3. Building Interest Classes

A class is a specific type of component that can be built with certain attributes. This chapter explains how interest classes are built and how attributes are defined.

When building an interest class, certain attributes, such as the following can be defined:

- The module in which you would use the class

- The interest type

- The association event

- The basis amount on which the interest is paid

- The rate type

- The default rate code (for floating interest)

- The default tenor

This chapter contains the following sections:

- Section 3.1, "Introduction"

- Section 3.2, "Specifying Currency-wise Limits for Interest Rate Application"

- Section 3.3, "Processing CPR (Conditional Prepayment Rate) Loans"

- Section 3.4, "Calculating Loan Interest Accrual on Principal Outstanding"

- Section 3.5, "Calculating Interest for Interest Basis '30SPL/360’"

- Section 3.6, "Rate Conversion Processing"

3.1 Introduction

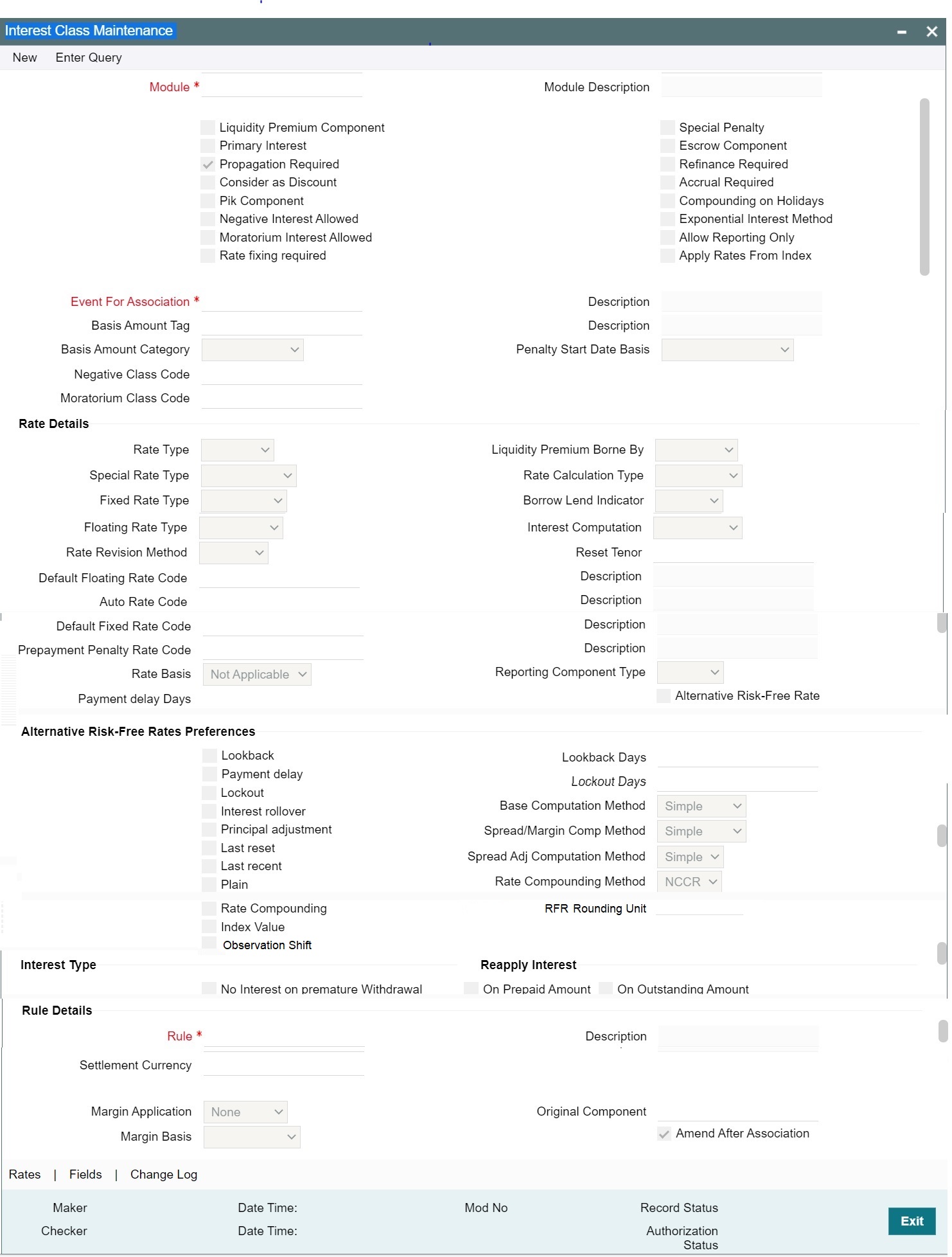

You can define the attributes of an interest class, in the ‘Interest Class Maintenance’ screen.

You can access this screen by typing LFDINTCL in the field at the top right corner of the Application tool bar and clicking the adjoining arrow button.

Before defining the attributes of an interest class, you should assign the class a unique identifier, called the Class Code and briefly describe the class. A description would help you easily identify a class.

An interest class is built for use in a specific module. This is because; an interest component would be applied on different basis amounts, in different modules.

Note

Basis Amount Tags available would depend on the module for which you build the class.

Events

The term Event can be explained with reference to a deal. A deal goes through different stages in its life cycle, such as:

- Contract Booking

- Money Settlement of contract

- Reversal of a contract

- Cancellation of a contract

Each stage is referred to as an Event in Oracle Lending.

The event at which you would like to associate the interest component, being defined, to a contract is referred to as the Association Event.

Basis Amount Tag

The basis on which an interest is calculated is referred to as the Basis Amount. When building an interest class, you have to specify the tag associated with the Basis Amount.

The attributes defined for an interest class, will default to all products with which you associate the class. When maintaining interest details for a product, you can change these default attributes. Contracts maintained under a product will acquire the attributes defined for the loan product.

Note

The amount tag ‘SCH_AMT_OS’ is the basis for calculation of late payment charge. It constitutes the total amount outstanding across all components due on a particular schedule date, provided late payment charge is applicable to these components. If you select the Basis Amount Tag as ‘SCH_AMT_OS’, then the following check boxes are disabled:

- Primary Interest

- Consider as Discount

- PIK Component

Specifying rate fixing

Select this check box to indicate whether the rate fixing is applicable for a particular component. This is applicable for Bilateral Loans and Loan Syndications.

Moratorium Interest Allowed and Moratorium Class code

In case 'Moratorium Interest Allowed' check box is selected for main interest component, then on save the system creates 'Moratorium Class Code' ('Class Code' field value is appended with _M).

Note

If 'Rate Type is 'Floating' for main component, then the system creates moratorium interest component with 'Fixed/Userinput'.

Specifying the amount category

Indicate the category of the component on which the interest has to be applied. The available options are:

- Expected

- Overdue

- Normal

- Outstanding

- Overdue OS

- Sch-Overdue

If Normal is selected, the balance on which interest has to be applied will be the Expected Balance (assuming that all the scheduled repayments, defined for the contract, are made on time). An example of this category is the application of interest on the principal of a loan.

If Overdue is selected, the balance on which interest has to be applied will be the amount that is outstanding, based on the repayment schedule defined for the contract. An example of this category is the application of penalty interest, on the principal or interest, when a repayment has not been made as per the schedule.

If Outstanding is selected with the amount category as principal, the interest is calculated on the balance of the total principal outstanding amount.

If Overdue OS is selected with the amount category as principal, the interest is calculated on the principal overdue outstanding.

If SCH-Overdue is selected, then the basis amount refers to amount outstanding on a particular schedule due date. If you select the ‘Basis Amount Tag’ as ‘SCH_AMT_OS’, then system defaults the ‘Amount Category’ as ‘Sch-Overdue’ and disables this field.

Select the applicable category using the drop-down list. The system defaults to Normal.

Specifying the penalty start day basis

Oracle Lending calculates the penalty in case the loan payment is not made on the principal schedule date. However, if the payment date falls on a holiday, the penalty can be calculated depending on the start date that you specify in this screen:

If you have specified that penalty start date basis as the Due Date, the penalty is calculated from the due date of payment even if it falls on a holiday.

If you have specified that the penalty start basis be Next Working Day, the penalty is calculated from the working day following the holiday. Thus the system waives the penalty for the holiday (s).

