This topic contains the following subtopics:

4)Credit Default Swap Contract Input

5)Credit Default Swap Pre-Settlement Input

6)Credit Default Swap Pre-Settlement Summary

Credit default swap (CDS) feature is a financial derivative or contract that allows you to swap or offset your credit risk with that of another investor.

For example, if a lender is worried that a borrower is going to default on a loan, the lender could use a CDS to offset or swap that risk. Protection buyer makes periodic or one-time payments to the protection seller, who collects the premium in exchange for making payment in whole or in partial in case of default.

CDS are over-the-counter (OT) transactions. These OT transactions are similar to buying or selling insurance contracts on a corporation or sovereign entity’s debt, without being regulated by insurance regulators (unlike insurance, it is not necessary to own the underlying debt to buy protection using CDS). Before trading, institutional investors and dealers enter into an International Swap and Derivative Association (ISDA) Agreement, setting up the legal framework for trading.

The following functionalities are required in the system to capture the maintenance and the complete life cycle of a CDS contract:

•Underlying details for a CDS.

•Contract terms such as credit events maintenance.

•Terms of exercise, standard contract features, recovery factor, premium type, and settlement details.

•Contract capture with the respective Premium schedules as required.

•Advice and event generation for accrual/amortization, booking, maturity, settlement, and exercise.

•Provision for handling information on pre-settlement events such as termination or exercise.

CDS uses the Options Branch Parameters which are maintained in the Options module.

For more information on Branch Parameters, refer the Maintain Branch Parameters section in this guide.

note: The user must de-select Delta Accounting Required in Option Branch Parameter screen to perform CDS.

Context:

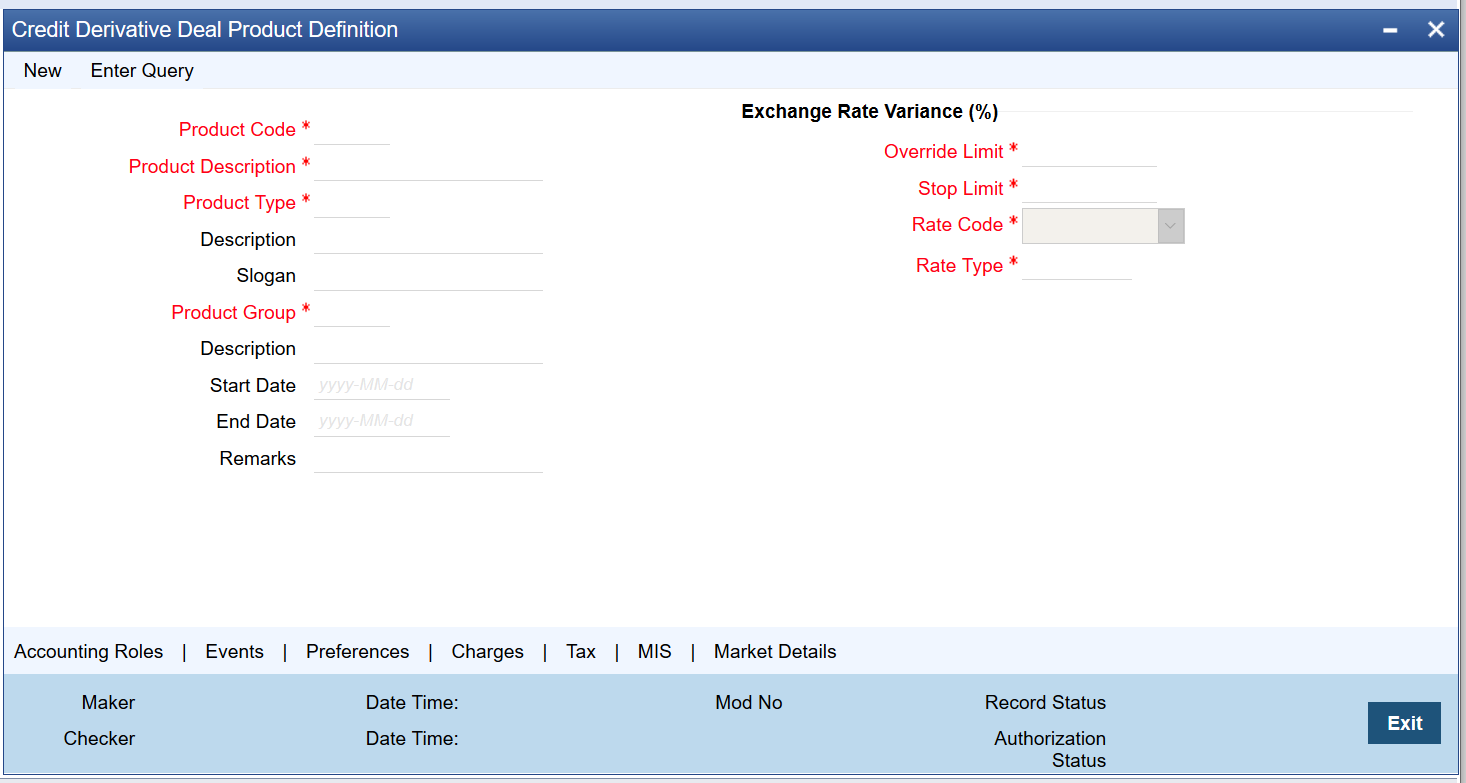

The credit deal product is maintained at the Credit Derivative Deal Product Definition screen.

note: All fields marked with an asterisk (*) are mandatory.

1.On the Home Page, enter DCDDLPRD in the text field, and then click the next arrow.

Step Result: Credit Definition Deal Product Definition screen is displayed.

