Defining Equitization Rules

This section provides an overview of equitization and discusses how to:

Establish equitization rules for processing equitization.

Establish non-controlling interest only equitization rules.

Establish dividend reclassification equitization rules.

Establish source elimination equitization rules.

Establish equitization rule sets.

Establish equitization groups.

Pages Used to Define Equitization Rules

|

Page Name |

Definition Name |

Navigation |

Usage |

|---|---|---|---|

|

Equitization Rule |

GC_EQTZ_RULE |

|

Establish an equitization rule. |

|

Equitization Rule - Source |

GC_EQTZ_SOURCE |

|

Specify the source ChartField values to equitize. |

|

Equitization Rule - Target |

GC_EQTZ_TARGET |

|

Specify the target accounts for equitization. |

|

Equitization Rule - Non-Controlling Interest |

GC_EQTZ_MIN_INT |

|

Specify the accounts to offset earnings attributed to non-controlling interest. |

|

Equitization Rule - Subsidiary Offset |

GC_EQTZ_OFFSET |

|

Specify the accounts to offset the total equitized source amount. |

|

Equitization Rule - Dividend Reclassification |

GC_EQTZ_DIV |

|

Specify the source and target accounts for a dividend reclassification equitization rule. This page is only available when the equitization rule processing option is set to Dividend Reclassification |

|

Equitization Rule - Notes |

GC_EQTZ_RULE_NOTES |

|

Enter notes about an equitization rule. |

|

Equitization Rule Set |

GC_EQTZ_SET |

|

Associate ownership sets with equitization rules to calculate the equitization adjustments and identify the set of equitization rules that should be used for subsidiaries. |

|

Equitization Rule Set - Notes |

GC_EQTZ_SET_NOTES |

|

Enter notes about an equitization rule set. |

|

Equitization Group |

GC_EQTZ_GROUP |

|

Define the equitization rule sets that comprise an equitization group and the order in which to process them. Include all the equitization rule sets needed to describe every subsidiary for which the system should process equitization. |

|

Equitization Group - Notes |

GC_EQTZ_GRP_NOTES |

|

Enter notes about an equitization group. |

Understanding Equitization Rules

Equitization rules post a subsidiary's net income or loss to its parent company's books, as a debit to investment and a credit to equity income. The equitization process records current period changes in a parent's investment in subsidiaries, based on the subsidiary's changes in equity. This process then creates the related elimination entries and books them to the elimination entity.

You have the option of calculating and accounting for non-controlling interest or reversing the target amounts that result from equitization; whether you need to do this depends on which accounts you're using as input into the consolidation process. If year-to-date (YTD) elimination for investment is taken care of for equitization processing, you do not want the NCI eliminations (part of processing eliminations) to generate them again; that is why the option to reverse the target amounts from equitization is provided.

Equitization rules are processed differently, depending the on the ledger template associated with the consolidation model. When the Processing Method selection on the Ledger Template-Consolidation Variables page is set to Use year-to-date data, the system uses the ownership percentage at the historic period end date for each period processed. This ensures that the equity pickup entries are based on historical ownership. If the processing method is set to Use period data, only the specified period is processed

See Defining Ledger Templates.

When a subsidiary's equity changes during the year, its parents will want to update their books to reflect those changes. This is important because it gives an accurate depiction of those parent statements on a standalone basis if these companies are reporting separately to regulatory agencies. When the organization as a whole presents its consolidated financial statements, this change in value requires elimination. The only impact that equitization should have on the consolidated reports is to show the portion of the subsidiary's change in equity for the current period or year that belongs to outside owners (non-controlling interest), if applicable.

The following example, using a trial balance format consolidation ledger, shows the results of the equitization.

The parent owns 70 percent of the subsidiary. Net income for the subsidiary is 100 USD; therefore, the parent's portion is 70 percent of this amount. The equitization process will create journals to debit 70 USD to the parent's investment account and credit 70 USD to the equity income account for this period:

|

Balance Sheet/Income Statement |

Subsidiary |

Parent |

|---|---|---|

|

Period 1 |

Period 1 |

|

|

Cash, receivables, and so forth |

100 USD |

230 USD |

|

Investment in subsidiary |

70 USD (a) |

|

|

Revenues |

–1,000 USD |

–2,230 USD |

|

Expenses |

900 USD |

2,000 USD |

|

Equity income |

–70 USD (a) |

When producing consolidated financial statements, you need to eliminate your equitization entries and create non-controlling interest entries related to the equity generated by the subsidiary during the period. These are both options with the equitization process. If specified, the equitization process creates the elimination entries that "back out" the equitization entries and sends them to the proper elimination entity as indicated in the consolidation tree. It also calculates the non-controlling interest expense and liability for the subsidiary's equity for the period. This example shows these entries:

|

Subsidiary |

Parent |

Elimination |

|

|---|---|---|---|

|

Period 1 |

Period 1 |

Period 1 |

|

|

Cash, receivables, and so forth |

100 USD |

230 USD |

|

|

Investment in subsidiary |

70 USD (a) |

–70 USD (b) |

|

|

Non-Controlling interest liability |

–30 USD (c) |

||

|

Revenues |

–1,000 USD |

–2,230 USD |

|

|

Expenses |

900 USD |

2,000 USD |

|

|

Equity income |

–70 USD (a) |

70 USD (b) |

|

|

Non-Controlling interest expense |

30 USD (c) |

Notice that the effect of the equitization to the parent's account (b) has been removed by eliminating the equitization entry (a). The non-controlling owner's claims on the subsidiary's net income for the period has also been taken into account by increasing the non-controlling interest liability and non-controlling interest expense (c).

Equitization Threshold

When you run the equitization process, the system uses the selection in the Equitize Parent field of the Ownership Rule-Ownership Percentage page to determine whether to equitize changes in subsidiary equity for each parent-subsidiary relationship.

When the Equitize Parent field is set to Use Threshold, the equitization threshold percent is compared to the control percentage for each subsidiary and parent relationship. When the cumulative control percentage is greater than or equal to the equitization threshold percent, specified on the Ownership Rule or Ownership Group page, subsidiary equity is equitized, using the ownership percentage to determine the amount for each subsidiary and parent relationship.

When the Equitize Parent field is set to Yes, the change in equity is always equitized, regardless of the parents controlling percentage.

When the Equitize Parent field is set to No, the change in subsidiary equity is not equitized to the direct parent, however it will be equitized to any indirect parent where the threshold is met, unless the Equitize Parent field is set to No for that parent as well.

The equitization threshold percentage can be specified on both the Ownership Group page and the Ownership Rule page. The threshold value that you enter on the Ownership Group page applies to all entities within the scenario. You can override this value at the parent level on the Ownership Rule page, by completing the Threshold Percent and Specify Threshold fields on the Ownership Rule page. .

See Ownership Rule Page.

See Ownership Group Page.

Equitization Method

The method by which you account for changes in subsidiary equity varies depending on the control percentage of the parent. This table outlines the general guidelines that apply:

|

Parent Control Percentage |

Method |

Description |

|---|---|---|

|

Less than 20 percent |

Cash |

Initial purchase of portion of the subsidiary is recorded as investments in subsidiary (asset). Dividends from the subsidiary are recorded as cash received (income). In this situation, the subsidiary data is probably not loaded into the consolidation ledger (CLED). |

|

From 20 percent through 49 percent |

Equity |

Initial purchase of portion of subsidiary recorded as investment in subsidiary (asset). The investment in subsidiary changes as the subsidiary records change in equity (income). In this situation, the subsidiary balances probably would be loaded into the CLED to facilitate equitization. However, you most likely would not consolidate—unless there are other parents in the organization that bring in enough additional control of the subsidiary to force consolidation. |

|

50 percent or greater |

Consolidate |

The subsidiary's balances are loaded into the consolidation ledger. Need to define equitization rule to compute and record any non-controlling interest liability for the investment in subsidiary. To view the parent as a stand alone entity, you might choose to equitize, but then define the rule so that you eliminate the equitization afterwards. |

Equitization Processing Options

The processing options that you can select for an equitization rule are:

Equitization.

Use when you are employing the equity method to account for changes in subsidiary equity.

Non-controlling interest only.

Use when you are employing the consolidation accounting method for a subsidiary, to generate the NCI expense for subsidiary equity.

Dividend reclassification.

Use to redistribute dividends received from subsidiaries and the associated tax withholding accounts. Applicable in cases where dividends that were recorded as income at lower levels of an organization need to be reclassified at higher levels of an organization where ownership percentages dictate the use of the equity method.

Source elimination.

Valid only for financial-statement-based consolidation ledgers. Use to eliminate the balances of the equitization source accounts that you identify. This is used in conjunction with the equitization processing option.

