Enable ORA_ERP_CONTROLLED_CONFIG Lookup Type

You must enable the mandatory new setup for the Account Hierarchy according to the updated guidelines.

Overview

According to the updated guidelines, you may have to run a new setup for the Account Hierarchy. If reports for previous years are required, then maintain the current JPK Hierarchy in Draft status. The old hierarchy must be temporarily activated and assigned to the proper Chart of Accounts, Natural Account segment.

Based on the directions provided by the Polish tax authorities:

- Accounts must be kept in accordance with the Accounting Act

- Branches or representative offices of foreign companies must also maintain accounts in accordance with the Accounting Act.

- There is no requirement for a specific Chart of Accounts hierarchy setup as was

the case for the JPK and JP parent accounts under the old format.

Users can use their standard Chart of Accounts as long as all their detailed accounts are mapped with the appropriate Industry Accounts under the S_12_1 mapping lookup. They must make sure that these are the correct accounts under the relevant ZOIs category (eg. ZOiS7).

These mandatory data elements are being added to the new format:

- Contractor (3rd party) Details

- New Trial Balance Format

- Common Control Section

- Common Detailed Journals and Account Analysis Section

- RPD Tax Section

- Asset Register (To be submitted in 2027)

To run the report in the current format, revert to the new hierarchy. Detailed directions on how to do this switch will be provided along with the new release.

Address Format for Legal Entity in Poland

You must follow the distinct format to set up the Address of the Polish Legal Entity:

- Navigate to Manage Address Formats and select the format for Poland, and Style for Postal Address.

This table lists the XML tags and the different elements that appear in the JPK header section and are used in the Poland address setup:

| Elements with XML Tags | Address Format |

|---|---|

| <etd:KodKraju>PL</etd:KodKraju> | Country |

| <etd:Wojewodztwo>mazowieckie</etd:Wojewodztwo> | State |

| <etd:Powiat>County-warsaw</etd:Powiat> | County |

| <etd:Gmina>Prov-warsaw</etd:Gmina> | Province |

| <etd:Ulica>ulic. Maja</etd:Ulica> | Street |

| <etd:NrDomu>7</etd:NrDomu> | Building |

| <etd:Miejscowosc>Warsaw</etd:Miejscowosc> | City |

| <etd:KodPocztowy>01-607</etd:KodPocztowy> | Postal Code |

Contractor (Third-Party) Details

This section includes information such as Customer and Supplier ID, their country codes, and their Tax registration numbers (TRN). All elements are available in the system and will be included in the new XML format. The prerequisite is that you must provide the third-party Tax Registration Numbers (TRN) in the Tax Registration setup at site, address, or third-party header level.

New Trial Balance Format

New classification markers are used to identify booking accounts at the level of the trial balance (Znaczniki Kont, ‘ZOiS’) segment. A specific lookup is used to provide information that indicates the type of industry, the company operates in. This lookup identifies the mapping between the Detailed and parent level accounts of the User’s Natural Account segment for Poland and the new classification from the S_12_1 account mapping. The Description field of the lookup used for the S_12_1 classification provides the ZOiS classification. In the following example, JEPL_JPK_S_12_1 lookup is defined and for other entries, the description is ZOiS7.

- The system already has a place holder (AR Invoice header: GLOBAL_ATTRIBUTE9 and AP Invoice header: GLOBAL_ATTRIBUTE7) for this number.

- Wherever implemented, and a number is stored, it is extracted in the proper

XML tag of the new report.

No action is required from the user.

This table displays requirements for the new Trial Balance Section for each Natural Account:

| JPK_KR_PD element | Polish Description | Analytical Description |

|---|---|---|

| S1 | Identyfikator konta ostatecznego zapisu (konta pomocniczego lub konta księgi głównej, jeżeli nie jest wymagany zapis na kontach pomocniczych) | Natural Account Code. The corporate Accounts must be mapped to the JEPL_JPK_S_12_1 lookup. When/If the requirement for deriving the external tax information from the system becomes mandatory, the natural account segment must be at least 12 digits to allow for the minimum length based on the Accounts defined by the Accounting Act, for the off-balance sheet accounts. A new hierarchy branch will be needed then as well, but it is not currently in scope. The S1 field will only report the final entry accounts and not the parent accounts similar to the previous version of JPK Accounting report. |