Figure 1:Credit Definition Deal Product Definition

2.On the Credit Derivative Deal Product Definition screen, specify the details as required. For more information about credit derivative deal maintenance, see “Credit Derivative Deal Product Definitions” in Securities User Guide.

note: To use CDS option, ensure to select the unique CD code for CDS option.

3.On the Credit Derivative Deal Product Definition screen, click Preferences.

Step Result: Preferences screen is displayed.

Figure 2:Preferences - Main Tab

4.On Preferences screen, click the Credit Default Swaps tab.

Step Result: Credit Default Swaps page is displayed.

Figure 3:Credit Default Swaps

Tab

5.On the Credit Default Swaps tab, specify the fields, and click Ok.

For more information on the fields, refer to Table 8.1: Credit Default Swap - Field Description

Table 8.1: Credit Default Swap - Field Description

|

Field |

Description |

|---|---|

|

Deal Type |

Specify whether the deal product that bank is buying CDS or selling CDS. note: The user can change this preference for a particular deal. |

|

Brokerage Allowed |

Select the Brokerage Allowed check box to involve brokerage. Indicates that CDS deals for the selected deal product can involve brokerage. |

|

Contract Type |

Select the Contract Type from the drop-down list. The available options are: •Trade •Hedge Indicates whether the type of the contract is Trade deals or Hedge deals. note: The user can change this preference for a particular deal. |

Table 8.2: Credit Default Swaps Tab - Default Parameters Field Description

|

Field |

Description |

|---|---|

|

Default Type |

Select the type of default with several underlying securities from the drop-down list. The drop-down list shows the following options: •FIRST TO DEFAULT •Nth TO DEFAULT •LAST TO DEFAULT |

|

Default Number |

Specify the default number in this field, if the Default Type is selected as Nth TO DEFAULT. |

|

Recovery Factor |

Specify the cash recovery percentage in this field. |

|

Settlement Includes Premium |

Select the Settlement Includes Premium check box to included premium in settlement for credit event exercise. Indicates whether settlement for credit event exercise must include premium or the premium is suppressed with accrual reversed. |

Table 8.3: Credit Default Swaps - Delivery Details Field Description

|

Field |

Description |

|---|---|

|

Security Product |

Click on the search icon and select the deal product from the security product list, to create a deal for Delivery Type as Physical. |

|

Security Portfolio |

Click on the search icon and select the portfolio from the list of values, to create underlying deal for physical settlement. |

|

Delivery Type |

Select the Delivery Type from the drop-down list. The available options are: •Cash •Physical •External Indicates whether settlement for credit event exercise must include premium or the premium is suppressed with accrual reversed. |

Table 8.4: Credit Default Swaps - Premium Details Field Description

|

Field |

Description |

|---|---|

|

Premium Type |

Select the premium payment type from the drop-down list. The available options are: •Advance •Arrears |

Table 8.5: Credit Default Swaps - Premium Amortization Details Field Description

|

Field |

Description |

|---|---|

|

Amortization Of Premium Required |

Select the Amortization Of Premium Required check box, if premium amortization is required for PRAT event. Indicates whether the premium amortization is required for PRAT event. note: This field is applicable only if the Premium Type is selected as Advance. |

|

Component |

Specify the amount tag for amortization. note: This field is applicable only if the user selected the Amortization of Premium Required field. |

|

Start Reference |

Specify the start reference date. This can either be the Value Date or the Calendar Date. If the user specifies Value Date as the Start Reference, the settlement schedule is calculated using the frequency and frequency units concerning the contract value date. If the start reference is the Calendar date, the settlement schedule is calculated based on the frequency, frequency units, Start Day, start weekday, and start month. |

|

Frequency |

Specify the frequency. The available options are: •Daily •Weekly •Monthly •Quarterly •Half Yearly •Yearly |

|

Frequency Units |

Specify the frequency units. The number of frequency units after which a schedule can repeat. For example, a monthly frequency with a frequency unit of 2 is effectively a bi-monthly schedule. |

|

Start Weekday |

Specify the Start Weekday only if the Frequency is Weekly. Select any day from Sunday to Saturday.This is the day of the Week on which a schedule must start. |

|

Start Day |

Select any day of the month from the 1st to the 31st. Indicate the Start Day, if the Frequency is selected as Daily or Weekly.This is the day on which a schedule must start. |

|

Start Month |

Specify the Start Month only in case of Quarterly, Half-yearly, and Yearly frequencies. This is the month from which a schedule must start. |

|

Adhere to Month End |

Select the Adhere to Month End check box, if the schedule must adhere to month ends. Indicates whether a schedule must adhere to month ends, if the maturity date is a day less than the month-end date. |

Table 8.6: Credit Default Swap - Premium Accrual Details Field Description

|

Field |

Description |

|---|---|

|

Accrual Of Premium Required |

Select the Accrual Of Premium Required check box, if premium amortization is required for PRAC event. Indicates whether the premium amortization is required for PRAC event. note: This field is applicable, if the Premium Type is selected as Arrears. |

|

Frequency |

Specify the frequency. The available options are: •Daily •Weekly •Monthly •Quarterly •Half Yearly •Yearly |

|

Frequency Units |

Specify the frequency units. The number of frequency units after which a schedule can repeat. For example, a monthly frequency with a frequency unit of 2 is effectively a bi-monthly schedule. |

|

Start Day |

Select any day of the month from the 1st to the 31st. Indicates the Start Day, if the Frequency selected is Daily or Weekly.This is the day on which a schedule should start. |

|

Start Weekday |

Specify the Start Weekday only if the Frequency is Weekly. Select any day from Sunday to Saturday.This is the day of the Week on which a schedule must start. |

|

Start Month |

Specify the Start Month only in case of Quarterly, Half-yearly and Yearly frequencies. This is the month from which a schedule must start. |

|

Numerator Method |

Select the method that is used to calculate the number of days between the schedule start and end dates for calculating the settlement amount from the adjoining drop-down list. The list displays the following values: •30 EURO •30-US •30-ISDA •0-PSA •Actual •Actual-Japanese |

|

Denominator Method |

Select the method that is used to calculate the number of days in a year for the calculation of the settlement amount from the drop-down list. The list displays the following values: •Actual •365 •360 |

|

Denominator Basis |

Specify whether the difference between the Strike Rate and the Reference Rate is to be taken for the whole year or for the schedule period during Settlement Amount calculation. The basis can either be Per Period or Per Annum. |