Specific rules should be defined for each specific processing option that you use. The processing option that you select dictates which pages appear in the equitization rule component. Once you define and save an equitization rule, you cannot change the processing option. By defining multiple rules using different processing options, and then grouping them into related equitization rule sets and an equitization group, you can process all these situations at one time within your consolidation model.

The following pages are available for specific processing options:

|

Page Name |

Equitization |

Non-Controlling Interest Only |

Dividend Reclassification |

Source Elimination |

|---|---|---|---|---|

|

Equitization Rule |

Yes |

Yes |

Yes |

Yes |

|

Source |

Yes |

Yes |

No |

Yes |

|

Target |

Yes |

No |

No |

No |

|

Non-controlling interest |

Yes |

Yes |

No |

Yes |

|

Subsidiary Offset |

Yes |

No |

No |

No |

|

Dividend Reclassification |

No |

No |

Yes |

No |

|

Notes |

Yes |

Yes |

Yes |

Yes |

The following sections describe how to define a rule for each type of processing option. By defining multiple rules using different processing options, as needed, you can process all of these situations at one time within your consolidation model.

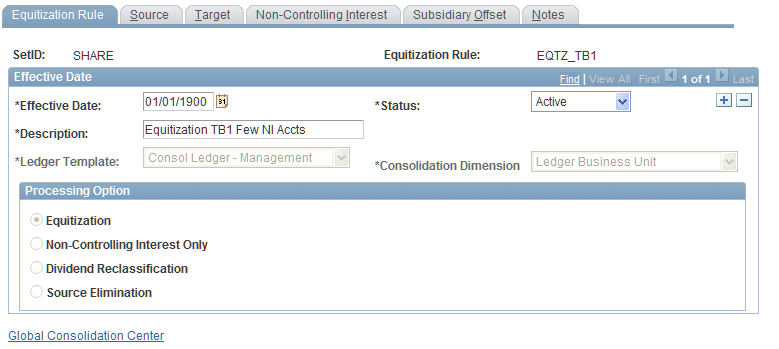

Equitization Rule Page

Use the Equitization Rule page (GC_EQTZ_RULE) to establish an equitization rule.

Image: Equitization Rule page

This example illustrates the fields and controls on the Equitization Rule page. You can find definitions for the fields and controls later on this page.