Example

Assume a loan principal payment schedule falls on 11th October 2003, which is maintained as a holiday in Oracle Lending.

In addition, there is a deficit of funds in the customer’s account for making the payment.

If you have selected the due date option, Oracle Lending calculates the penalty from 11th October 2003.

If you have selected the next working day option, the system calculates the penalty from 13th October 2003 and waives the penalty for 11th and 12th October.

You can choose to accrue the interests due on a contract. To accrue the interest payable on a contract, choose the ‘Accrual Required’ option.

The accrual details that you define for an interest class defaults to all products with which you associate the class. When maintaining interest accrual details for a product, you can change these default details. Contracts maintained under a product acquires the accrual details defined for the product. However, you can define unique accrual details for a contract.

Specifying Rate Details

Rate Type

The interests paid on contracts can be at a Fixed Rate, or on the basis of a Floating Rate. If you indicate that interests should be calculated on the basis of a Floating Rate, you must specify the ‘Periodic’ Floating Rate Type.

For all contracts maintained under products, associated with a class, the interest will be by default calculated using the specified Rate type.

If you select the ‘Basis Amount Tag’ as ‘SCH_AMT_OS’, then system defaults the ‘Rate Type’ as ‘Special’ and disables this field.

Special Rate Type

Select the special rate type from the adjoining drop-down list. This list displays the following values:

- Fixed Rate

- Flat Amount

This field is enabled only if the ‘Special Penalty Component’ box is checked. By default, system displays the value of ‘Special Rate Type’ as ‘Fixed Rate’.

Indicating the Fixed Rate Type

If the rate type is ‘Fixed’, you have to indicate whether the rate would be entered by the user or needs to be picked up from the rate maintenance table. The following options are available:

- User Input (U) – This option may be used if you want the user to specify the rate of interest applicable on the contract

- Standard (S) – If you opt for this option, the system pick-ups the rate from the ‘Standard Rate Maintenance’ screen. This rate is combination of the Standard Rate, Amount-Slab-Wise Spread and Tenor-wise Spread. However, you can change this rate at the contract level

- For contracts involving fixed rate interest components, your bank may require choosing the applicable rate from historical floating rates for a floating rate code that has been maintained for a treasury source. For such requirements, select the TREASURY option in the Fixed Rate Type field. This option is applicable only for interest classes that you define for the Loans module.

When you enter a fixed rate loan contract or Money Market deal which involves an interest component class for which the TREASURY Fixed Rate Type option has been indicated, the historic floating rates maintained for the default floating rate treasury designated for your branch, are available for choosing.

Specifying Borrow Lend Indicator

You can select the following option from the drop-down list. By default, ‘Mid’ is selected.

- Borrow

- Lend

- Mid

For floating rate interest, you should also indicate if the interest rate for a given rate code to be applied, from the Floating Rates table, is the ‘Borrow’, ‘Lend’ or ‘Mid’ rate.

Specifying the method for Interest Computation

You need to specify the method to be used for computation of interest. The available options are:

- Simple - indicates that the interest would be computed using the Simple Interest formula

- Compound - indicates that the interest would be compounded

Indicating whether compounding of interest on holidays is required

You can opt to compound interest on holidays. Select the ‘Compounding on Holidays’ option to indicate the same.

An example to show compounded interest calculation is given under the section titled ‘Defining interest details’.

Indicating Exponential Interest Method

If main interest component is of exponential method for the loan product, the system validates that the day’s basis mentioned for main interest and penalty interest components are same during contract save/modification.

Indicating Allow Reporting Only

By default, this check box is not selected. If 'Allow Reporting Only' is selected then the component does not have any schedules and it is liquidated when the main interest is liquidated. For COSIF the accrual is always be on a Actual/360 basis, for RAP the amount is

deducted upfront and reverted during the accruals. COSIF and main Component always have the same amount due on the schedule dates which are achieved by adjusting the effective rate for COSIF using the below logic

Rate_act360 =(((((〖Rate〗_bu252/100)+1)^( #budays /252))^(360/#days))-1)*100

Special Penalty Comp

System automatically checks this box if you select the ‘Basis Amount Tag’ as ’SCH_AMT_OS’ and you cannot modify it.

Specifying the Default Fixed Rate Code

If you opt for ‘Standard’ rate type, you have to select rate code based on which rate pick-up would be done.

All the rate codes maintained through the ‘Standard rate code maintenance’ screen will be available for selection in the option-list provided. The Standard rates maintained (in the Standard Rate Maintenance screen) for the selected rate code would be applicable on all products associated with the Interest class being maintained.

Specifying the Prepayment Penalty Rate Code

Likewise, select the rate code based on which the system will pick-up the prepayment penalty rate for all contracts under the product. Whenever a prepayment is processed, the prepayment penalty rate maintained for the selected rate code is applied on all the contracts associated with this interest class.

Choosing Rate Basis

The following options are available for rate basis.

- Per Month – This option is used for fixed per month rate.

- Per Annum/Not Applicable – This option is used for annual rate input. The value input is considered as resolved rate.

- Quote Basis – This option is used for float rate input for all quote basis.

Choosing the Default Floating Rate Code

Interest payable on contracts would be calculated at specific rates. When building an interest component, you have to specify the rate at which the interest should be computed. When associating a rate code (that you have maintained in the Rate Codes Maintenance screen) with the interest component that you are building, the rates corresponding to the code is used to compute interest.

The details defined for an interest class defaults to all products with which the class is associated. When maintaining interest details for a product, you can change this default information. Contracts maintained under a product acquires the interest details defined for the contract product. However, you can define unique interest details specific to a contract.

When maintaining a contract, you can choose to waive the rate code altogether or amend the properties of the code to suit the security.

If you allow amendment of a rate code, you can specify if you would like to allow rate code amendment after the association event.

You can also allow the amendment of the rate value (corresponding to a rate code).

Each rate code is associated with a tenor. For instance you have a Rate Code ‘LIBOR’. You can link any number of tenor codes to the same rate code.

Tenor Code |

Description |

1W |

One week rate |

2W |

Two week rate |

2M |

Two months rate |

6M |

Six months rate |

1Y |

One year rate |

When building an interest component, you can specify a Tenor Code that you would like to associate, with the Floating Interest Rate Code. Interests for contracts (maintained under a product with which you associate the class) is calculated using the rate corresponding to the Rate Code and the Tenor Code.

Indicating whether interest should be applied on premature withdrawal

You can opt to waive Interest on premature withdrawal of the loan. Select the ‘No interest on premature withdrawal’ option to indicate that interest needs to be waived if premature withdrawal (partial of full) is done for the loan.

Reapplying interest rate on prepayment

If the ‘Fixed’ rate type is ‘Standard’, you can opt to reapply interest when a prepayment is made.

You can reapply interest on one of the following:

- On Prepaid Amount – Select this option to indicate that interest on the prepaid amount would be recalculated during prepayment based on the rate applicable for the current tenor of the loan.

- On Outstanding Balance – This option indicates that interest is recalculated on the outstanding balance during prepayment based on the rate applicable for the current tenor of the loan

Enabling the Consider as Discount option

While defining an interest class for either the loans or the bills module, you can indicate whether the interest component is to be considered for discount accrual on a constant yield basis and whether accrual of interest is required.

If you select the ‘Consider as Discount’ option the interest received against the component is used in the computation of the constant yield and subsequently amortized over the tenor of the associated contract. By checking this option, you can also indicate whether the component should be included in the Internal Rate of Return computation.

If you select the ‘Accrual Required’ option, the interest is accrued depending on the accrual preferences defined for the product.

If neither option is selected, the interest is not accrued, but is recognized as income on interest liquidation.

The ‘Consider as Discount’ option is not available if the amount category is Penalty.

Note

- For bearing contracts, if the option ‘Consider as Discount’ is checked then the option ‘Accrual Required’ also has to be checked. If the option ‘Accrual Required’ is not checked, the option ‘Consider as Discount’ is disabled.

- For Discounted contracts, you can select either one of the options or both together. If the options ‘Accrual Required’ and ‘Consider as Discount’ are selected then discounted interest is considered for IRR calculation. If the option ‘Accrual Required’ is not selected and ‘Consider as Discount’ is selected, then discounted interest is considered a part of the total discount to be accrued.

- The ‘Consider as Discount’ option is not available if the amount category is Penalty.