Table 8.7: Credit Default Swaps - Premium Accrual Liquidation Details Field Description

|

Field |

Description |

|---|---|

|

Start Reference |

Specify the start reference date. This can either be the Value Date or the Calendar Date. If the user specifies Value Date as the Start Reference, the settlement schedule is calculated using the frequency and frequency units concerning the contract value date. If the start reference is the Calendar date, the settlement schedule is calculated based on the frequency, frequency units, Start Day, start weekday, and start month. note: This field is applicable only if the user selected the Amortization of Premium Required field. |

|

Frequency |

Specify the frequency. The available options are: •Daily •Weekly •Monthly •Quarterly •Half Yearly •Yearly |

|

Frequency Units |

Specify the frequency units. The number of frequency units after which a schedule can repeat. For example, a monthly frequency with a frequency unit of 2 is effectively a bi-monthly schedule. |

|

Start Day |

Select any day of the month from the 1st to the 31st. Indicate the Start Day, if the Frequency selected is Daily or Weekly.The schedule must start on this day. |

|

Start Weekday |

Specify the Start Weekday only if the Frequency is Weekly. Select any day from Sunday to Saturday. In this day of the Week, a schedule must start. |

|

Start Month |

Specify the Start Month only in case of Quarterly, Half-yearly and Yearly frequencies. This is the month from which a schedule must start. |

|

Adhere to Month End |

Select the Adhere to Month End check box, if the schedule must adhere to month ends. Indicates whether a schedule must adhere to month ends, if the maturity date is a day less than the month-end date. |

Table 8.8: Credit Default Swaps - Revaluation Details Field Description

|

Field |

Description |

|---|---|

|

Revaluation source |

Select the option from the displayed list. •Internal •External •None |

|

Revaluation Level |

Select the Revaluation Level. The available options are: •Contract •Product Indicates the revaluation level. |

|

Revaluation Frequency |

Specify the frequency with which a portfolio is revalued. The revaluation frequency can be one of the following: •Daily •Monthly •Quarterly •Half yearly •Yearly |

|

Revaluation start day |

Specify the date on which revaluation must start during the month. |

|

Revaluation Start Weekday |

Specify the day to perform revaluation based on the revaluation frequency. |

|

Revaluation Start Month |

Specify the month based on revaluation frequency to perform revaluation. |

|

Rekey Required |

Select the Rekey Required check box, if the rekey value is required when the CDS contract is invoked for authorization. |

|

Contract Currency |

Select Contract Currency, if the currency is required when the CDS contract is invoked for authorization. |

|

Premium Currency |

Select Premium Currency, if the currency of premium is required when the CDS contract is invoked for authorization. |

|

Value Date |

Select Value Date, if the Value Date is required when the CDS contract is invoked for authorization. |

|

Maturity Date |

Select Maturity Date, if the Maturity date is required when the CDS contract is invoked for authorization. |

8.4 Credit Default Swap Contract Input

Context:

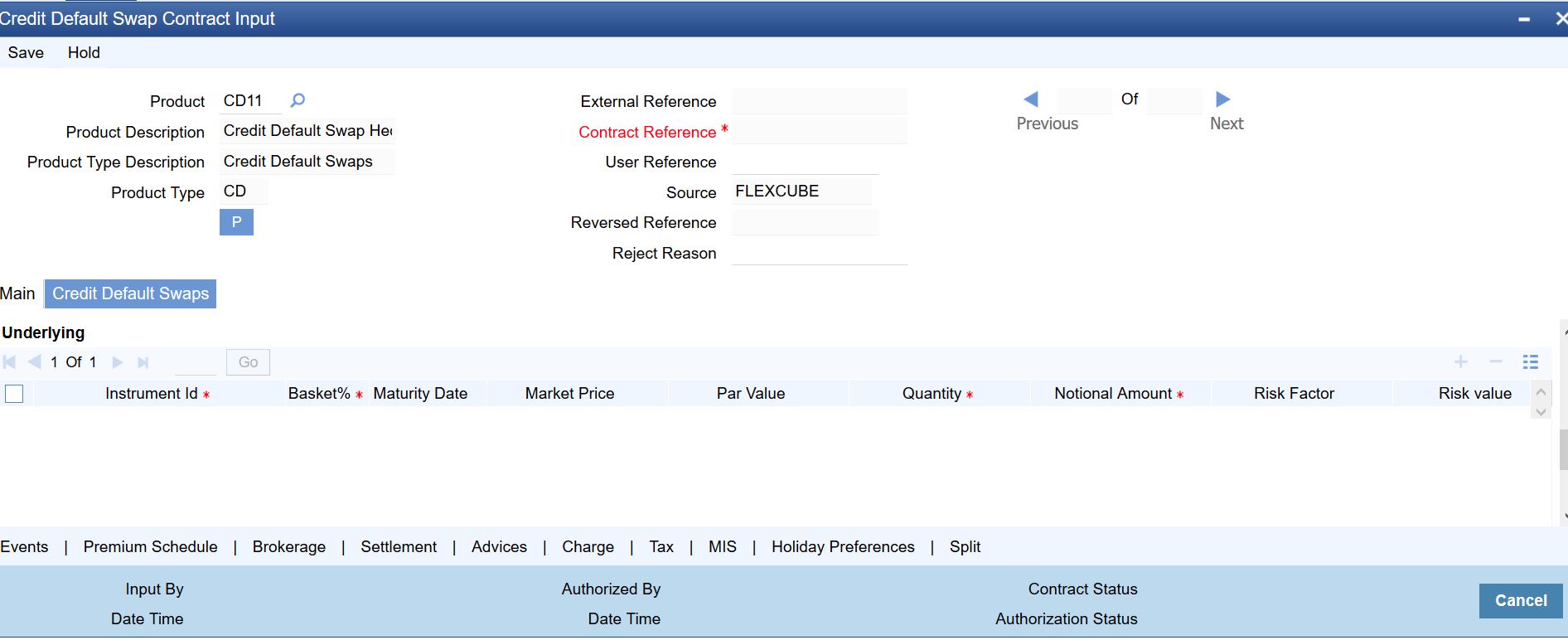

The CDS contract input and summary information are captured in the Credit Default Swap Contract Input screen.

note: All fields marked with an asterisk (*) are mandatory.

1.On the Home page, enter DCDCDSON in the text box, and then click the next arrow.

Step Result: Credit Default Swap Contract Input screen is displayed.

Figure 4:Credit Default Swap Contract Input

2.On Credit Default Swap Contract Input screen, under Main tab, specify the contract details.

For more information on the fields, refer to the Table 8.9: Credit Default Swap Contract Input and Main Tab - Field Description.

Table 8.9: Credit Default Swap Contract Input and Main Tab - Field Description

|

Field |

Description |

|---|---|

|

Product |

Click on the search icon and select the required CDS product from the displayed list. |

|

Product Description |

The System displays the description of the selected product. |

|

Product Type Description |

The System displays the description of the selected product type. |

|

Product Type |

The System displays the type of the selected product. |

|

P |

Click P to populate the product details and to generate contract reference number. The system displays the External Reference, Contract Reference, User Reference, and Source details of the selected product. |

|

Reversed Reference |

The reference number displays the reversed and re-booked contract. |

|

Reject Reason |

Specify the Reject Reason Code for the payment reversal message. |

|

Main Tab |

|

|

Counterparty |

Select the unique code from the displayed list for identifying the customer. |

|

Trade Date |

Specify the Trade Date. Indicates the business date on which CDS deal is initiated. |

|

Booking Date |

Specify the Booking Date. Indicates the booking date on which the CDS contract option is added in the system |

|

Value Date |

Specify the Value Date. Indicates the value date which is the first date of the interest period. |

|

Maturity Date |

Specify the Maturity Date. Indicates the maturity date on which the contract expires. note: If the Maturity Date is less than the Value date, an error message is displayed. |

|

Currency |

Click the Search icon and select the unique code from the displayed list for identifying the currency of the CDS contract. |

|

Nominal Amount |

Enter the nominal amount in this field. note: If you enter a nominal amount below zero, then an error message is displayed in the system. |

|

Broker |

Click the Search icon and select the unique code for identifying the broker of the contract from the list. note: This field is applicable only if the user selected the brokerage allowed while maintaining the product preferences. |

|

Contract Type |

Select the contract type from the drop-down list. Indicates whether the contract type is Hedge or Trade. |

|

Buy or Sell |

Indicates the nature of the contract that bank is buying the contract or selling the contract. |

|

Deal Input Time |

Indicates the deal execution time at the time of deal booking received from front office. Default Time Format: YYYY-MM-DD HH:MM:SS:SSS. note: The user can change the format in the user setting option based on requirement. |

3.On the Credit Default Swap Contract Input screen, click the Credit Default Swaps tab.

Step Result: The Credit Default Swaps page is displayed.

Figure 5:Credit Default Swaps Tab

4.On the Credit Default Swap Contract Input screen, under Credit Default Swaps, specify the fields.

The user can modify the Default Parameters and Premium Details of the product in this section. For more information on the fields, refer to Table 8.10: Credit Default Swaps - Default Parameters and Premium Details - Field Description

Table 8.10: Credit Default Swaps - Default Parameters and Premium Details - Field Description

|

Field |

Description |

|---|---|

|

Delivery Type |

Select the Delivery Type option. The available options are: •Cash •Physical •External Indicates the type of settlement when the credit event is triggered. |

|

Recovery Factor |

Specify the cash recovery factor. |

|

Settlement Includes Premium |

Select the Settlement Includes Premium check box, if the settlement for credit event exercise must include premium or the premium is suppressed with accrual reversed. |

|

Premium Currency |

Click on the search icon and select the unique code from the list for identifying the premium currency |

|

Premium Amount |

Specify the premium amount of the contract. |

|

Premium Percent |

Specify the percentage of the premium amount for the contract. |

|

Premium Pay Date |

Specify the date to pay the premium amount. |

|

Premium Type |

Indicates the type of the premium. |

5.On the Credit Default Swap Contract Input screen, under Credit Default Swaps, specify the Underlying fields as required.

Figure 6:Credit Default Swap Tab

For more details on the fields, refer to Table 8.11: Credit Default Swaps - Underlying Field Description.