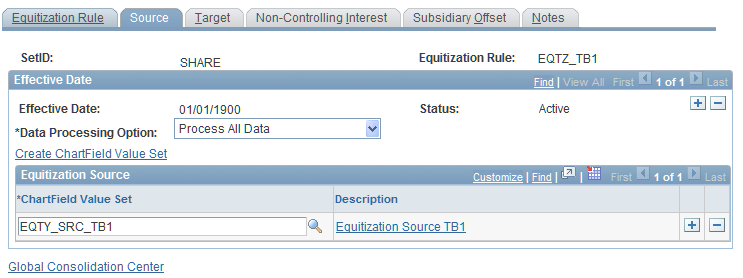

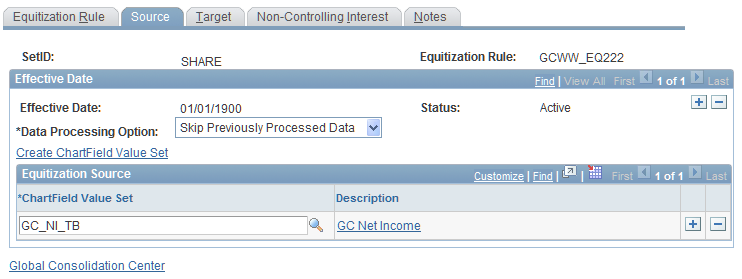

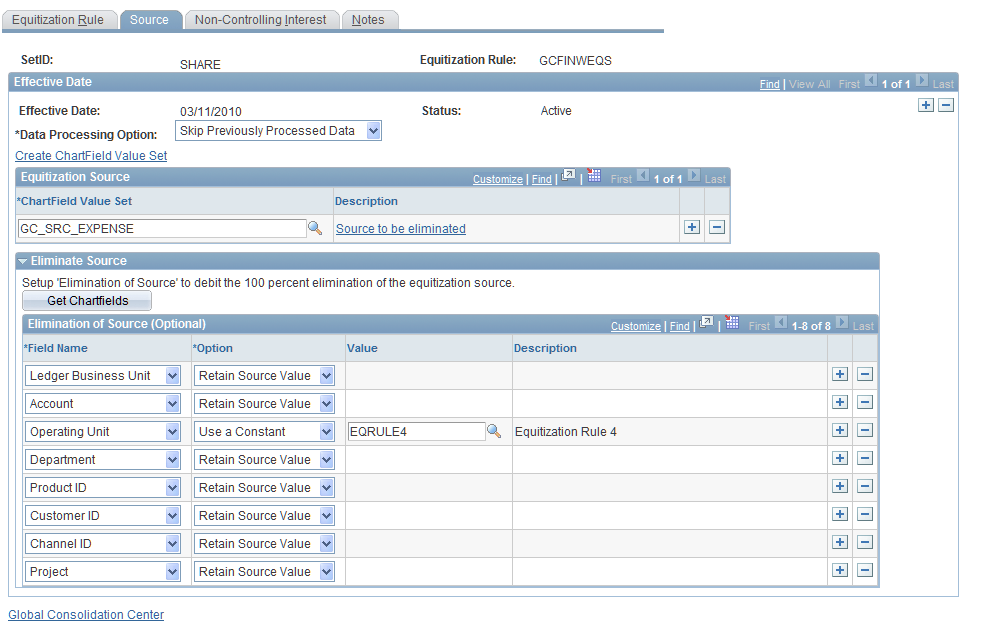

Specifying Equitization Sources

Use the Equitization Rule - Source page (GC_EQTZ_SOURCE) to specify the source ChartField values to equitize.

Image: Equitization Rule - Source page

This example illustrates the fields and controls on the Equitization Rule - Source page. You can find definitions for the fields and controls later on this page.

Equitization Source

Select one or more ChartField value sets containing the accounts to equitize. Typically these are the accounts that store the subsidiary's current income (or earnings).

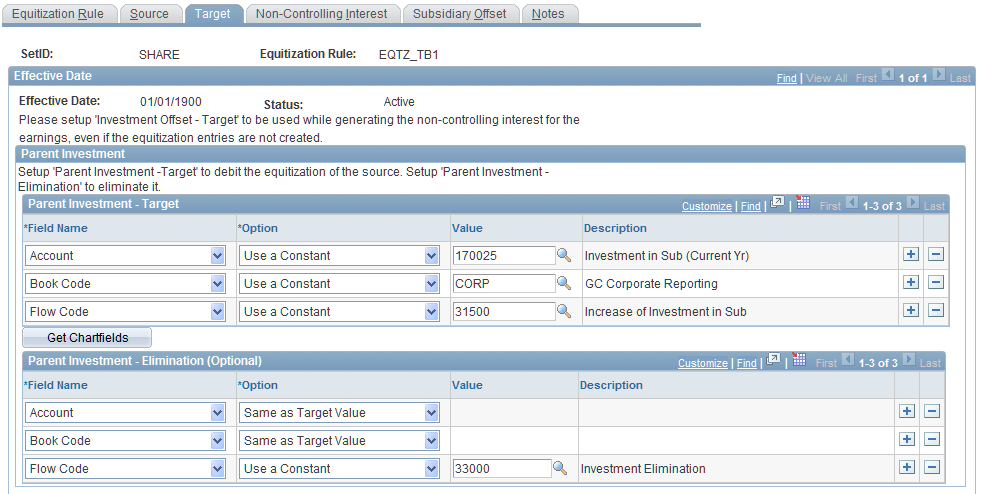

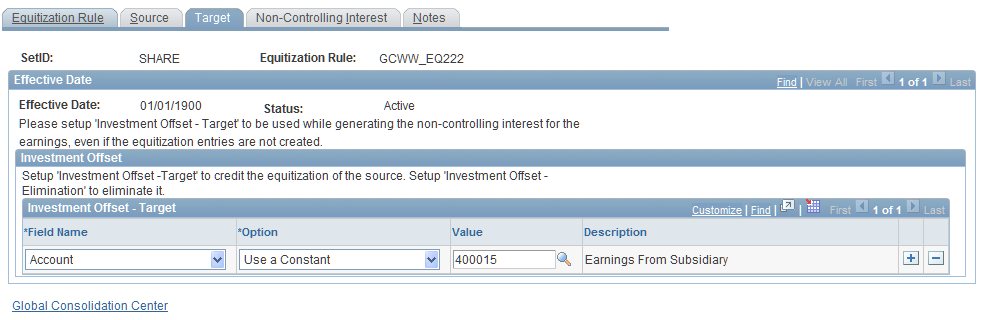

Specifying Equitization Targets

Use the Equitization Rule - Target page (GC_EQTZ_TARGET) to specify the target accounts for equitization.

