This chapter describes the details of Tiered Balance Interest Rate.

Topics:

· Overview

Tiered balance interest is when a different interest rate is paid/charged for parts of an account balance that fall within set amount ranges. For example:

Balance Tiers |

Interest Rate |

|---|---|

| $0 - $1,999 | X% |

| $2,000 - $24,999 | Y% |

$25,000 and above |

Z% |

If there is $30,000 in an account that pays tiered interest, X% is paid on the first $1,999, Y% is paid on the amount from $2,000 to $24,999 and Z% is paid on the amount from $25,000 to $30,000. The interest rate of each tier can be separately managed. For example, X% may be fixed for life, Y% may be floating pegged to an administered rate and Z% may be adjustable pegged to an interest rate curve. Some attributes like payment frequency, current payment, etc. will be at the account level (and common across all tiers) while some like reprice frequency, next reprice date, etc. will be unique at the tier level.

This functionality is supported for Loans (Mortgages and Loan Contracts) and Term Deposits.

Salient features of this functionality are:

The interest rate for an account is given for a balanced range in table STG_ACCOUNT_RATE_TIERS.

1. Adjustable type of each tier can be different - Fixed (0), Floating Rate (50), or Adjustable (250). It cannot be a reprice pattern.

2. Reprice frequency, last, and next reprice date can be different for each tier. In case of multiple reprice i.e. more than one reprice taking place during one payment period, accrued interest (from last payment date to as of date) is required separately for each tier to make the initial interest cash flow more accurately. If accrued interest is not given, interest is calculated from the last payment date using the current interest rate.

3. Amortization type, current payment, last and next payment date, payment frequency, the remaining number of payment, maturity date given at account level is used. Thus, the same attributes will be used for all tiers.

4. Current payment: ALM uses CUR_PAYMENT from the account for the life of the record until a payment re-calculation occurs for adjustable rate records and the next reprice date is reached. In the case of tiered rates since the next reprice date is at tier level and current payment only at the account level, it will not be re-calculated. Thus, the current payment given for the account will be used until maturity. Due to changes in the interest rate and constant current payment, effective maturity can get curtailed (when forecasted rates go down leading to higher principal payment) or extended (when forecasted rates go up leading to lower principal payment). If curtailment occurs then the account will mature on the calculated maturity date which can be earlier than the given maturity date. If extension occurs then all remaining principal balance will get repaid on the given maturity date (similar to balloon amortization).

5. Teaser functionality does not apply to accounts with a tiered rate. Teaser accounts are those where the interest rate is fixed for some time at the start. In the case of tiered rates since each balance range can have different adjustable types including fixed, teaser functionality is not applicable. Thus, teaser end date and other related attributes if given at account level are ignored.

6. When the adjustable type of tier is floating or adjustable then the interest rate is derived using current logic i.e. in case of floating rate changes as per IRC and in case of adjustable it changes based on reprice frequency. Rates are subject to the cap, floor, lag, minimum change, rate increase/decrease period/life and other attributes given at account level.

7. When one or multiple tiers uses floating or adjustable rate then the interest rate curve is expected for each tier. The interest rate curve can be different for each tier. Net Margin Cd, Gross Rate does not apply to these types of accounts.

8. Forecast Rates Scenario for each tier works in the same way as it is at the account level. Each tier that is tied to an IRC will be forecasted and new future rates will be derived based on Repricing Date and Repricing Frequency.

9. Rate Change Min, Rate Decrease Cycle, Rate Increase Cycle, Rate Set Lag, Rate Cap Life, Rate Floor Life, and other related attributes given at account level are used.

10. The current interest rate (Cur_Net_Rate), if any, given at the account level is ignored and the interest rate of each tier is used for calculations. The interest cash flow of each tier is calculated separately during a payment period and added together for further calculations like principal payment etc.

11. When repayment and prepayment occurs, current balance reduces from tiers based on ranking. Normally tier with the highest interest rate gets the highest rank. Rank will be supplied by the source system.

12. Prepayment and early redemption

Prepayment models: When the dimension used in the prepayment model is coupon rate, market rate, or rate ratio then the highest interest rate applicable to tiers is used to make prepayment decisions. The market rate will depend on the IRC of the tier with the highest interest rate.

The prepayment amount is calculated using the balance of the account and then allocated to individual tiers based on rank.

13. Tiered rate functionality applies to all amortization types except negative amortization (600), annuity (850), and lease (840). The tiered rate is not expected in these cases.