Table 8.11: Credit Default Swaps - Underlying Field Description

|

Field |

Description |

|---|---|

|

Instrument ID |

Indicates the instrument used as the underlying for the contract. |

|

Basket% |

Indicates the percentage portion of the basket constituted by the underlying instrument. |

|

Maturity Date |

Indicates the date on which the CDS contract expires. If the Maturity Date is less than or equal to Value Date, an error message is displayed. |

|

Market Price |

Indicates the market price of the underlying instrument |

|

PAR Value |

Indicates the current face value of the instrument. |

|

Quantity |

Indicates the number of units of the instrument. |

|

Notional Amount |

Indicates notional amount of the underlying instrument. note: If the notional amount is not greater than zero, then an error message is displayed. |

|

Risk Factor |

Indicates the risk factor associated with the underlying instrument. note: The Risk Factor Value must be between 0 and 1. |

|

Risk Value |

Indicates the value at risk of underlying instrument. |

8.5 Credit Default Swap Pre-Settlement Input

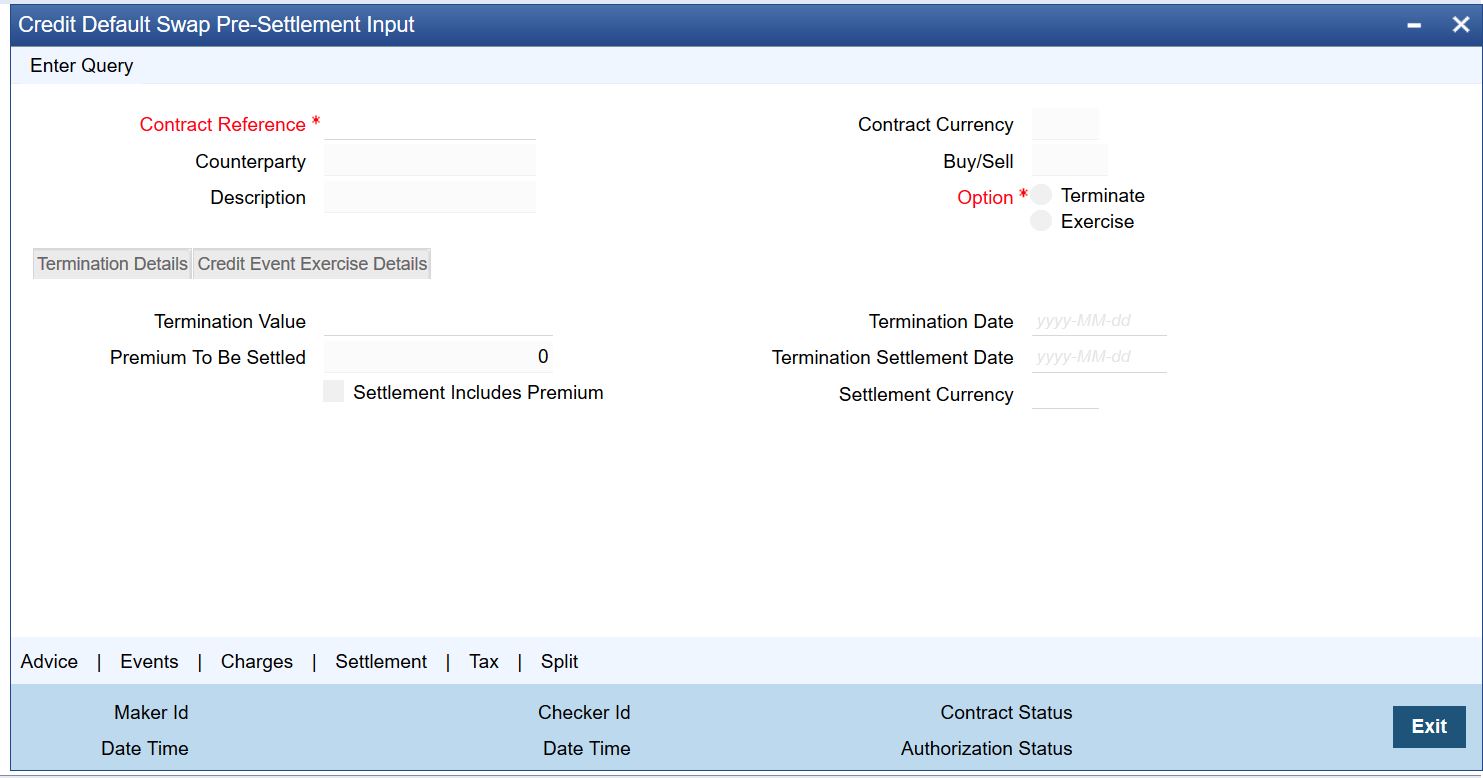

Context:

The CDS contract details for contract termination and contract exercise are captured in the Credit Default Swap Pre-Settlement Input screen.

note: All fields marked with an asterisk (*) are mandatory.

1.On the Home page, enter DCDCNTRM in the text box, and then click next arrow.

Credit Default Swap Pre-Settlement Input screen is displayed.

Figure 7:Credit Default Swap Pre-Settlement Input

2.On Credit Default Swap Contract Input screen, click Enter Query, and specify the contract details as required.

For more information on the fields, refer to the Table 8.12: Credit Default Swap Contract Input - Field Description.

Table 8.12: Credit Default Swap Contract Input - Field Description

|

Field |

Description |

|---|---|

|

Contract Reference |

Click the search icon and select the unique code from the list for identifying the contract for termination. |

|

Counterparty |

The system displays the counterparty of the selected contract. |

|

Description |

The system displays the brief description of the counterparty for the selected contract reference. |

|

Contract Currency |

Indicates the currency of the nominal amount. |

|

Buy/Sell |

Indicates whether the bank is buying the contract or selling the contract. |

|

Option |

Select either Terminate Option to terminate the contract or Exercise Option to exercise the contract. |

Click Execute Query to execute the selected option.