| S2 | Nazwa konta | Account Name (Description). Enter in Polish so that it will be extracted in Polish under the new report. |

| S3 | Identyfikator konta nadrzędnego | Parent account identifier. When the final entry account (S1) is of the first level and thus has no parent account, S3=S1. |

| S4 | Bilans otwarcia po stronie Winien w walucie polskiej | Opening balance on the Debit side in Polish currency. It refers to the balance in the beginning of the fiscal year. |

| S5 | Bilans otwarcia po stronie Ma w walucie polskiej | Opening balance on the Credit side in Polish currency. It refers to the balance in the beginning of the fiscal year. |

| S6 | Obroty konta po stronie Winien, w okresie którego dotyczy JPK | Turnover of the debit side account in the period to which the JPK applies. It refers to the period indicated by the parameters From Period – To Period during the execution of the report. |

| S7 | Obroty konta po stronie Ma, w okresie którego dotyczy JPK | Turnover of the credit side account in the period to which the JPK applies. It refers to the period indicated by the parameters From Period – To Period during the execution of the report. |

| S8 | Obroty konta po stronie Winien, w okresie od otwarcia ksiąg do daty końcowej okresu, którego dotyczy JPK | Account turnover on the debit side in the period from the opening of the books to the end date of the period covered by the JPK. This excludes the opening balance of the fiscal year on the debit side. |

| S9 | Obroty konta po stronie Ma, w okresie od otwarcia ksiąg do daty końcowej okresu, którego dotyczy JPK | Account turnover on the credit side in the period from the opening of the books to the end date of the period covered by the JPK. This excludes the opening balance of the fiscal year on the credit side. |

| S10 | Saldo po stronie Winien w walucie polskiej na datę końcową okresu, którego dotyczy JPK z uwzględnieniem bilansu otwarcia | Balance on the debit side in Polish currency as of the end date of the period covered by the JPK, taking into account the opening balance. |

| S11 | Saldo po stronie Ma w walucie polskiej na datę końcową okresu, którego dotyczy JPK z uwzględnieniem bilansu otwarcia | Balance on the credit side in Polish currency as of the end date of the period covered by the JPK, taking into account the opening balance. |

| S_12_1 | Znacznik konta wynikający z rozporządzenia w sprawie dodatkowego zakresu danych, o które należy uzupełnić prowadzone księgi rachunkowe | Markers mapping the account to the financial statement for entities preparing separate financial statements based on the Act on Accounting (B3IIa). This is a mandatory classification of all final entry accounts. |

| S_12_2 | Dodatkowy znacznik konta wynikający z rozporządzenia w sprawie dodatkowego zakresu danych, o które należy uzupełnić prowadzone księgi rachunkowe | Markers mapping the account to the financial statement for entities preparing separate financial statements based on the Act on Accounting. This is an optional classification only for those companies that need it. |

| S_12_3 | Dodatkowy znacznik konta wynikający z rozporządzenia w sprawie dodatkowego zakresu danych, o które należy uzupełnić prowadzone księgi rachunkowe (PD) | Mappings to tax tags of profit and loss and off-balance sheet accounts ). Currently off scope as the K group amounts are defined in the relative lookup manually, entering the information presented by external systems. |

Here are the important notes:

- All other values excluding S_12_1, S_12_2, and S_12_3, follow the standard functionality of the application.

- The old JPK format or release reports the detailed final entry natural account and its allocation under the triple digit JPK category code and single digit group category JPK code.

- Under the new Trial balance section, the final entry natural accounts are reported under the S1 field and for each level, the immediate parent account must be reported under the S3 field.

- If the highest-level parent accounts are also final entry accounts (not to be confused with the Top-Level Account which is not reported; these highest-level accounts are referenced as Synthetic Accounts), the S1 and S3 values are the same.

- The triple digit JPK category and single digit JPK group category classifications are no longer required.

The assignment of the newly introduced S_12_1, S_12_2, and S_12_3 attributes to the actual Natural Accounts used by Polish companies are set through these specific lookups.

