Manage Catch-Up and Employer Match Contributions for SECURE Act 2.0

With this release, US Payroll Administrators can ensure compliance with the requirements of Sections 603 and 604 of the SECURE Act 2.0.

- Section 603 requires that, effective in 2024 and later, employees who are eligible to make catch-up contributions to their 401(k) or other qualified deferred compensation plans must do so on a Roth (or after tax) basis if they earned over a certain wage limit in the prior tax year. An exception has been made for workers earning under the wage limit in the prior year who are still permitted to contribute catch-up amounts on a pre-tax basis.

- Section 604 allows employers to offer matching contributions to employee 401(k), 403(b) and 457 contributions on a Roth (or after tax) basis. Prior to the enactment of SECURE Act 2.0, these could only be offered on a pre-tax basis.

Complying with Sections 603 and 604 of SECURE Act 2.0 enables organizations to accurately administer retirement plan catch-up contributions and Roth contribution requirements while maintaining compliance with evolving U.S. retirement regulations. This reduces the risk of payroll and tax reporting errors, streamlines benefits administration, and enhances employee confidence by ensuring retirement savings contributions are processed correctly and efficiently.

Feature Description

New Pre-Tax Deduction Categories

To support the provisions in Sections 603 and 604, Oracle maintains separate Roth elements for catch-up and employer match processing.

The following deferred compensation deduction categories enable you to comply with the regulations included in Sections 603 and/or 604:

- Deferred Comp 401k - SECURE 2.0

- Deferred Comp 403b - SECURE 2.0

- Deferred Comp 457 - SECURE 2.0

These categories are available in the Deduction window, Classification field. When creating pre-tax or tax deferred 401(k) or 403(b) deductions and enabling catch-up contributions, a separate catch-up deduction element is created.

New Catch-Up Processing Option

The "Post Sequential" Catch-Up processing option is applicable to pre-tax 401(k), 403(b), or 457 deductions that are created using the "SECURE 2.0" categories. With this Catch-Up option, catch-up processing will not start in the same pay period that the base deduction reaches the annual limit, but instead will start in the next pay period.

In the Deduction window, this option is available in the Catch-Up Processing option group.

This Catch-Up processing option is also available to the following element entry input values in the Entry Values window:

- <Base Element> Catchup - Catchup Processing

- <Base Element> Roth Catchup - Catchup Processing

New Input Value

To comply with the Section 604 requirement of optionally offering employer matches to qualified retirement plans on a Roth (after-tax) basis, use the "ER Match Type" input value. This input value is available for the following elements that are created when a 401(k), 403(b), or 457 deduction element is created using the "SECURE 2.0" tax category.

- <Base_Element>

- <Base_Element> Catchup

- <Base_Element> Roth

- <Base_Element> Roth Catchup

The ER Match Type input value has "Pre-Tax Basis" and "Roth Basis" options. It has a default value of Pre-Tax Basis for base (i.e. pre-tax) and base Catch-up elements and Roth Basis for Roth and Roth Catch-up elements. This input value is available in the Entry Values window for an employee.

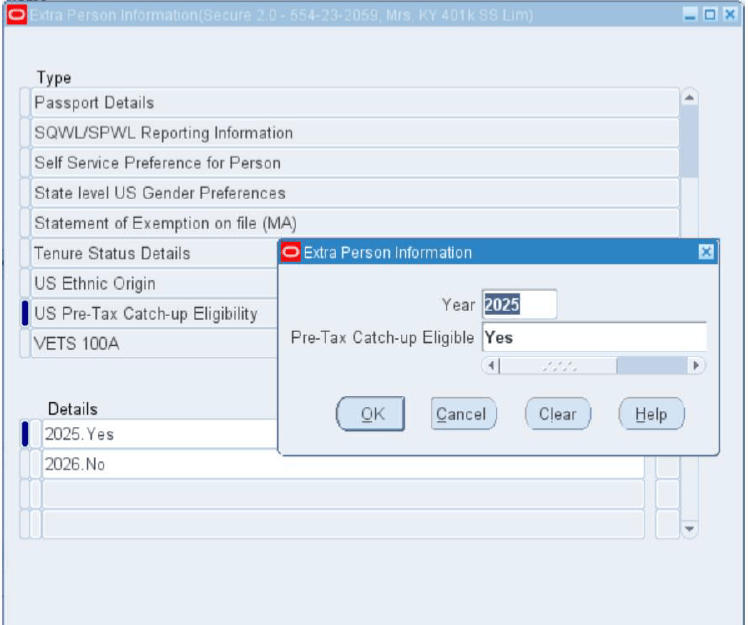

New Person Extra Information Type

US Pre-Tax Catch-up Eligibility EIT

For employees who have elected to make catch-up contributions to their 401(k)/403(b)/457 plans, the US Pre-Tax Catch-up Eligibility EIT determines who is eligible to make pre-tax 401(k), 403(b), (and/or 457(b)) catch-up contributions and who is not, and therefore can only make catch-up contributions on a Roth or after-tax basis.

This EIT has the following parameters:

- Year

- Pre-Tax Catch-up Eligible

New Person Extra Information Type

If you are an Oracle US Payroll customer, you can also have employee eligibility for pre-tax catch-up contributions determined automatically in the 401(k), 403(b) and 457 catch-up processing formula using the "Employee Year End Archive Wages" internal-only EIT. This EIT will be populated with the employee's W-2 Box 3 (Social Security wages) amount when the Year End Pre-Process (or W-2c PreProcess) is run for the applicable reporting year and GRE.

This EIT has the following parameters:

- Year

- GRE

- SS Wages

New User Table

The "SECURE Act Section 603 Wage Limit" user table stores the applicable wage limit in effect for Section 603. The value stored in the field "SS Wages" in the Person EIT "Employee Year End Archive Wages" is compared to the value stored in the user table. Oracle Benefits uses information in this table to determine whether the employee is eligible to make catch-up contributions to their 401(k), 403(b), and/or 457(b) plan on a pre-tax or Roth (post-tax) basis.

Steps to enable and configure

Refer to the implementation information in the following transfer of information:

R12.2.14 TOI: Implement and Use Advanced Benefits, Core Payroll and HRMS (US)

Tips and considerations

Refer to the following transfer of information for tips and best practices:

R12.2.14 TOI: Implement and Use Advanced Benefits, Core Payroll and HRMS (US)

Key resources

Oracle HRMS Compensation and Benefits Management Guide (US)

- Chapter: Setup for Health and Welfare Management

- Overview of Retirement Savings and SECURE Act 2.0

- Processing Employee Retirement Savings According to the Provisions of the SECURE Act 2.0

- Determining Employee Eligibility According to the Provisions of the SECURE Act 2.0

Transfer of Information

R12.2.14 TOI: Implement and Use Advanced Benefits, Core Payroll and HRMS (US)