Reporting Component Type

By default, the value is blank. You can select RAP, COSIF and blank from the drop-down list. This is applicable only when ‘Allow Reporting Only’ is selected.

Payment Delay Days

You can define the payment delay days in this screen and the same is defaulted to product and contract screens.

Payment delay days is used to capture the number of days between 'Schedule Due Date' and 'Pay By Date'.

For example, for a contract payment scheduled for Principal and Main Interest component is 05 Feb 2017, and the Payment Delay Days is 5, then you can 5 days buffer to do the repayment, that is till 10 Feb 2017. In case of non-payment till ‘Pay By Date’, that is, till 10 Feb 2017, penalty is calculated from 'Pay By Date' only not from 'Schedule Due Date'.

Holiday treatment is applicable for ‘Pay By Date’. If ‘Pay By Date’ falls on holiday and holiday treatment is enabled for the contract then ‘Pay By Date’ gets adjusted according to holiday treatment.

Example, 10 Feb 2017 undergoes same holiday treatment as the due date (as defined in product)

Alternative Risk-Free Rate

If you select this check box then only you can select options available in the 'Alternative Risk-Free Rates Preferences' screen. Select this check box to define floating rate as ‘Alternative Risk Free Rate’.

Note

Look back and Look out methods can be selected in combination. None of the other methods are selected in combination.

Look Back

Apply x days prior rate, where the x number of look back days is configurable. Payment on due date continues with no change.

On the booking date of a contract, X days prior rate considered & applied. The no of prior days is captured on Look Back Days field. And, with the past day's rate available till X day, the subsequent dates calculation is done.

For example, Lookback Days = 5 days. On 12 May 20, a contract is booked with current value date, for 1 year term, with monthly schedules. Rate is available till 8 May.

Rate pickup date is arrived as Tuesday 12 May 20 - 5 working days = Tuesday 5 May 20. So 5 May 20 rate is applied for 12 May. And the already available 6 May to 8 May rates are applied as below.

- Rate fixed till Rate picked up date

- Tuesday, May 12, 2020 Tuesday, May 5, 2020

- Wednesday, May 13, 2020 Wednesday, May 6, 2020

- Thursday, May 14, 2020 Thursday, May 7, 2020

- Friday, May 15, 2020 Friday, May 8, 2020

And, once the 11 May rate is received, on current day's EOD, the same is be applied to Monday 18 May. Thus 4 days ahead of due date the calculation for the schedule is completed. Liquidation continues to happen on Due Date BOD (if Payment Delay Days = 0)

Payment Delay

Apply current day’s rate. As the current day’s rate is published only on the next day, current day’s interest computation happens on the next day. Thus, interest for the last day of the schedule is arrived on due date. Hence payment date can be configured x days after the due date. The x payment delay days is configurable. Auto liquidation of the payment happens on the pay by date, instead of the due date. Rollovers go by due date.

Always uses current day's rate. On booking current day rate is considered as 0. Calculation & accrual does not happen on book date EOD. On 2nd day EOD, interest calculation for previous day happens. Accordingly calculation for last day of the schedule happens on due date EOD. So LIQD does not happen on due date, instead happens on Pay By Date.

For ex ample, Payment Delay Days = 3. On 12 May 20, current dated contract is booked, for 1 year term, with monthly schedules. On Book date EOD, calculation & accrual does not happen. On 13 May EOD, interest calculation for 12 May is done. On the due date 12 Jun BOD, liquidation is skipped, as calculation for 11 Jun is pending. On 12 Jun EOD, calculation for 11 Jun is done, and schedule liquidation is triggered on the Pay By Date.

Lockout

Apply current day’s rate. However, x days ahead of due / maturity the current day’s rate is frozen and the same is applied till the schedule end date. Thus notice is generated with accurate expected interest amounts. The x lock out days is configurable.

On booking current day rate is considered as 0, as not available. Calculation and accrual does not happen on book date EOD. On 2nd day EOD, interest calculation for previous day happens. However, X days prior to the due date, the rate is frozen and applied till the due date-1. Hence on Due Date BOD, schedule liquidation is triggered.

For example, Lockout Days = 5. Current dated contract booked on 12 May 20, with 1 year term and monthly schedules. On book date no accrual is posted. On 13 May EOD, calculation for 12 May is done. Schedule due is on 12 Jun 20. Lock out freeze date is arrived as Due date, Friday 12 Jun - 5 currency business days = Friday 5 Jun 20. On 5 Jun EOD, the 4 Jun rate is applied for 4 Jun as usual. In addition, the same applied till 11 Jun. Thus, billing notice could be generated on 5 Jun EOD and liquidation is triggered on the due date 12 Jun BOD.

Interest Rollover

This SOFR method is for bearing loans. Booking and cash flow projection goes with latest available rate. On payment due date EOD re-calculation happens with the actual rates. The difference in interest amount (between projected and actual) is adjusted on the interest on the next schedule.

For example, On 12 May 20, current dated contract is booked, for 1year term, with monthly schedules. Calculation and accrual happens with latest available rate (during booking). On payment 12 Jun 20 due date BOD, Instalment get debited and during EOD, system applies the actual rate from booking to end of schedule and the recalculated amount difference (between projected and actual) is adjusted on the interest on the next schedule 13 Jul 20.

Principal adjustment

This SOFR method is for amortized loans. Instalment is arrived with latest available rate. On payment due date EOD re-calculation happens with the actual rates. The difference in interest amount (between projected and actual) is adjusted on the interest on the next schedule, thus the principal of the next schedule is also changes to retain the instalment same.

For example, On 12 May 20, current dated contract is booked, for 1year term, with monthly schedules. Calculation and accrual happens with latest available rate (during booking). On payment 12 Jun 20 due date BOD, Instalment get debited and during EOD, system applies the actual rate from booking to end of schedule and the recalculated amount difference (between projected and actual) is adjusted on the interest on the next schedule 13 Jul 20, thus the principal of the next schedule is also changes to retain the instalment.

Last reset

This SOFR method is for discounted loans and true discounted loans. The SOFR average rate same as the payment periodicity of the loan will be linked operationally. Booking and cash flow projection goes with latest available rate of the linked rate code. On payment due date BOD rate revision is triggered to fetch the latest average rate. Re-calculation happens with this rate and the same is liquidated.

For example, For a 1 year contract with quarterly liquidation cycle, the 90 days average SOFR rate code will be mapped. And, for a loan with monthly payment schedule, the 30 days average SOFR rate code is linked. On booking, latest available average SOFR rate is picked up & applied to the loan. Cash flow projection till maturity goes with this rate. Advance interest collection for the first schedule happens with the same rate, on booking. Every day accrual happens with the same rate. Rate revision is controlled on this method, and triggered only on the payment due dates. On due date BOD, again the latest available average SOFR rate is picked up applied for the subsequent schedules. Rate fixing days is applicable to this method.

For example, For a last reset loan booked on Tue, 12 May 20 with rate fixing days 2, the SOFR average rate of Fri 08 Aug 20 is applied.

Last recent

This SOFR method is for discounted loans and true discounted loans. The recent SOFR average rate, lesser than the payment periodicity of the loan will be linked operationally. Booking and cash flow projection goes with latest available rate of the linked rate code. On payment due date BOD rate revision is triggered to fetch the latest average rate. Re-calculation happens with this rate and the same is liquidated.

For example, For a 1 year contract with quarterly liquidation cycle, the 30 days average SOFR rate code will be mapped. On booking, latest available average SOFR rate is picked up & applied to the loan. Cash flow projection till maturity goes with this rate. Advance interest collection for the first schedule happens with the same rate, on booking. Every day accrual happens with the same rate. Rate revision is controlled on this method, and triggered only on the payment due dates. On due date BOD, again the latest available average SOFR rate is picked up applied for the subsequent schedules. Rate fixing days is applicable to this method. Ex : For a Last Recent loan booked on Tue, 12 May 20 with rate fixing days 2, the SOFR average rate of Fri 08 Aug 20 is applied.

Plain

Apply current day’s rate. Due amount for the schedule is arrived on the due date EOD as previous day’s rate is received today. The payment follows on the same EOD, i.e. on due date. (Payment on due date BOD is skipped on this method).

This behaves similar to Payment Delay method, except the difference that, liquidation happens on Due dt EOD and Payment Delay Days is not applicable.