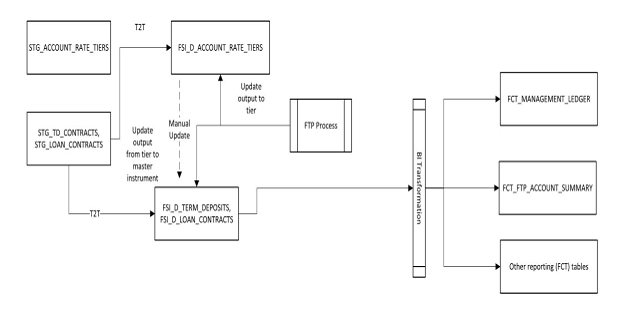

Below figure shows the ALM data flow:

Description of ALM Data Flow as follows

Below figure shows the FTP data flow:

Description of FTP Data Flow as follows

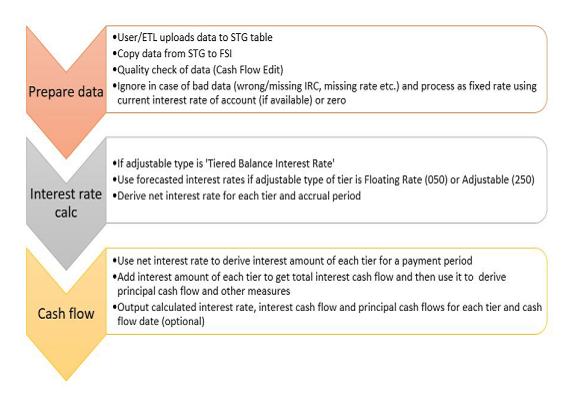

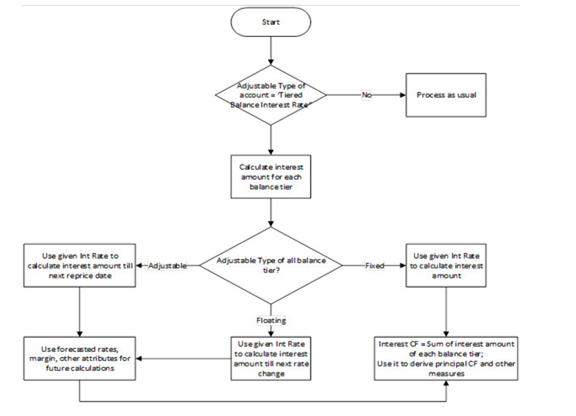

Description of Tiered balance interest rate Process Flow as follows

Tiered balance interest rate is calculated as below for Liquidity gap, Repricing gap, Market value, Duration, YTM, DV01, Average Life, and Income simulation.

· Liquidity gap

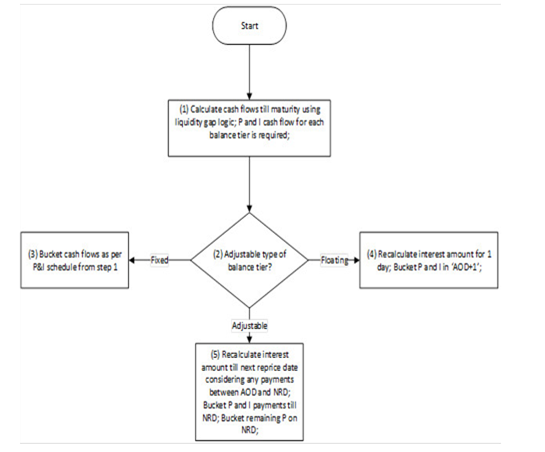

Below flow chart shows how Tiered balance interest rate is calculated for Liquidity gap:

Description of Tiered balance interest rate Process Flow for Liquidity gap as follows

Principal payments are first reduced from balance tier with the highest rank.

· Repricing gap

Tiered balance interest rate is calculated for the repricing gap as follows:

a. If the adjustable type of tier is ‘Fixed (000)’, then runoff as per schedule.

b. If the adjustable type of tier is ‘Floating (050)’ then runoff on ‘As of date + 1’ i.e. first-time bucket.

c. If the adjustable type of tier is ‘Adjustable (250)’ then

i. Runoff as per schedule till next reprice date

ii. Remaining principal after scheduled payments will runoff on next reprice date

Description of Tiered balance interest rate Process Flow for Repricing gap as follows

· Market value

This is calculated for each balance tier separately and then the weighted average market value is calculated for the account. The current par balance of the tier is used as a weight.

· Duration

This is calculated for each balance range separately and then the weighted average duration is calculated for the account. MARKET_VALUE_C * CUR_PAR_BAL / 100 of the tier is used as a weight.

· Current Yield (YTM)

This is calculated for each balance range separately and then weighted average YTM is calculated for the account. The current par balance of the tier is used as a weight.

· Convexity

This is calculated for each balance range separately and then weighted average convexity is calculated for the account. MARKET_VALUE_C * CUR_PAR_BAL / 100 of the tier is used as a weight.

· Modified duration

This is calculated for each balance range separately and then weighted average modified duration is calculated for the account. MARKET_VALUE_C * CUR_PAR_BAL / 100 of the tier is used as a weight.

· DV01:

This is calculated for each balance range separately and then weighted average DV01 is calculated for the account. MARKET_VALUE_C * CUR_PAR_BAL / 100 of the tier is used as a weight.

· Average life:

This is calculated for each balance range separately and then weighted average life is calculated for the account. The current balance of the tier is used as a weight.

· Income simulation

This is calculated at the tier level and then aggregated.

Transfer Rates and TP Adjustment Rates

The FTP application will run directly against the FSI_D_ACCOUNT_RATE_TIERS table and will treat each tier record as an independent instrument record. Transfer Rates and TP Adjustment rates will be calculated based on the details of each rate tier record. Aggregation of tier level results and posting back to the parent record is not yet supported but can be handled by a custom procedure.