer

Specify the name of the primary customer.

Policy Amount

Specify the amount insured on the policy.

Policy Start Date

Specify the start date of the insurance policy. Click the date button to choose a date from the calendar.

Policy End Date

Specify the end date of the insurance policy. Click the date button to choose a date from the calendar.

Premium Amount

Specify the yearly premium amount being paid for this insurance.

Insured Name

Specify the name of the person insured under this policy.

Managed by

Specify the name of the person who manages the insurance policy. If an insurance broker manages the policy, enter the name of the broker.

Note

Oracle FLEXCUBE changes the undisbursed DSBRs to moratorium using VAMI options.

The system also collects the processing fee in advance and runs along with the BOOK/DSBR events.

For more details on the additional links, refer the section titled ‘Creating a Loan Account’ in Retail Lending user manual.

5.1.14 Repayment Holiday for Amortized Mortgages

A mortgage has two formulae for the slots of simple and the amortized. Simple and amortized formulae can occupy any position in schedules definition.

During principal repayment holiday period, interest is calculated on the simple interest formula specified. The customer needs to repay only the interest component. Principal is amortized for the remaining period or tenor of the mortgage. Principal schedule will not be present during repayment holiday period.

The system treats instances of overdue and default as per the liquidation order maintained.

For example, consider the following details:

|

|

Mortgage Amount |

24000 |

Tenor of Mortgage |

24 months |

Rate of Interest |

20% |

Simple Calculation Period |

06 |

Amortized Calculation Period |

18 |

Mortgage start Date |

01-Sep-2008 |

Mortgage End Date |

01-Sep-2010 |

Interest Calculation Amortized |

From 01-Sep-2008 to 01-Sep-2009 |

Interest Calculation Simple |

From 01-Sep-2009 to 01-Mar-2010 |

Interest Calculation Amortized |

From 01-Mar-2010 to 01-Sep-2010 |

Sl No |

Instalment Schedule Date |

Mortgage Outstanding Amount |

Instalment Amount |

Repayment |

|

Principal |

Interest |

||||

1 |

10/1/2008 |

9482.13 |

601.2 |

517.87 |

83.33 |

2 |

11/1/2008 |

8962.58 |

601.2 |

519.55 |

81.65 |

3 |

12/1/2008 |

8436.07 |

601.2 |

526.51 |

74.69 |

4 |

1/1/2009 |

7907.51 |

601.2 |

528.56 |

72.64 |

5 |

2/1/2009 |

7374.4 |

601.2 |

533.11 |

68.09 |

6 |

3/1/2009 |

6830.56 |

601.2 |

543.84 |

57.36 |

7 |

4/1/2009 |

6288.18 |

601.2 |

542.38 |

58.82 |

8 |

5/1/2009 |

5739.38 |

601.2 |

548.8 |

52.4 |

9 |

6/1/2009 |

5187.6 |

601.2 |

551.78 |

49.42 |

10 |

7/1/2009 |

4629.63 |

601.2 |

557.97 |

43.23 |

11 |

8/1/2009 |

4068.3 |

601.2 |

561.33 |

39.87 |

12 |

9/1/2009 |

3502.13 |

601.2 |

566.17 |

35.03 |

13 |

10/1/2009 |

3502.13 |

29.18 |

|

29.18 |

14 |

11/1/2009 |

3502.13 |

30.16 |

|

30.16 |

15 |

12/1/2009 |

3502.13 |

29.18 |

|

29.18 |

16 |

1/1/2010 |

3502.13 |

30.16 |

|

30.16 |

17 |

2/1/2010 |

3502.13 |

30.16 |

|

30.16 |

18 |

3/1/2010 |

3502.13 |

27.24 |

|

27.24 |

19 |

4/1/2010 |

2931.09 |

601.2 |

571.04 |

30.16 |

20 |

5/1/2010 |

2354.32 |

601.2 |

576.77 |

24.43 |

21 |

6/1/2010 |

1773.39 |

601.2 |

580.93 |

20.27 |

22 |

7/1/2010 |

1186.97 |

601.2 |

586.42 |

14.78 |

23 |

8/1/2010 |

595.99 |

601.2 |

590.98 |

10.22 |

24 |

9/1/2010 |

0 |

601.12 |

595.99 |

5.13 |

Repayment amounts marked in ‘italics’ are derived using amortized formula. The remaining amounts are derived using simple formula.