For ex ample, Payment Delay Days = 0. On 12 May 20, current dated contract is booked, for 1 year term, with monthly schedules. On Book date EOD, calculation & accrual does not happen. On 13 May EOD, interest calculation for 12 May is done. On the due date 12 Jun BOD, liquidation is skipped, as calculation for 11 Jun is pending. On 12 Jun EOD, calculation for 11 Jun is done, followed by schedule liquidation.

Note

- For Penalty component, the allowed RFR methods are either ‘Look Back’ or ‘Plain’.

Rate Compounding

Rate Compounding is another method of compounding the interest in SOFR calculation along with amount compounding. Rate Compounding approaches accurately compound interest when principal is unchanged within an interest period or, if principal is paid down, when any accompanying interest is paid down at the same time.

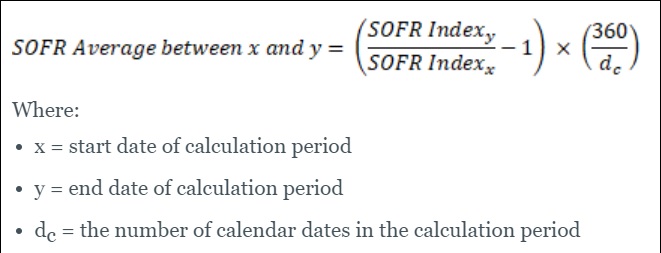

Index Value

To apply index related rate code along with amount compounding, index value method to be selected. The RFR index measures the cumulative impact of compounding the RFR on a unit of investment over time, with the initial value set to 1.00000000 on a particular date. The Index is compounded by the value of each RFR thereafter. The following formula can be used to calculate compounded averages of the SOFR over custom time periods between any two dates within the SOFR publication calendar.

Observation Shift

In RFR Look back method, when a back dated rate is applied for the current date, the weightage of the rate, based on its applicable days, is considered while arriving the rate factor, and applied to the current rate application date.

Lookback Days-

This option is applicable only for Look Back method.

Lockout Days

This option is applicable only for Lockout method.

Base Rate/Spread Margin/ Spread Adj Computation Method

You can select 'Simple' or 'Compound'. For compounding, interest calculation on week days go with compounded P, while for week ends its on simple P.

Rate Compounding Method

You can either select 'NCCR' or 'CCR' methods. The rate compounding happens in these two methods for RFR rate types (Normal and Index value rate types).

CCR - Cumulative Compounded Rate calculates the compounded rate at the end of the interest period and it is applied to the whole period. It allows calculation of interest for the whole period using a single compounded rate.

NCCR - Non Cumulative Compounded Rate is derived from Cumulative Compounded Rate i.e., The Cumulative Compounded Rate is first un-annualized. And then the cumulating is removed by subtracting previous day rate with current day & the same is annualized.. This generates a daily compounded rate which allows the calculation of a daily interest amount. For OL module, this value gets defaulted to 'Bilateral Loans - Product Definition' (OLDPRMNT) from 'Interest Class Maintenance' screen. If required, you can define rate compounding method at component level in these product screens. Similarly, rate compounding method is defaulted to 'Loan and Commitment -Contract Input' (OLDTRONL) screen based on the selection at the product level. If required, you can define rate compounding method at component level in these contract screens.

For LB module, this value gets defaulted to Loan Syndication -Borrower Product Definition' (LBDPRMNT) screen from 'Interest Class Maintenance' screen and then it is defaulted from product to tranche (LBDTRONL). If required, you can redefine the rate compounding method at tranche level. For drawdown contract (LBDDDONL), rate compounding method is defaulted from tranche (LBDTRONL). If tranche level rate compounding method is not defined then, it is defaulted from product screen. If required, you can redefine the rate compounding method at drawdown contract level as well.

RFR Rounding Unit

This option is applicable only for Rate compounding method. This contains the Risk Free Rate rounding unit as agreed with the borrower. The CCR is rounded with this parameter.

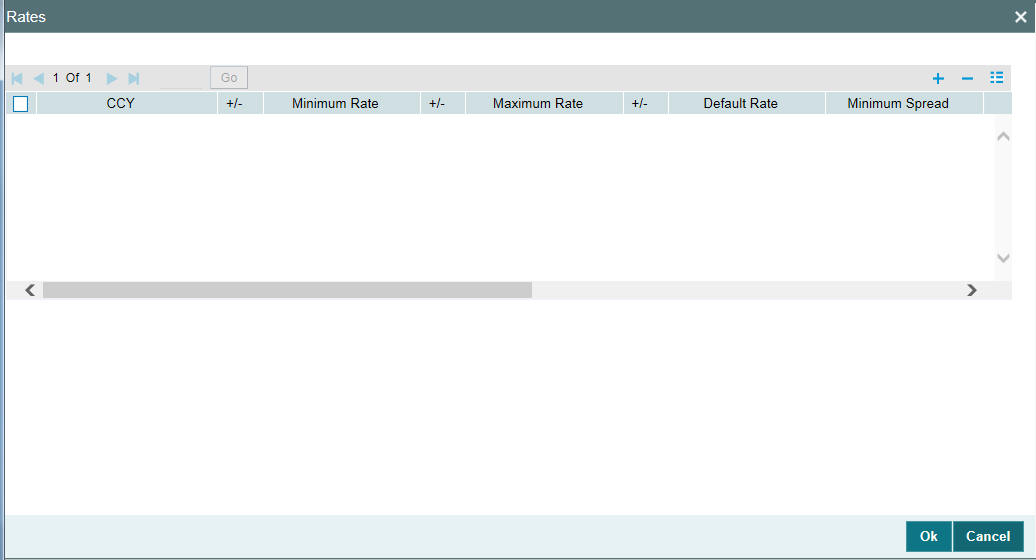

3.2 Specifying Currency-wise Limits for Interest Rate Application

When you define an interest class, you can specify the limits applicable for the interest component, and the rules according to which interest amounts in respect of the interest component must be rounded. To define the rules, click the ‘Rates’ button in the ‘Interest Class Maintenance’ screen. The ‘Rates’ screen is displayed.

In this screen, the following limits and rounding rules can be defined for each currency and for each tenor:

- For fixed rate components, the default rate to be applied in respect of the interest component

- The allowable limits for the interest rates in respect of the component. You can define the minimum and maximum applicable interest rates. If the interest rate falls below the minimum, the minimum rate is applicable; similarly, if the interest rate exceeds the maximum, the maximum rate is applicable

- For floating rate components, the allowable limits for the spread that can be applied on the floating rate. If the spread falls below the minimum, the minimum spread is applicable; similarly, if the spread exceeds the maximum, the maximum spread is applicable

- The basis on which interest is calculated for each currency, for which the limits are applicable

- How the interest amounts in respect of the interest component in the specified currency are to be rounded – truncated, rounded up, rounded down or rounded near

- If truncation is opted for, the number of digits after the decimal place, to which interest amounts in respect of the interest component in the specified currency must be truncated. The number of digits specified for truncation cannot exceed the allowed decimal places for the specified currency. If not specified, the number of decimals indicated in the Currency Definition for the specified currency is picked up by the System

- For the Round Up, Round Down and Round Near options, the rounding unit which is the lowest possible measure in which the interest amounts, in respect of the interest component in the specified currency, can be considered. This value cannot be less than the rounding unit for the specified currency in the Currency Definition. If not specified, the rounding unit indicated in the Currency Definition for the specified currency is picked up by the System

Note

- When generic interest limits are being defined for all currencies in the Currency-wise Limits screen (that is, the ALL option has been selected in the Currency field), the fields relating to rounding rules are not available for definition

- The currency rounding rules can be defined only for classes that would be maintained for Loans and Money Market modules

Specifying the interest period basis

You can indicate how the system must consider the tenor basis upon which interest is computed over a schedule or interest period, in respect of the interest component.

You can specify the interest period basis for each currency in the Currency-wise Limits screen, which you can invoke by clicking the Rates button in the Interest tab in the ‘Interest Class Maintenance’ screen.

You can choose any of the following options:

Including the From Date

For all schedules, the period considered for interest calculation would include the start date and exclude the end date. Therefore, the value date of the loan is considered for interest calculation and the maturity date is excluded.

Including the To Date

For all schedules, the period considered for interest calculation would exclude the start date and include the end date. Therefore, the value date of the loan is excluded, but the maturity date is included for interest calculation.