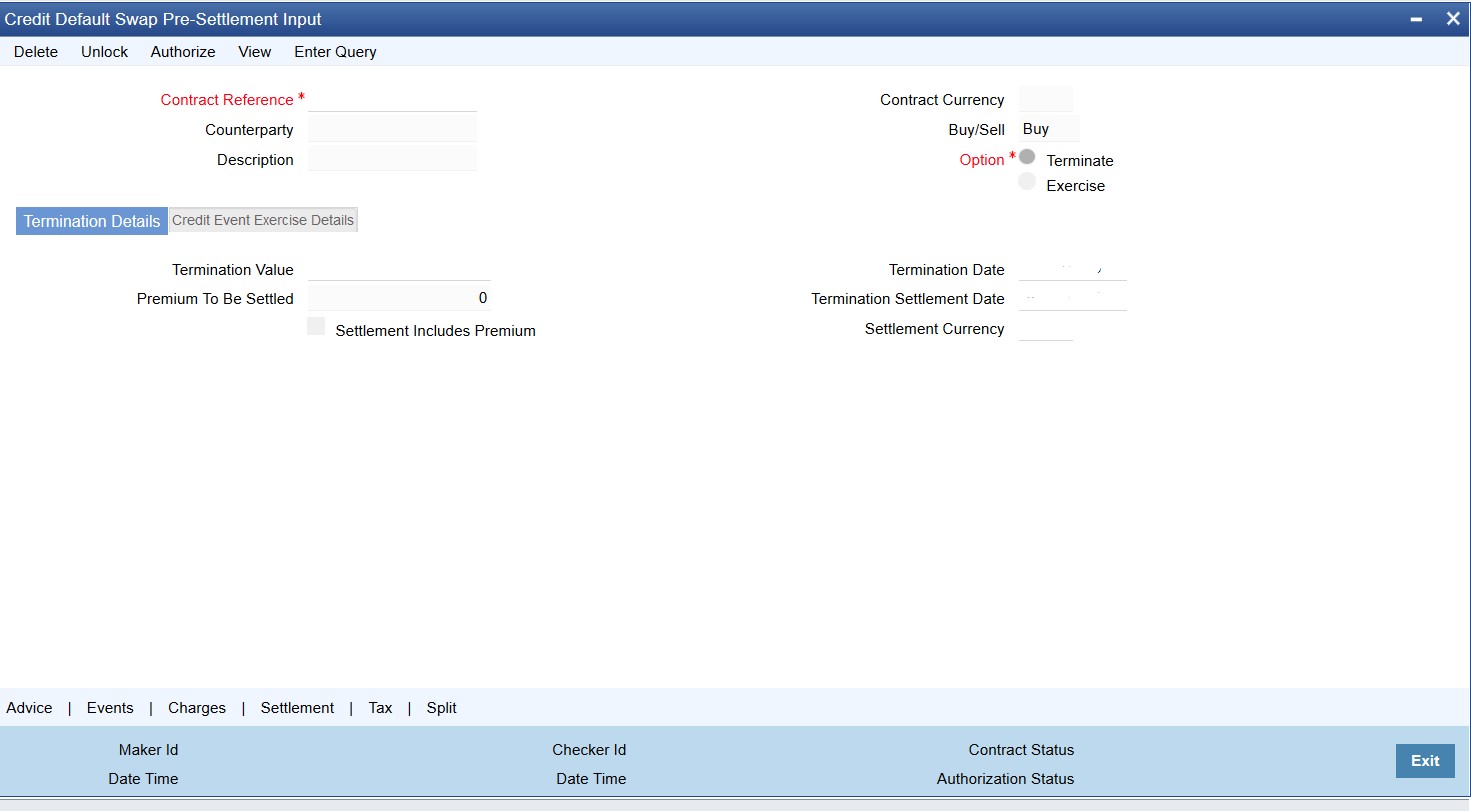

3.On the Credit Default Swap Pre-Settlement Input screen, click Termination Details.

Step Result: The Termination Details page is displayed.

.

Figure 8:Credit Default Swap Pre-Settlement Input - Termination Details Tab

4.On the Credit Default Swap Contract Input screen, under Termination Details, specify the fields.

For more information on the fields, refer to Table 8.13: Credit Default Swaps Contract Input- Termination Details Field Description

Table 8.13: Credit Default Swaps Contract Input- Termination Details Field Description

|

Field |

Description |

|---|---|

|

Termination Value |

Specify the Termination Value. note: Positive value denotes income and Negative value denotes expense. |

|

Premium to be Settled |

Indicates the premium for settlement as per the PUR_CDS_PREM_PACD amount tag for buying CDS and WRI_CDS_PREM_PACD for selling CDS. This field is mandatory, if the user selected the Settlement Includes Premium. |

|

Termination Date |

Indicates the effective date of contract termination. note: If the Termination Date is less than or equal to Value Date or if the Termination Date is greater than or equal to Maturity Date, an error message is displayed. |

|

Termination Settlement Date |

Indicates the settlement date on which the termination begins. note: If the Termination Settlement Date is less than or equal to the Termination Date, then an error message is displayed. |

|

Settlement Includes Premium |

Indicates whether settlement for credit event exercise must include premium or the premium is suppressed with accrual reversed. |

|

Settlement Currency |

Indicates the currency of the contract termination settlement. |

5.On the Credit Default Swap Pre-Settlement Input screen, click the Credit Event Exercise Details tab.