Image: Equitization Rule - Target page (1 of 2)

This example illustrates the fields and controls on the Equitization Rule - Target page (1 of 2). You can find definitions for the fields and controls later on this page.

Image: Equitization Rule - Target page (2 of 2)

This example illustrates the fields and controls on the Equitization Rule - Target page (2 of 2). You can find definitions for the fields and controls later on this page.

This page's contents differ depending on the consolidation ledger format. The example shown is for a financial statement format.

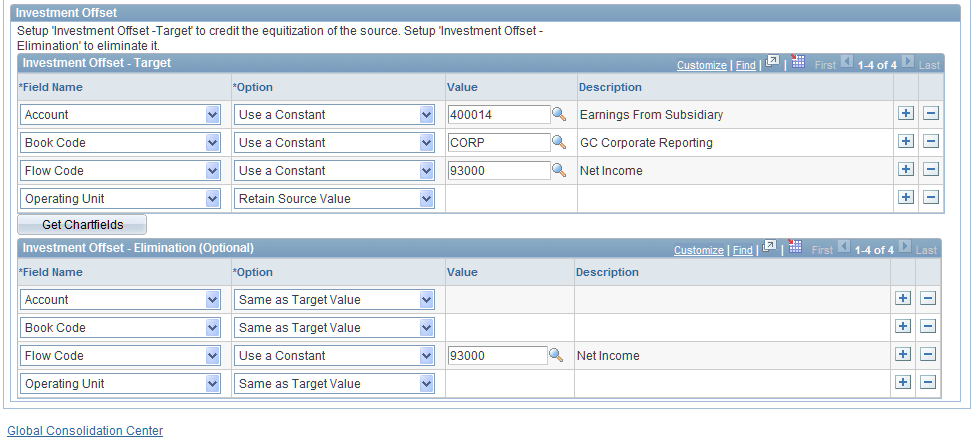

Specify the accounts on the parent to which the change in subsidiary equity is recorded by completing the fields within the Parent Investment and Investment Offset group boxes. Entries are booked for the percent of subsidiary source owned by the parent.

For financial-statement-based consolidation ledgers only, complete the fields within the Offset Balancing grid to credit the equitization of the source.

| Offset Balancing - Target |

Specify the target ChartFields to offset (or balance) the parent investment target entry (credit). Typically this is an equity account. |

For each grid, enter values in these fields:

Note: For financial statement format consolidations, the parent investment and offset balance must be balance forward account types and the investment offset must be a non-balance forward account type. You can set up a three-sided entry (all three accounts) or a one-sided entry (just the investment offset account).

Eliminating Non-Controlling Interest for Subsidiary Equity (Optional)