Including both From and To Dates

The period considered for interest calculation would include both the value date and the maturity date. This would mean:

- For the first schedule, it would include the Value Date. Interest would be calculated for the Value Date

- For the last schedule, it would include the Maturity Date. Interest would be calculated for the Maturity Date

Excluding both From and To Dates

The period considered for interest calculation would exclude both the value date and the maturity date. This would mean:

- For the first schedule, it would exclude the Value Date. No interest would be calculated for the Value Date

- For the last schedule, it would exclude the end date. No interest would be calculated for the Maturity Date

Note

This feature is only available for classes that would be maintained for Loans module.

Maintaining positive or negative values for interest limits and the default rate

When you maintain currency-wise interest rate limits for the interest class, you can indicate the applicable sign for the interest limits values as well as for the default rate value. If required, you can assign the negative sign, indicating a negative range for the limits, or a negative default rate.

In the case of Default Rate, the assigned sign is defaulted along with the rate specified, for contracts that use a product associated with this class.

Click on the Rates button in the Interest tab in the ‘Interest Class Maintenance’ screen, to invoke the Currency-wise Limits screen.

Note

This feature is only available for classes that would be maintained for the Money Market module.

Specifying interest basis

A new interest basis methods are introduced to support interest and penalty calculations based on working days and 365.25 as denominator for leap and non-leap year.

Different values for the numerator basis are as explained below:

- Actual - Actual number of days in a month is taken.

- 30 (Euro) - 30 days is considered for all months including February irrespective of leap or non-leap year.

- 30 (US) - 30 days is considered for interest computation for all months except February where the actual number of days is considered.

- Working Days - To calculate the working days, branch holiday maintenance of the branch where loan is booked is considered. During interest calculation the days are calculated based on the working days.

Different values for the denominator of the interest basis are as explained below.

- 252- Number of days in a year is taken as 252 which is the number of working days.

- 360 - Number of days in a year is taken as 360 irrespective of actual number of calendar days.

- 365 - Number of days in a year is taken as 365 for leap as well as non-leap year.

- Actual: Actual number of days in a year is taken for interest calculation which is 366 for non-leap year.

- 365.25 - Number of days in a year is taken as 365.25 for leap as well as non-leap year.

Note

- 252 interest basis is applicable for all schedule type like, bearing, Amortized, Discounted, and so on. There is no restriction in component level for the application of 252 basis.

- The system does not consider the currency holiday preference for working day calculation. It considers only the branch local holiday maintenance.

- No changes are done to interest basis available in currency definition screen.

- There is no any change in grace days calculation for penalty interest even if interest basis is “Working Days”. It is based on calendar days.

- Interest accrual happens only for working days. The interest basis gets the number of days from the previous accrual date to the current accrual date. If there are no holidays in a month, even though denominator is 252, interest accrual happens till end of the month.

- In case an ad-hoc holiday is declared, then the system does not recalculate the interest as part of ad-hoc holiday processing. Accrual adjustment for the unaccrued portion happens on the schedule end date.

If the 'Interest Basis' is selected as '30SPL/360' then number of actual working days in a month is taken as 30 and number of days in a year is taken as 360 for interest calculation. The interest calculation based on the computation days.

Specifying Interest Rate Rounding Components

The ‘Rate Rounding Rule, ‘Rate Rounding Unit’, and ‘Rate Rounding Position’ values get defaulted from ‘Interest Limits Detail’ screen. If required, you can change these values

3.3 Processing CPR (Conditional Prepayment Rate) Loans

CPR (Conditional Prepayment Rate) Loans are referred to the loans which have the interest on Principal Outstanding fixed till maturity and floating rate thereafter.

Oracle Lending allows you to create a secondary interest component which can be applicable only after the maturity date of a loan on the total principal outstanding. While defining the interest class definition for the secondary interest component, you should specify the amount tag as ‘Principal’ and the amount category as ‘Overdue OS’ and the rate type as ‘Floating’ which gets defaulted to the ‘Interest Class Maintenance’ screen also.

Note

Interest computation on Outstanding Principal balance is applicable for Normal-Bearing type of loans.

3.4 Calculating Loan Interest Accrual on Principal Outstanding

When you select amount category as ‘Outstanding’ for calculating the interest the interest is calculated on the balance of the total principal outstanding amount. ’Loan and Commitment- Contract Input’ screen accepts the schedules for Interest which is defined for this amount category.

The accrual logic remains the same and to arrive at the daily average amount the total interest is divided by the number of days. However, the computation of interest schedules change based on the above setup.

Example;

A contract is booked with the following details

Principal Amount |

12000000 |

Interest Rate |

10% |

Value Date |

28-Sep-05 |

Maturity Date |

28-May-06 |

The amount category is maintained as “Expected” and the schedules of Principal and Interest are defined as monthly. The schedules get defined in the following manner.

Principal |

Interest Rate |

Start Date |

End Date |

No of Days |

Principal Schedule |

Interest Amount |

Daily Avg Amount |

12000000 |

10% |

28-Sep-05 |

28-Oct-05 |

30 |

2000000 |

100000 |

3333.33333 |

10000000 |

10% |

28-Oct-05 |

28-Nov-05 |

31 |

2000000 |

86111.1111 |

2777.77778 |

8000000 |

10% |

28-Nov-05 |

28-Dec-05 |

30 |

2000000 |

66666.6667 |

2222.22222 |

6000000 |

10% |

28-Dec-05 |

28-Jan-06 |

31 |

2000000 |

51666.6667 |

1666.66667 |

4000000 |

10% |

28-Jan-06 |

28-Feb-06 |

31 |

2000000 |

34444.4444 |

1111.11111 |

2000000 |

10% |

28-Feb-06 |

28-May-06 |

89 |

2000000 |

49444.4444 |

555.555556 |

However the schedules will get defined in the following manner for the contract with same details as above, if the amount category is maintained as “Outstanding”.

Principal O/s |

Interest Rate |

Start Date |

End Date |

No of Days |

Principal Schedule |

Interest Amount |

Daily Avg Amount |

12000000 |

10% |

28-Sep-05 |

28-Oct-05 |

30 |

2000000 |

100000 |

3333.33333 |

12000000 |

10% |

28-Oct-05 |

28-Nov-05 |

31 |

2000000 |

103333.333 |

3333.33333 |

12000000 |

10% |

28-Nov-05 |

28-Dec-05 |

30 |

2000000 |

100000 |

3333.33333 |

12000000 |

10% |

28-Dec-05 |

28-Jan-06 |

31 |

2000000 |

103333.333 |

3333.33333 |

12000000 |

10% |

28-Jan-06 |

28-Feb-06 |

31 |

2000000 |

103333.333 |

3333.33333 |

12000000 |

10% |

28-Feb-06 |

28-May-06 |

89 |

2000000 |

296666.667 |

3333.33333 |

Here even though the schedules are defined for monthly payment schedules of Principal, the schedules are computed on the Loan Principal Outstanding since the Principal amount is not ‘expected’ to be paid at the time of Loan Initiation.

Now assuming that the payment of principal which was due on 28-Oct-2005 was paid along with the interest due on the scheduled due date, then the schedules are redefined as under.

Principal O/s |

Interest Rate |

Start Date |

End Date |

No of Days |

Principal Schedule |

Interest Amount |

Daily Avg Amount |

12000000 |

10% |

28-Sep-05 |

28-Oct-05 |

30 |

2000000 |

100000 |

3333.33333 |

10000000 |

10% |

28-Oct-05 |

28-Nov-05 |

31 |

2000000 |

86111.1111 |

2777.77778 |

10000000 |

10% |

28-Nov-05 |

28-Dec-05 |

30 |

2000000 |

83333.3333 |

2777.77778 |

10000000 |

10% |

28-Dec-05 |

28-Jan-06 |

31 |

2000000 |

86111.1111 |

2777.77778 |

10000000 |

10% |

28-Jan-06 |

28-Feb-06 |

31 |

2000000 |

86111.1111 |

2777.77778 |

10000000 |

10% |

28-Feb-06 |

28-May-06 |

89 |

2000000 |

247222.222 |

2777.77778 |

The accrual amount on the EOD of 28-Oct-2005 with the next working day as 29-Oct-2005 is 2777.78

Note

Even a prepayment of Principal changes the accrual amount.