Step Result: The Credit Event Exercise Details page is displayed

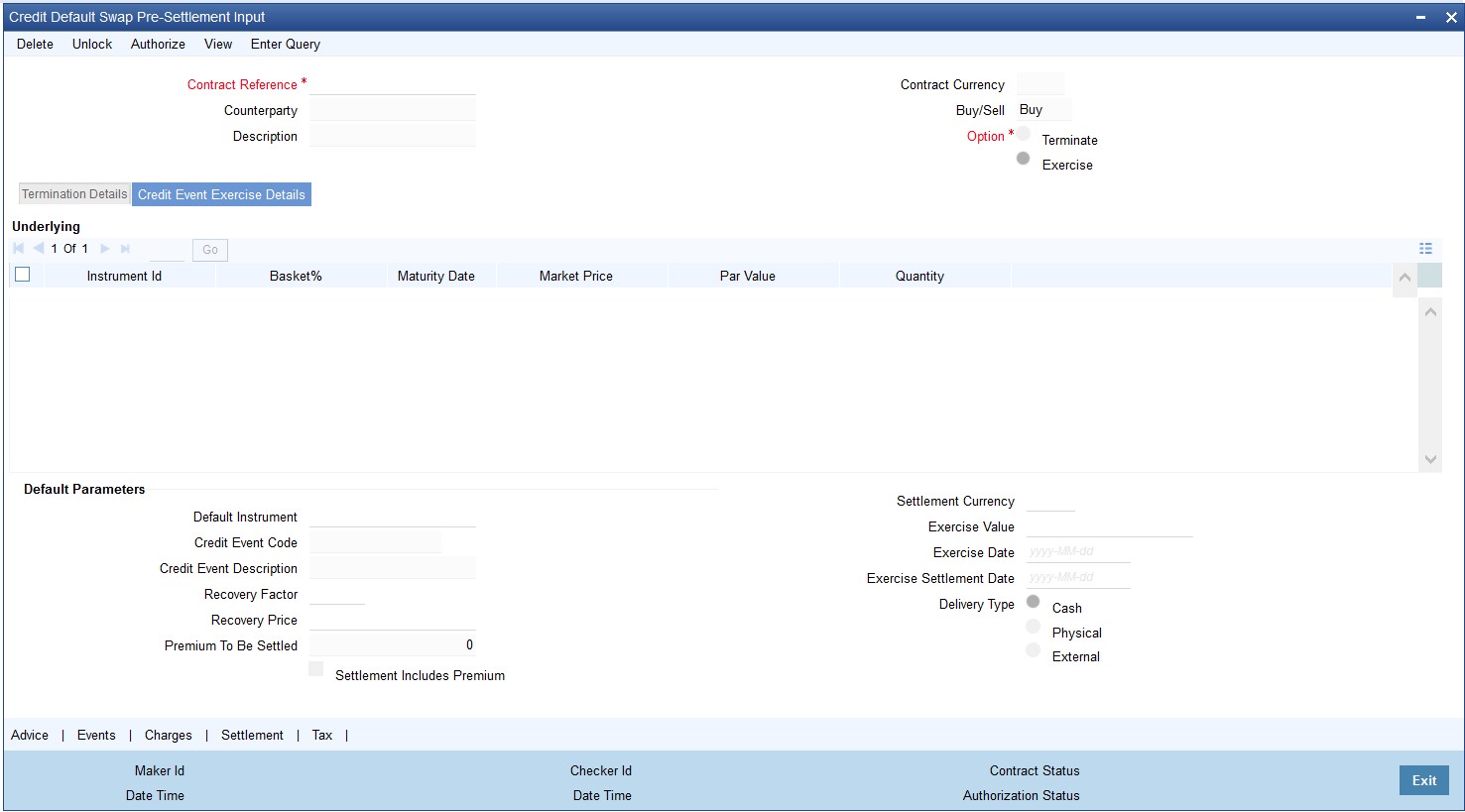

Figure 9:Credit Default Swap Pre-Settlement Input - Credit Event Exercise Details Tab

6.On the Credit Default Swap Contract Input screen, under Credit Event Exercise Details, specify the fields as required.

For more information on the fields, refer to Table 8.14: Credit Default Swap contract Input - Credit Event Exercise Details Field Description

.

Table 8.14: Credit Default Swap contract Input - Credit Event Exercise Details Field Description

|

Field |

Description |

|---|---|

|

Instrument ID |

Indicates the instrument used as the underlying for the contract. |

|

Basket% |

Indicates the percentage portion of the basket constituted by the underlying instrument. |

|

Maturity Date |

Indicates the date on which the CDS contract expires. If the Maturity Date is less than or equal to Value Date, an error message is displayed. |

|

Market Price |

Indicates the market price of the underlying instrument |

|

PAR Value |

Indicates the current face value of the instrument. |

|

Quantity |

Indicates the number of units of the instrument. |

|

Default Instrument |

Click the search icon and select the unique code from the displayed list for identifying the defaulted Instrument. |

|

Credit Event Code |

Click the search icon and select the unique code from the displayed list for identifying the event code causing the exercise. |

|

Credit Event Description |

The system displays the brief description of the selected credit event. |

|

Exercise Value |

Indicates whether the settlement must include accrued premium. |

|

Exercise Date |

Specify the effective of contract Exercise Date. note: If the Exercise Date is less than or equal to the Value Date and greater than the Maturity Date, an error message is displayed. |