- JEPL_JPK_S_12_1

- JEPL_JPK_S_12_2

- JEPL_JPK_S_12_3

Under this new configuration, the lookup code would be the current corporate natural account (actual parent and / or detailed account) assigned to the provided code S_12_1 (else S_12_2 wherever needed or S_12_3 for off-balance accounts, if used). The tag column identifiies the assigned attribute from the values provided by the tax authorities for the given industry and company.

Relation Between S1 and S3 Tags

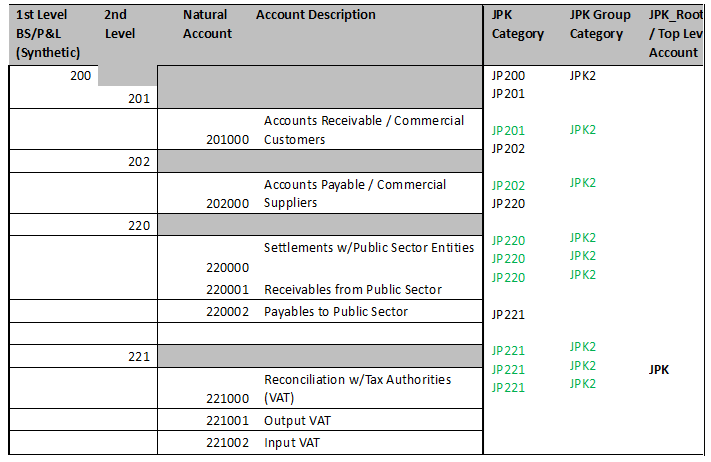

Under the JPK top-level account (existing from the present JPK account hierarchy structure requirements), you must define the actual hierarchy of your Natural Accounts with all the levels used, ending with your detailed natural accounts, as you use them for your corporate needs. Example below: 200 (Synthetic Account), 201(second parent account), 201000 (detailed account).

This image shows examples for JEPL_JPK_S_12_1, JEPL_JPK_S_12_2, and JEPL_JPK_S_12_3 lookups:

All accounts must be mapped under the S_12_1 listing. Those accounts that were not previously listed under the JPK report must also be included in the Account hierarchy under the new report. Such accounts will have the value INNE (other) for S_12_1 attribute. The JPK related triple digit category and single digit group category parent accounts and their hierarchy can remain as they are, with the relative hierarchy set as Draft, in case you need to provide an auditor with previous years data under the previous format. If you didn’t use JPK reporting before 2025, you do not need to create or maintain these parent accounts and their hierarchy in the application.

Controls Section

The controls section in the new format combines the two control sections from the previous JPK report into one section. No additional fields are introduced, and no action is needed from the user.

Detailed Journals and Account Analysis Section

This table shows the details of the JPK_KR_PD element:

| JPK_KR_PD element | Polish Description | Analytical Description |

|---|---|---|

| D1 | Numer zapisu w dzienniku, nadawany w sposób ciągły w roku obrotowym, zgodnie z wymogiem określonym w art. 14 ust. 2 i ust. 4 UoR, tj.: - zapisy w dzienniku muszą być kolejno numerowane, - przy prowadzeniu ksiąg rachunkowych przy użyciu komputera zapis księgowy powinien posiadać automatycznie nadany numer pozycji, pod którą został wprowadzony do dziennika. Chronologia zapisów w dzienniku powinna być zachowana według dat zapisów księgowych, a nie według dat dokonania operacji gospodarczych. Z art. 15 ust 1 UoR wynika, że na kontach księgi głównej obowiązuje ujęcie zarejestrowanych uprzednio lub równocześnie w dzienniku zdarzeń zgodnie z zasadą podwójnego zapisu, co oznacza, że zapisy w dzienniku nie mogą być wtórne do zapisów księgowych na kontach księgi głównej - pole znakowe (dla poszczególnych dzienników), np. 1/Zak/01/2016, 280/Sprz/01/2016 |