Example;

If a contract has been booked with the following details,

Principal Amount |

12000000 |

Interest Rate |

10% |

Value Date |

28-Sep-05 |

Maturity Date |

28-May-06 |

Assuming that all the repayment schedules except the last two schedules have been paid, the schedules are the following:

Principal O/s |

Interest Rate |

Start Date |

End Date |

No of Days |

Principal Schedule |

Interest Amount |

Daily Avg Amount |

12000000 |

10% |

28-Sep-05 |

28-Oct-05 |

30 |

2000000 |

100000 |

3333.33333 |

10000000 |

10% |

28-Oct-05 |

28-Nov-05 |

31 |

2000000 |

86111.1111 |

2777.77778 |

8000000 |

10% |

28-Nov-05 |

28-Dec-05 |

30 |

2000000 |

66666.6667 |

2222.22222 |

6000000 |

10% |

28-Dec-05 |

28-Jan-06 |

31 |

2000000 |

51666.6667 |

1666.66667 |

4000000 |

10% |

28-Jan-06 |

28-Feb-06 |

31 |

2000000 |

34444.4444 |

1111.11111 |

4000000 |

10% |

28-Feb-06 |

28-May-06 |

89 |

2000000 |

98888.8889 |

1111.11111 |

The highlighted schedules are unpaid. On the EOD of 28-May-2006, the Main Interest Component Accrual stops and the Floating Interest component starts computing the interest based on the maintenance, with the basis amount as 4000000.

3.5 Calculating Interest for Interest Basis '30SPL/360’

- In case of new drawdown booking/rollover/value dated amendment, the principal and interest payment schedules should be defined either as ‘Monthly’, ‘Quarterly’ or ‘Bullet’.

- No other frequency is allowed for the new interest basis ‘30SPL/360’.

- In case of consolidated rollover or consolidated + split rollover, all the parent contracts being rolled over should be associated with the same interest basis method ‘30SPL/360’.

- In case of split rollover, the parent contract being rolled over should be associated with the same interest basis method ‘30SPL/360’. However, a parent contract with the new interest basis ‘30SPL/360’ can be split rolled to a child contract with any other interest basis.

Note

The computation of interest based on the new interest basis is applicable only for the contracts where the new interest basis ‘30SPL/360’ is selected.

There is no impact in the existing contracts even if the new interest basis is added to the corresponding products. Only the new contracts created will have the interest computation based on the new interest basis.

- In LS module, amendment of interest rate basis from ‘30SPL/360’ to other interest basis or from other interest rate basis to ‘30SPL/360’ for main/PIK interest component will be allowed only as part of contract amendment (CAMD). You are not allowed to amend the interest basis as part of value dated amendments (VAMI).However, the system validates that there should not be any of the below financial events processed in the contract when user changes the interest basis as part of CAMD. If the validations are failed, the system displays appropriate error messages.

- Value dated amendment (future/backdated) for principal amount change (VAMI)

- Value dated amendment (future/backdated) for maturity date change (VAMI)

- Liquidation/Payment (LIQD) - future/backdated

- Participant Ratio Amendment (PRAM)

- Future dated rollover/split rollover/consolidated rollover

- Future dated split/merge reprice

Note

Contract amendment can be processed in Oracle Banking Corporate Lending only from the value date of the contract. Hence the change in interest basis method by means of CAMD is effective from the value date itself and the computation is revised from the value date.

- In OL module, amendment of interest rate basis from ‘30SPL/360’ to other interest basis or from other interest rate basis to ‘30SPL/360’ for main/PIK interest component is allowed only as part of value dated amendment (VAMI). However, the system validates that there should not be any of the below financial events processed in the contract when you change the interest basis as part of VAMI. If the validations are failed, the system display appropriate error messages.

- Value dated amendment (future/backdated) for principal amount change (VAMI)

- Value dated amendment (future/backdated) for maturity date change (VAMI)

- Liquidation/Payment (LIQD) - future/backdated

- Future dated split/merge reprice

Note

When the user amends the interest basis through value dated amendment screen, system validates if the amendment date is equal to the value date of the contract. If the validation is failed, appropriate error messages are displayed.

- Split and Cosol reprice are not allowed if interest basis is ‘30SPL/360’ for OL module

- Split Reprice functionality is allowed in LS module for all LS drawdown contracts where the new interest basis ‘30SPL/360’ is selected. Merge reprice is not allowed in LS module. You are allowed to perform split reprice for the LS drawdown contracts with the same amount as the parent contract or reprice with increased / decreased amount. However, the split reprice can be done only with the value date as the maturity date of the LS drawdown contract.

- When you perform, split reprice with decrease for LS drawdown contracts where the new interest basis ‘30SPL/360’ is selected, the ‘Liquidate Principal’ check box need not be selected mandatorily. If the ‘Liquidate Principal’ check box is not selected and reprice with decrease is done, the parent contract is left active. However, any further payments done on the contract is allowed only for the maturity date of the contract. Appropriate error message is displayed if any further payments are not done on the maturity date of the contract.

- The interest basis for the child drawdown contracts are defaulted from the ‘Interest Basis’ field selected for each of the child contracts in the LS Split Reprice screen. However, you are allowed to change the interest basis for the child contract through CAMD as per the existing functionality.

- You are not allowed to select the interest basis as ‘30SPL/360’ for the child contracts in the LS split reprice screen if the parent contract being repriced is not associated with the new interest basis ‘30SPL/360’. However, a parent contract with the new interest basis ‘30SPL/360’ can be repriced to a child contract with any interest basis.

- In the LS split reprice screen, you are not allowed to select the ‘Liqd Int On Prepayment’ check box for the contracts where the new interest basis ‘30SPL/360’ is selected.

- You are not allowed to select the ‘Liqd Interest on Prepayment’ check box for a drawdown contract when the new interest basis ‘30SPL/360’ is selected either for the main interest or PIK interest component. Similarly, you are not allowed to select the new interest basis ‘30SPL/360’ for the main interest or PIK interest component when the ‘Liqd Interest on Prepayment’ check box is checked.

Note

You are allowed to change the interest basis from ‘30SPL/360’ to another interest basis as part of CAMD from the value date of the contract and simultaneously select the ‘Liqd Interest on Prepayment’ check box.

- You are not allowed to select the ‘Partial Interest Payment Allowed’ check box in the LS drawdown contract online screen when the new interest basis ‘30SPL/360’ is selected. Similarly, you are not allowed to select the new interest basis ‘30SPL/360’ when the ‘Partial Interest Payment Allowed’ check box is selected.

- You are not allowed to prepay principal / interest for the contracts where the new interest basis ‘30SPL/360’ is checked.

- You are not allowed to do full / partial payment of principal for contracts with new interest basis ‘30SPL/360’ if the‘Liqd of Int on Prepaid Principal’ check box is selected in the manual payment screen in both the LS module.

- You are allowed to do partial / full principal payment in the contracts where new interest basis ‘30SPL/360’ is selected, but only on the maturity date / schedule due date of the contracts. Partial principal prepayments are not allowed and appropriate error messages are displayed. You are allowed to pay the interest amount only in full when full / partial principal payment is done on the maturity / schedule due date of the contracts.

- In the LS and OL manual payment screens, if you enter the limit date as the maturity date of the contract, the total principal + interest payment which is due till maturity date (including the overdue schedules) is populated in the field ‘Amount Paid’ as per the existing functionality. However, you are allowed to do full/partial principal payment only to the extent of the total principal due till the value date entered in the manual payment screen. If you enter a greater amount, appropriate error messages are displayed.

- If you enter the limit date as the schedule due date of the contract, the total principal payment which is due till the schedule due date entered (including the overdue schedules) is populated in the field ‘Amount Paid’ as per the existing functionality. However, you are allowed to do full/partial principal payment only to the extent of the total principal due till the value date entered in the manual payment screen. If you enters a greater amount, appropriate error messages are displayed.

The computed interest is applied while processing the below events for OL/LS module.