|

Exercise Settlement Date |

Indicates the Settlement Date of the exercised contract. |

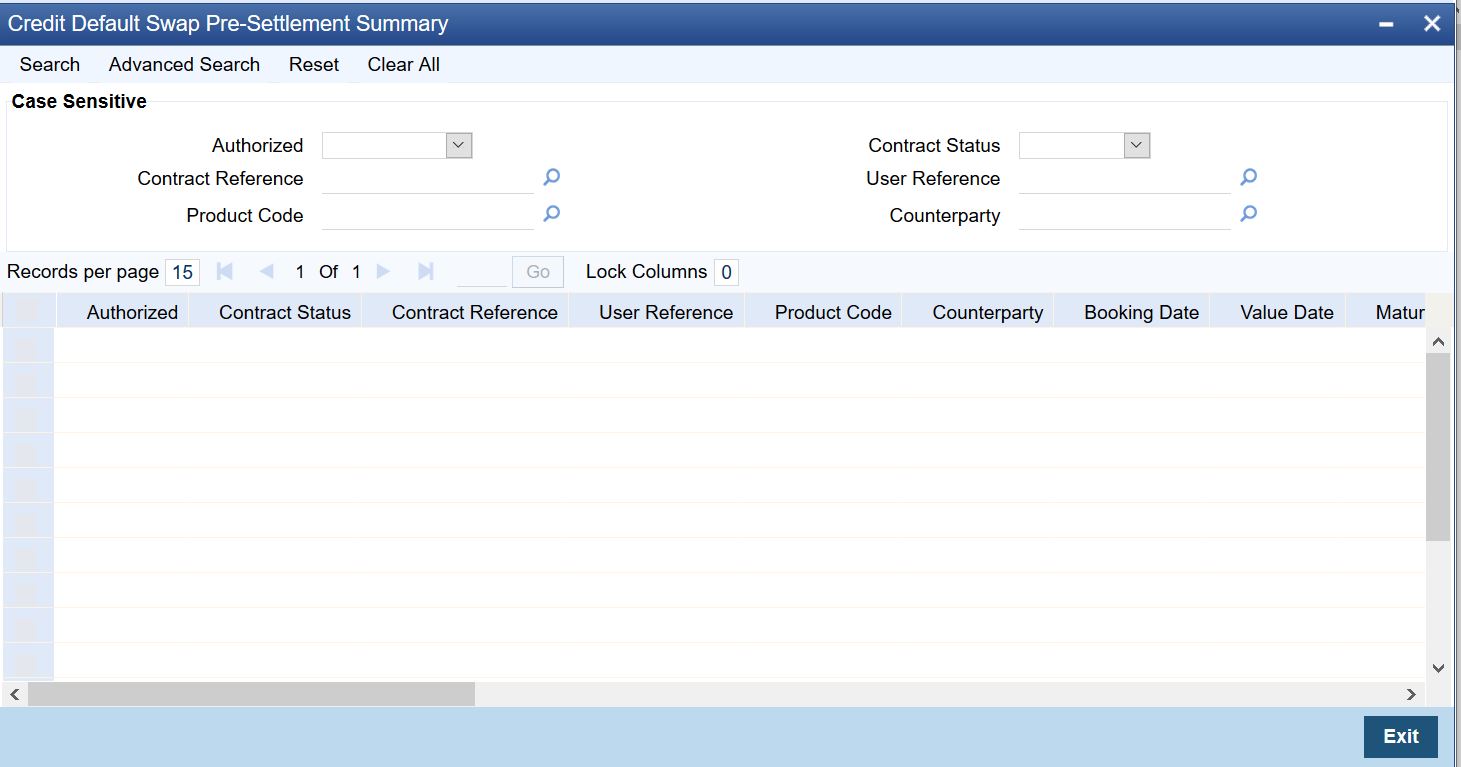

8.6 Credit Default Swap Pre-Settlement Summary

This topic provides the details to capture the CDS Contract Termination and CDS Contract Exercise summary.

Context:

The Credit Default Swap Pre-Settlement Summary screen displays the status on contract termination and contract exercise.

1.On the Home page, enter DCSCNTRM in the text box, and then click next arrow.

Step Result: Credit Default Swap Pre-Settlement Summary Screen is displayed.

Figure 10:Credit Default Swap Pre-Settlement Summary

2.On the Credit Default Swap Pre-Settlement Summary screen, click Search or Advanced Search to view the summary of the terminated contract and exercised contract records.

3.On the Credit Default Swap Pre-Settlement Summary screen, specify any one of the field, and click Search to fetch the status of the specific record based on the selected criteria.

For more information on the fields, refer to Table 8.15: Credit Default Swap Pre-Settlement Summary - Field Description.

Table 8.15: Credit Default Swap Pre-Settlement Summary - Field Description

|

Field |

Description |

|---|---|

|

Authorized |

Select the authorization status of the CDS contract from the drop-down list to fetch the records based on the authorization status. The available options are: •Authorized •Unauthorized |

|

Contract Status |

Select the CDS contract status from the drop-down list to fetch the records based on the contract status. The available options are: •Terminated •Exercised |

|

Contract Reference |

Specify the unique code of the contract reference number from the displayed list to fetch the record based on the contract reference. |

|

User Reference |

Specify the unique code of the user reference number to fetch the record based on the user reference. |

|

Counterparty |

Specify the unique code of the counterparty from the displayed list to fetch the record based on the counterparty. |

|

Product Code |

Specify the unique code of the product from the displayed list to fetch the record based on the product code. |

8.7 List of Glossary - Credit Default Swap

Credit Definition Deal Product Maintenance - 8.3 Deal Product Maintenance (p. 124).

Credit Default Swap Contract Input Screen - 8.4 Credit Default Swap Contract Input (p. 132).

Credit Default Swap Pre-Settlement Input - 8.5 Credit Default Swap Pre-Settlement Input (p. 136).

Credit Default Swap Pre-Settlement Summary - 8.6 Credit Default Swap Pre-Settlement Summary (p. 140).