Number of an entry in the journal assigned in sequence during a financial year in accordance with the requirement specified in Article 14(2) and Article 14(4) of the Accounting Act: - entries in the journal must be numbered in sequence, - an entry should automatically be assigned a number with which it is entered in the journal where the accounting books are kept using a computer. The chronology of entries in the journal should reflect the dates on which entries are made and not the dates of business transactions. Article 15(1) of the Accounting Act specifies that entries in general ledger accounts must be made for events recorded previously or simultaneously in the journal in accordance with the double-entry method, hence, entries in the journal cannot be secondary to the entries made in general ledger accounts – character field (for particular journals), e.g. “1/Zak/01/2025”, “280/Sprz/01/2025”. The series must be gapless and chronological:

|

| D2 | Opis dziennika - pole znakowe. Dzienniki częściowe stosowane przez jednostkę, jako element ksiąg rachunkowych zgodnie z art. 14 ust. 3 i 4 UoR. Powinny one zostać opatrzone nazwą np. Zakup, Sprzedaż | Journal description – character field. Partial journals used by an entity as an element of accounting books in accordance with Article 14(3) and Article 14(4) of the Accounting Act. These should be named for instance “Zakup” (Purchase) and “Sprzedaż” (Sale). |

| D3 | Kod kontrahenta identyfikujący jednoznacznie podmiot w systemie finansowo-księgowym jednostki- identyczny jak w elemencie T_1 w sekcji Kontrahent | Counterparty code which provides unique identification of an undertaking in the financial and accounting system of the entity – the same as in theT_1 element in the Kontrahent section (optional field). |

| D4 | Numer identyfikacyjny dowodu nadany przez wystawcę dowodu księgowego, zgodnie z wymogiem art. 21 ust. 1 pkt 1 UoR – pole znakowe | Identification number of accounting evidence assigned by its issuer as required by Article 21(1)(1) of the Accounting Act (character field). |

| D5 | Rodzaj dowodu księgowego (który stanowi podstawę zapisu księgowego, o czym mowa w art. 23 ust. 2 pkt 2 UoR) umieszczony na dowodzie księgowym przez wystawcę, zgodnie z art. 21 ust. 1 pkt 1 UoR - pole znakowe | Type of accounting evidence (which is the basis of an entry, as referred to in Article 23(2)(2) of the Accounting Act) identified on the accounting evidence by the issuer in accordance with Article 21(1)(1) of the Accounting Act (character field). |

| D6 | Data dokonania operacji gospodarczej, o której mowa w art. 23 ust. 2 pkt 1 UoR, umieszczona na dowodzie księgowym przez jego wystawcę, zgodnie z wymogiem określonym w art. 21 ust. 1 pkt 4 UoR – pole daty, np. 2016-01-02 |

Date of business transaction referred to in Article 23(2)(1) of the Accounting Act, identified on the accounting evidence by the issuer as required by Article 21(1)(4) of the Accounting Act (date field, e.g. “2025-01-02”). This will be the Tax Point Date whenever it is used by the user, or else it will be the Transaction Date. |

| D7 | Data sporządzenia dowodu księgowego, o której mowa w art. 23 ust. 2 pkt 2 UoR, umieszczona na dowodzie księgowym przez jego wystawcę, zgodnie z wymogiem określonym w art. 21 ust. 1 pkt 4 UoR. Jeśli dowód został sporządzony pod ate dokonania operacji gospodarczej I brak jest na dowodzie daty sporządzenia dowodu księgowego, to zgodnie z art. 21 ust. 1 pkt 4, w polu należy umieścićateę operacji gospodarczej.–- pole daty, np. 2016-01-02 | Date of preparation of the accounting evidence referred to in Article 23(2)(2) of the Accounting Act, identified on the accounting evidence by the issuer as required by Article 21(1)(4) of the Accounting Act. If the evidence is prepared prior to the date of the business transaction and no date of preparation of the accounting evidence is provided thereon, in accordance with Article 21(1)(4), the date of the business transaction should be entered in the field (data field, e.g. “2016-01-02”). |

| D8 | Data, pod którą ujęto dowód w księgach | Date with which the evidence is entered in the books (data field, e.g. “2016-01-02”). |

| D9 | Dane pozwalające na ustalenie osoby odpowiedzialnej za treść zapisu zgodnie z wymogiem określonym w art. 14 ust. 4 UoR – pole znakowe, np. E Nowak | Data enabling identification of the person responsible for the contents of the entry as required in Article 14(4) of the Accounting Act (character field, e.g. “Nowak”). |

