United States: Manage Catch-Up Contribution Eligibility for SECURE Act 2.0 Section 603

Manage catch-up contribution eligibility to help comply with Section 603 of the US SECURE Act 2.0. Section 603 requires that employees eligible for catch-up contributions to 401(k) or other qualified deferred compensation plans make those catch-up contributions on a Roth or after-tax basis when they exceeded a wage limit in the prior tax year.

With this release, EBS US Benefits administrators can use updated eligibility options and savings plan enrollment setup to assist with Section 603 compliance. The feature introduces Person Extra Information Type support, formula setup, eligibility profiles, and savings plan configuration patterns for pre-tax and Roth catch-up eligibility.

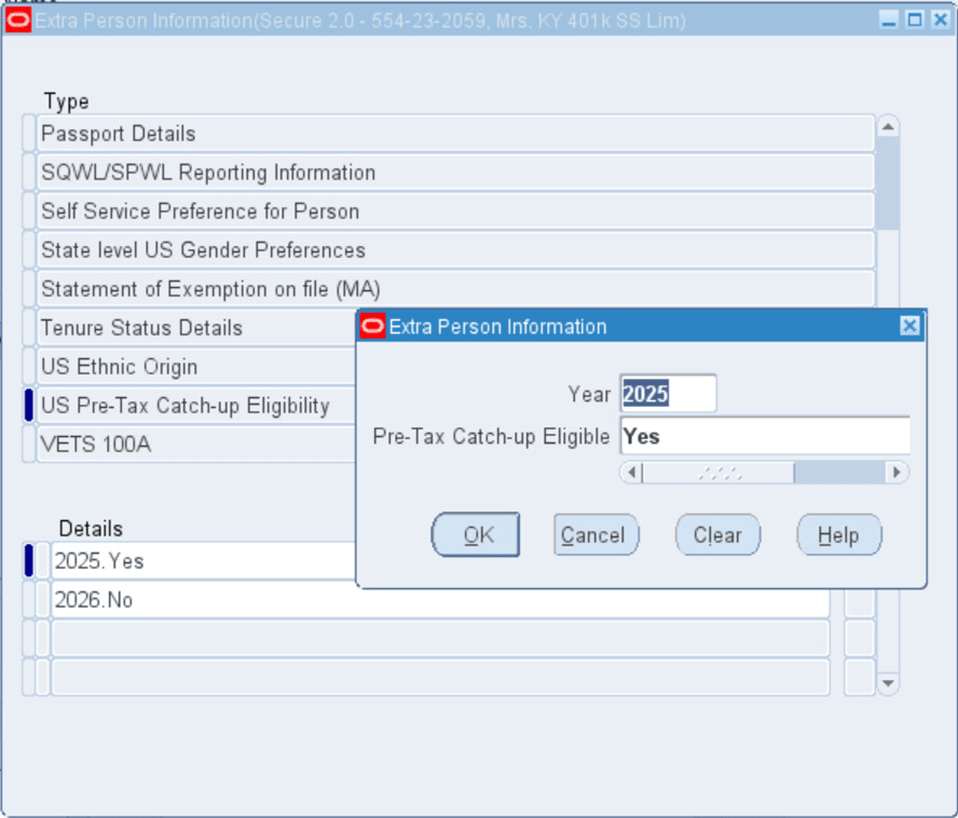

US Pre-Tax Catch-up Eligibility Person EIT

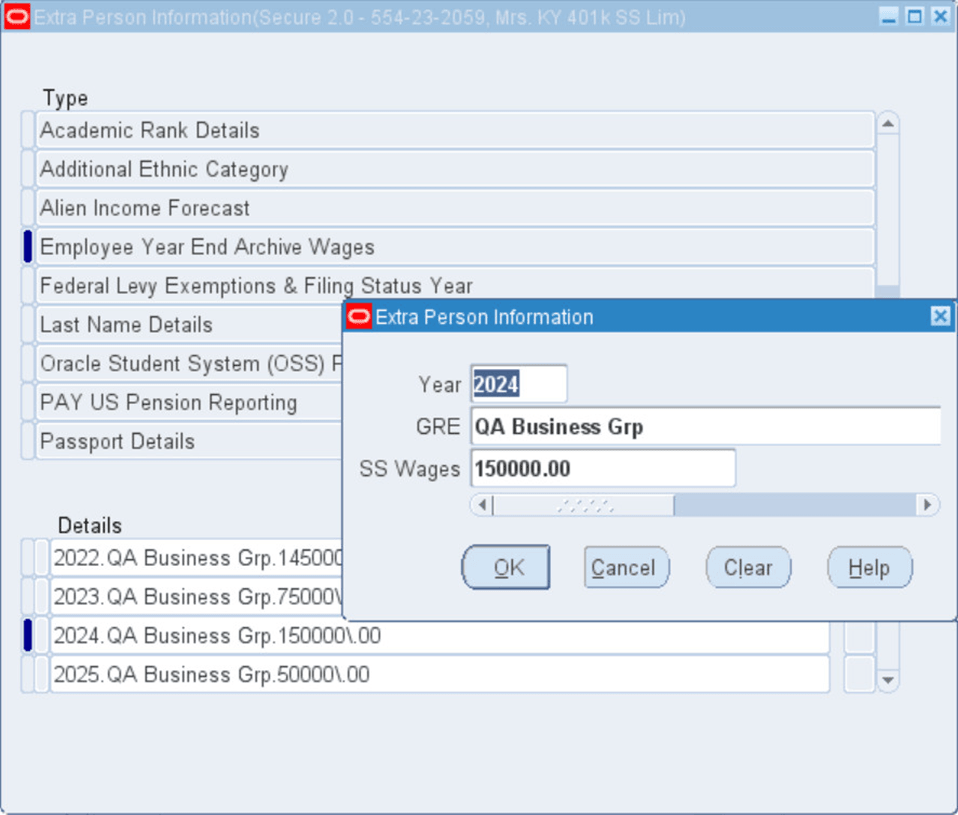

Employee Year End Archive Wages Person EIT

This feature helps organizations ensure compliance with updated retirement plan regulations by accurately identifying employees eligible for enhanced catch-up contributions. This improves payroll and benefits administration efficiency, reduces compliance risks, and supports employees in maximizing their retirement savings opportunities through timely and accurate contribution processing.

Steps to enable and configure

- Use the Person Extra Information Type US Pre-Tax Catch-up Eligibility to identify whether the employee is eligible for pre-tax catch-up contributions for the applicable year.