Module |

Event Code |

Description |

Remarks |

OL |

DSBR |

Disbursement |

Interest is computed with the new interest basis and the schedule details are populated accordingly |

OL |

ACCR |

Loan interest accrual |

Accruals are posted using the interest amount computed with the new interest basis |

OL |

VAMI |

Value dated amendment on loan contracts |

When the principal amount, interest rate, interest basis or maturity date is changed in a contract as part of value dated amendments, interest computation is revised. |

OL |

ROLL |

Split rollover processing |

New Interest basis selected in the split rollover screen is defaulted to the child contracts and interest computation is done |

OL |

Consolidated rollover processing |

New Interest basis selected in the consolidated rollover screen is defaulted to the child contract and interest computation is done. All parent contracts should have the same (30SPL/360) interest basis |

|

OL |

Consolidated + split rollover processing |

All parent contracts should have the same (30SPL/360) interest basis. The child is defaulted with the interest basis selected in the consolidated rollover screen. |

|

OL |

LIQD |

Loan Payment |

The main interest component which is computed with the new interest basis will be liquidated as part of LIQD |

Module |

Event Code |

Description |

Remarks |

LS |

INIT |

New drawdown booking |

Interest is computed with the new interest basis and the schedule details are populated accordingly |

LS |

CAMD |

Drawdown amendment |

When the interest basis is amended as part of contract amendment, the computation is revised as per the new interest basis from the value date of the contract. |

LS |

LIQD |

Drawdown repayment |

The main interest component which is computed with the new interest basis is liquidated as part of LIQD |

LS |

VAMI |

Value dated amendment on drawdown contracts |

When the principal amount or maturity date is changed in a contract as part of value dated amendments, interest computation is revised |

LS |

MRFX |

Margin rate revision |

When margin rate is revised, interest computation is revised |

LS |

ROLL |

Drawdown split rollover processing |

New Interest basis selected in the split rollover screen is defaulted to the child contracts and interest computation is done |

LS |

Drawdown consolidated rollover processing |

New Interest basis selected in the consolidated rollover screen is defaulted to the child contract and interest computationis done. All parent contracts should have the same (30SPL/360) interest basis |

|

LS |

Drawdown consolidated + split rollover processing |

All parent contracts should have the same (30SPL/360) interest basis. The child is defaulted with the interest basis selected in the consolidated rollover screen. |

|

LS |

IRFX |

Drawdown interest rate fixing |

Interest is computed with the new interest basis and the schedule details are populated accordingly |

LS |

IRAM |

Drawdown interest rate amendment |

When interest rate is amended for a contract having new interest basis, interest is recomputed and the schedule details are populated accordingly |

LS |

PRAM |

Participant amendment processing |

When participant ratio amendment is done, the interest computation is revised |

OL |

INIT |

New loan booking |

Interest is computed with the new interest basis and the schedule details will be populated accordingly |

OL |

ACCR |

Loan interest accrual |

Accruals are posted using the interest amount computed with the new interest basis |

OL |

VAMI |

Value dated amendment on loan contracts |

When the principal amount, interest rate, interest basis or maturity date is changed in a contract as part of value dated amendments, interest computation is revised. |

OL |

LIQD |

Loan Payment |

The main interest component which is computed with the new interest basis is liquidated as part of LIQD |

Example 1: (Partial principal payment on contract with only 1 bullet schedule)

- Value date: 10-Jan-2019

- Maturity date: 10-Jun-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 151

- Number of Calendar Months: 6-1 = 5

- Computation Days: 5 * 30 = 150

- Interest Amount: 100,000 * 150 * 2% / 360 = 833.33

- Daily Accrual Amount: 833.33/151 = 5.52

- Schedule 1: Bullet (10-Jan-2019 to 10-Jun-2019)

- Interest Due: 833.33

- Principal Due: 100,000.00

- Total Due: 100,833.33

In this example, if you want to partially pay the principal, you should enter the value date, limit date and schedule date as 10-Jun-2019. This populates the amount as 100,833.33. You are allowed to modify the amount field to any value below 100,000.00.

Example 2: (Partial principal payment on contract with 4 monthly and 1 bullet schedules)

- Value date: 10-Jan-2019

- Maturity date: 10-Jun-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- No of Schedules: 4 Monthly + 1 Bullet

- Interest Computation (monthly): 100,000 * 30 * 2% / 360 = 166.66

- Schedule 1: Monthly (10-Jan-2019 to 10-Feb-2019)

- Total Due: 20,000.00 + 166.66 = 20,166.66

- Schedule 2: Monthly (10-Feb-2019 to 10-Mar-2019)

- Total Due: 20,000.00 + 166.66 = 20,166.66

- Schedule 3: Monthly (10-Mar-2019to 10-Apr-2019)

- Total Due: 20,000.00 + 166.66 = 20,166.66

- Schedule 4: Monthly (10-Apr-2019to 10-May-2019)

- Total Due: 20,000.00 + 166.66 = 20,166.66

- Schedule 5: Bullet (10-May-2019 to 10-June-2019)

- Total Due: 20,000.00 + 166.66 = 20,166.66

In this example, if you want to partially pay the principal till Schedule 4 (previous schedules unpaid), you should enter the value date, limit date and schedule date as 10-May-2019. This populates the amount as 80,666.64. You are allowed to modify the amount field to any value below 80,666.64.

The interest computation considers the number of days as per the below logic.

- For monthly schedules below changes are done,

- Number of days for interest computation are arrived as 30 for all monthly interest/principal payment schedules.

- The calculated interest is accrued over the actual number of days between the value date and maturity date of the contract. The interest computation and accrual are proportionate if the actual number of days for the monthly schedule is 30.

Example 1:

- Value date: 15-Jan-2019

- Maturity date: 16-Feb-2019

- Actual no of days: 31

- Computation days: 30

- For quarterly schedules below changes are done,

- Number of days for interest computation are arrived as 90 for all quarterly interest/principal payment schedules.

- The calculated interest is accrued over the actual number of days between the value date and maturity date of the contract. The interest computation and accrual are proportionate if the actual number of days for the quarterly schedule is 90.

Example 1:

- Value date: 10-Apr-2019

- Maturity date: 10-Jul-2019

- Actual no of days: 91

- Computation days: 90

- For bullet schedules below changes will be done,

- OBCL calculates the number of calendar months between the value date and maturity date of the contract, excluding the calendar month of the value date. The number of calendar months derived are then be multiplied by 30 to arrive the total number of computation days.

- The calculated interest is accrued over the actual number of days between the value date and maturity date of the contract. The interest computation and accrual are proportionate if the actual number of days is multiple of 30.

Example 1: (Actual number of days is greater than computation days)

- Value Date: 15-Jan-2019

- Maturity Date: 25-Apr-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 100

- Number of Calendar Months: 4-1 = 3

- Computation Days: 3 * 30 = 90

- Interest Amount: 100,000 * 90 * 2% / 360 = 500

- Daily Accrual Amount: 500/100 = 5

Example 2: (Actual number of days is less than computation days)

- Value Date: 15-Jan-2019

- Maturity Date: 10-Apr-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 85

- Number of Calendar Months: 4-1 = 3

- Computation Days: 3 * 30 = 90

- Interest Amount: 100,000 * 90 * 2% / 360 = 500

- Daily Accrual Amount: 500/85 = 5.88

Example 3: (Actual number of days is less than computation days)

- Value Date: 15-Jan-2019

- Maturity Date: 10-Feb-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 26

- Number of Calendar Months: 2-1 = 1

- Computation Days: 1 * 30 = 30

- Interest Amount: 100,000 * 30 * 2% / 360 = 166.66

- Daily Accrual Amount: 166.66/26 = 6.41

However, the amount which is accrued daily is arrived as interest computed / actual number of days in this example.

Example 4: (Value date and maturity date in same calendar month)

- Value Date: 01-Jan-2019

- Maturity Date: 25-Jan-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 24

- Computation Days: 24

- Interest Amount: 100,000 * 24 * 2% / 360 = 133.33

- Daily Accrual Amount: 133.33/24 = 5.55

Note

If the value date and maturity date of the contract is within the same calendar month, then the interest is computed for the actual number of days between value date and maturity date.

- In cases where the schedules are defined as monthly + bullet (last schedule), below changes are done,

- Number of days for interest computation are arrived as 30 for all monthly interest/principal payment schedules

- For the last bullet schedule, if the schedule start date and maturity date of the contract falls in different calendar months, OBCL calculates the number of calendar months between the schedule start date and maturity date of the contract, excluding the calendar month of the schedule start date. The number of calendar months derived are then be multiplied by 30 to arrive the total number of computation days.