| D10 | Opis operacji gospodarczej, o której mowa w art. 23 ust. 2 pkt 3 UoR, umieszczony na dowodzie księgowym przez jego wystawcę, zgodnie z wymogiem określonym w art. 21 ust. 1 pkt 3 UoR, lub zrozumiały tekst, skrót lub kod opisu operacji, z tym że należy posiadać pisemne objaśnienia treści skrótów lub kodów – zgodnie z art. 23 ust. 2 pkt 3 UoR - pole znakowe | Description of a business transaction referred to in Article 23(2)(3) of the Accounting Act, included on the accounting evidence by the issuer as required by Article 21(1)(3) of the Accounting Act, or comprehensible text, abbreviation or code of the transaction description, with the proviso that written explanations of the abbreviations or codes should be provided – in accordance with Article 23(2)(3) of the Accounting Act (character field, up to 512 characters). |

| D11 | Kwota operacji gospodarczej, o której mowa w art. 23 ust. 2 pkt 4 UoR, wynika z wartości operacji gospodarczej zamieszczonej przez wystawcę dowodu księgowego, zgodnie z art. 21 ust. 1 pkt 3 UoR - pole kwotowe | Amount of a business transaction referred to in Article 23(2)(4) of the Accounting Act, resulting from the value of the business transaction identified by the issuer of accounting evidence in accordance with Article 21(1)(3) of the Accounting Act (numeric field). |

| D12 | Numer identyfikujący fakturę lub fakturę korygującą w Krajowym Systemie e-Faktur (KSeF). Pole wymagane dla operacji, które dokumentowane są fakturą lub fakturą korygującą wystawioną przy użyciu KSeF przez podmiot składający JPK | Number identifying the invoice or correction invoice in the National e-Invoice System (KSeF). The field is required for transactions documented with an invoice or a correction invoice issued using the KseF by an entity filing the JPK (optional field). |

Tax Settlements Section RPD

This node will collectively display differences between the balance sheet and tax results, broken down into these categories:

- K_1: Tax-exempt income.

- K_2: Non-taxable income in the current year.

- K_3: Revenues subject to taxation in the current year, recorded in the accounts of previous years.

- K_4: Costs that are not deductible for tax.

- K_5: Costs not recognized as tax deductible costs of obtaining income in the current year.

- K_6: Costs recognized as costs of obtaining income in the current year, recorded in the books of previous years.

- K_7: Taxable income not recognized in the accounting books.

- K_8: Costs considered as PURCHASES not included in the accounting books.

The JEPL_JPK_RPD lookup type may be introduced for the above tax settlements:

- A new lookup code for each of the K_1 to K_8 values for each fiscal year where the user can enter manually the amounts calculated externally for the different tax elements. Each lookup-code will have the indication of the fiscal year and the Tax Registration number of the organization. The dates will also identify the time period for which the amount is in effect. The actual amounts will be entered manually by the user at the tag column.

- A new logic to derive these values from the system income tax information. This can also be used for reconciliation purposes between system-based income tax information and external book-keeping for off-balance tax transactions. This specification identified the need for an additional hierarchy “branch” with the JPK one, and additional Journal entries at the end of the fiscal year for these non-operational accounts. As the TA has requested that at least for the first years of implementation the tax amounts will be entered manually in the relative (JEPL_JPK_RPD) lookup only; and the setup and maintenance of having the external book-keeping entries for off-balance tax transactions to be entered in the system is exceeding the benefits of this feature, this is not included in our scope for the JPK_KR_PD.

Revert to Old Format for Audit Purposes

To revert to old format of past fiscal years, follow these steps:

- Disable the JE_37558149 lookup code of the ORA_ERP_CONTROLLED_CONFIG lookup type and then disable the new hierarchy (with the actual natural accounts and their parents), and set it as Draft, while you activate the old hierarchy with the JPK parents.

- Go to Manage Chart of Accounts Structure Instances task and set the old hierarchy tree as the hierarchy tree of your natural account segment.

- The reverse order of actions is required once the audit data have been extracted to return to the new format.

- After each configuration change on the hierarchies and their structure reference, you must deploy the Accounting Flexfield.