- If using EBS US Payroll data, use the Employee Year End Archive Wages EIT with the SECURE Act Section 603 Wage Limit user table to help determine eligibility.

- Create a new formula function using ben_aca_utils.pre_tax_catchup_eligible.

- Add context usages ASSIGNMENT_ID and DATE_EARNED, and add parameters P_PERSON_ID and P_TAX_UNIT_ID.

- Create a Participation and Rate Eligibility fast formula that calls the new formula function.

- Create the needed savings plans, including pretax savings, pretax catch-up, and Roth catch-up plans.

- Create and attach eligibility profiles for pretax base plan eligibility, Roth and pretax enrollment exclusions, and the Section 603 pretax eligibility rule.

- Validate enrollment results for employees with Pre-Tax Catch-up Eligible set to Yes, No, or left null.

Tips and considerations

- Do not manually update Employee Year End Archive Wages; it is populated by the application when the Year End or W-2c Preprocess is run.

- Review values in US Pre-Tax Catch-up Eligibility and Employee Year End Archive Wages if eligible individuals do not see the expected pretax catch-up option.

- Coordinate Benefits and Payroll setup when using payroll-derived wage data.

Key resources

Oracle HRMS Compensation and Benefits Management Guide (US)

- Chapter: Setup for Health and Welfare Management

- Overview of Retirement Savings and SECURE Act 2.0

- Processing Employee Retirement Savings According to the Provisions of the SECURE Act 2.0

- Determining Employee Eligibility According to the Provisions of the SECURE Act 2.0

Transfer of Information

R12.2.14 TOI: Implement and Use Advanced Benefits, Core Payroll and HRMS (US)