- For the last bullet schedule, if the schedule start date and maturity date of the contract falls in the same calendar month, then the interest is computed for the actual number of days between the schedule start date and maturity date of the contract.

- The calculated interest is accrued over the actual number of days between the schedule start date and maturity date of the contract. The interest computation and accrual are proportionate if the actual number of days is multiple of 30

Example 1: 3 Monthly + 1 Bullet Interest Payment Schedules (Bullet schedule start date & end date in different calendar months)

- Value Date: 15-Jan-2019

- Maturity Date: 10-May-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 116

- No of Schedules: 3 Monthly + 1 Bullet

- Interest Computation (monthly): 100,000 * 30 * 2% / 360 = 166.66

Schedule 1: Monthly (15-Jan-2019 to 15-Feb-2019)

- Daily Accrual Amount: 166.66 / 31 = 5.37

- Interest Due 166.66

Schedule 2: Monthly (15-Feb-2019 to 15-Mar-2019)

- Daily Accrual Amount: 166.66 / 29 = 5.74

- Interest Due 166.66

Schedule 3: Monthly (15-Mar-2019 to 15-Apr-2019)

- Daily Accrual Amount: 166.66 / 31 = 5.37

- Interest Due 166.66

Schedule 4: Bullet (15-Apr-2019 to 10-May-2019)

- Interest Computation (bullet): 100,000 * 30 * 2% / 360 = 166.66

- Daily Accrual Amount: 166.66 / 25 = 6.66

- Interest Due 166.66

Example 2: 3 Monthly + 1 Bullet Interest Payment Schedules (Bullet schedule start date & end date in the same calendar month)

- Value Date: 15-Jan-2019

- Maturity Date: 28-Apr-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 104

- No of Schedules: 3 Monthly + 1 Bullet

- Interest Computation (monthly): 100,000 * 30 * 2% / 360 = 166.66

Schedule 1: Monthly (15-Jan-2019 to 15-Feb-2019)

- Daily Accrual Amount: 166.66 / 31 = 5.37

- Interest Due 166.66

Schedule 2: Monthly (15-Feb-2019 to 15-Mar-2019)

- Daily Accrual Amount: 166.66 / 29 = 5.74

- Interest Due 166.66

Schedule 3: Monthly (15-Mar-2019 to 15-Apr-2019)

- Daily Accrual Amount: 166.66 / 31 = 5.37

- Interest Due 166.66

Schedule 4: Bullet (15-Apr-2019 to 28-Apr-2019)

- Interest Computation (bullet): 100,000 * 13 * 2% / 360 = 72.22

- Daily Accrual Amount: 72.22 / 13 = 5.55

- Interest Due 72.22

- In cases where the schedules are defined as quarterly + bullet (last schedule), below changes are done,

- Number of days for interest computation is arrived as 90 for all quarterly interest/principal payment schedules

- For the last bullet schedule, if the schedule start date and maturity date of the contract falls in different calendar months, OBCL calculates the number of calendar months between the schedule start date and maturity date of the contract, excluding the calendar month of the schedule start date. The number of calendar months derived are then be multiplied by 30 to arrive the total number of computation days.

- For the last bullet schedule, if the schedule start date and maturity date of the contract falls in the same calendar month, then the interest is computed for the actual number of days between the schedule start date and maturity date of the contract.

- The calculated interest is accrued over the actual number of days between the schedule start date and maturity date of the contract. The interest computation and accrual are proportionate if the actual number of days is multiple of 90 for quarterly schedules or multiple of 30 for the last bullet schedule.

Example 1: 2 Quarterly + 1 Bullet Interest Payment Schedules (Bullet schedule start date & end date in different calendar months)

- Value Date: 10-Jan-2019

- Maturity Date: 10-September-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 243

- No of Schedules: 2 Quarterly + 1 Bullet

- Interest Computation (quarterly):100,000 * 90 * 2% / 360 = 500.00

Schedule 1: Quarterly (10-Jan-2019 to 10-Apr-2019)

- Daily Accrual Amount: 500.00 / 90 = 5.55

- Interest Due 500.00

Schedule 2: Quarterly (10-Apr-2019 to 10-Jul-2019)

- Daily Accrual Amount: 500.00 / 91 = 5.49

- Interest Due 500.00

Schedule 3: Bullet (10-Jul-2019 to 10-Sep-2019)

- Interest Computation (bullet): 100,000 * 60 * 2% / 360 = 333.33

- Daily Accrual Amount: 333.33 / 62 = 5.37

- Interest Due 333.33

Example 2: 2 Quarterly + 1 Bullet Interest Payment Schedules (Bullet schedule start date & end date in the same calendar month)

- Value Date: 10-Jan-2019

- Maturity Date: 28-Jul-2019

- Principal: 100,000.00

- Interest Rate: (1.5% + 0.5%) = 2%

- Actual no of days: 199

- No of Schedules: 2 Quarterly + 1 Bullet

- Interest Computation (quarterly):100,000 * 90 * 2% / 360 = 500.00

Schedule 1: Quarterly (10-Jan-2019 to 10-Apr-2019)

- Daily Accrual Amount: 500.00 / 90 = 5.55

- Interest Due 500.00

Schedule 2: Quarterly (10-Apr-2019 to 10-Jul-2019)

- Daily Accrual Amount: 500.00 / 91 = 5.49

- Interest Due 500.00

Schedule 3: Bullet (10-Jul-2019 to 28-Jul-2019)

- Interest Computation (bullet): 100,000 * 18 * 2% / 360 = 100.00

- Daily Accrual Amount: 100.00 / 18 = 5.55

- Interest Due 100.00

3.6 Rate Conversion Processing

- Final rate is always be per annum rate.

- The final annual rate is resolved based on the following

Parameter

Values

Rate Basis

Not Applicable/Per Annum/Per Month/Quote basis

- Changes are done in arriving at the resolved rate based on new parameters during the save of OL account and during VAMI/Rate revision cascade processes as well.

- After auto rate revision, existing rate basis gets re-defaulted by the system.

3.6.1 Linear Rate with Rate Basis as Per Month/Per Annum/Not Applicable

- If ‘Rate Method’ is ‘Rate/Rate code’ and the ‘Rate Basis’ is ‘Per Annum/Not Applicable’, then rate calculation is always in per annum

- If ‘Rate Method’ is maintained as ‘Rate/Rate code’ at OL product level and rate basis is Per Month, the system calculates the per annum rate as Rate per Month *12 This rate is displayed as Final rate on save

3.6.2 Linear Rate with Rate Basis as Quota Basis

If ‘Rate Method’ is ‘Rate/Rate code’ and ‘Rate Basis’ is ‘Quote Basis’, the final rate is based on the ‘Quote Basis’ at float rate maintenance level.

Float rate per annum is derived as below depending on the quote basis:

Quote basis |

Resolved Rate |

Exponential-252 |

{(((1+Float rate)^(1/252)) –1 )}*YEAR |

Exponential-365 |

{(((1+Float rate)^(1/365)) –1 )}*YEAR |

Linear360 |

Float rate/360*YEAR |

Days in year is the ‘Interest Basis’ denominator used for the ‘Main Interest’ component.

3.6.3 Exponential Rate with Rate Basis as Per month/Per annum/Not Applicable

- If 'Rate Method' type is maintained as 'Exponential Rate', the calculations for rate resolution is based on exponential method

- If 'Rate Method' type is maintained as 'Exponential Rate' and the 'Rate Basis' is 'Per Month', then the system calculates the per annum rate as ((1+Rate per Month)^12)-1

3.6.4 Exponential Rate with rate basis as quote basis

If 'Rate Method' is 'Exponential Rate' and 'Rate Basis' is 'Quote Basis', the final rate is resolved as 'Float Rate Per Annum’.

Depending on the 'Quote Basis', the 'Floating Rate Per Annum' is calculated as below:

Quote basis |

Float Rate per Annum |

Exponential-252 |

{1+((1+Float rate)^(1/252) –1 )}^YEAR-1 |

Exponential-365 |

{1+((1+Float rate)^(1/365) –1 )}^YEAR-1 |

Linear 360 |

{1+(Float rate/360) }^YEAR-1 |

Year is the ‘Interest Basis’ denominator used for the ‘Main Interest’ component.

Note

If any spread is fetched as maintained in OL module it is applied to the final resolved rate only.