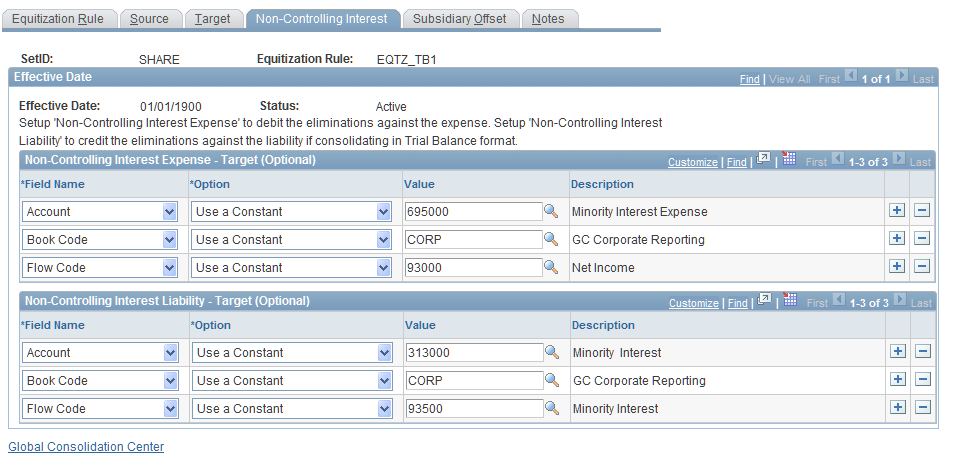

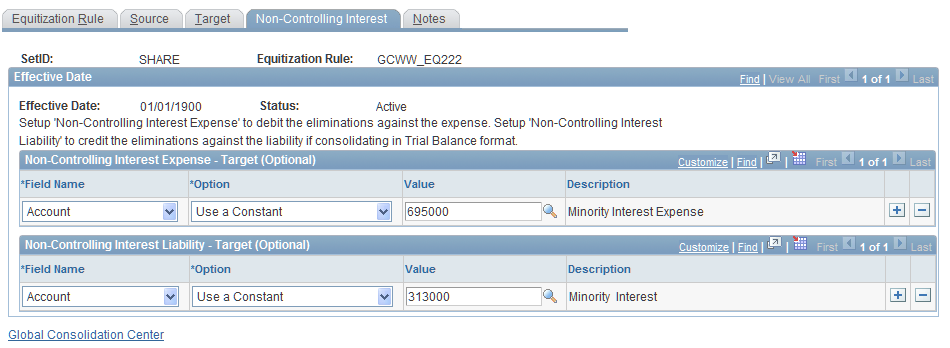

Use the Equitization Rule - Non-Controlling Interest page (GC_EQTZ_MIN_INT) to specify the accounts to offset earnings attributed to non-controlling interest.

Image: Equitization Rule - Non-Controlling Interest page

This example illustrates the fields and controls on the Equitization Rule - Non-Controlling Interest page. You can find definitions for the fields and controls later on this page.

This page's contents differ depending on the consolidation ledger format. The example shown is for a financial statement format.

Complete this page to enable the system to calculate the amount of non-controlling interest liability and expense and post it to the accounts specified on this page. Entries are booked to the elimination entity for the non-owned percentage. The system increases the non-controlling interest liability and non-controlling interest expense accounts for trial balance format consolidation ledgers. For financial statement format consolidation ledgers, this affects only the non-controlling interest expense account.

Complete the following grids:

For each grid, enter values in these fields:

To specify additional ChartFields, such as department, insert additional rows.

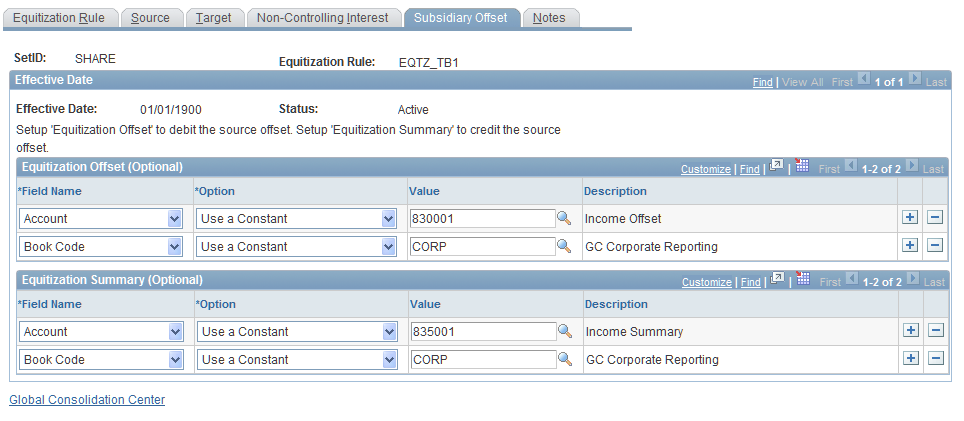

Subsidiary Offset (Optional)

Use the Equitization Rule - Subsidiary Offset page (GC_EQTZ_OFFSET) to specify the accounts to offset the total equitized source amount.

Image: Equitization Rule - Subsidiary Offset page

This example illustrates the fields and controls on the Equitization Rule - Subsidiary Offset page. You can find definitions for the fields and controls later on this page.

Complete this page if you want to offset the total equitized source amount (which is booked against an elimination entity) to a specified account. Entries are booked at 100 percent of source. This enables you to move the amount to a separate account, for reporting purposes.

Identify the ChartFields to use for the equitization offset and equitization summary. This offsets the total equitized source amount to the equitization summary account specified in the rule by debiting the equitization offset account for the subsidiary and crediting the equitization summary. These entries are booked against the subsidiary.

Equitization Rule Page (Non-Controlling Interest)

Use the Equitization Rule (GC_EQTZ_RULE) page to establish an equitization rule.

Specifying the Source

Use the Equitization Rule - Source (GC_EQTZ_SOURCE) page to specify the source ChartField values to equitize.

Image: Equitization Rule - Source page

This example illustrates the fields and controls on the Equitization Rule - Source page. You can find definitions for the fields and controls later on this page.

The Source page contains the ChartField value sets used for processing non-controlling interest only.

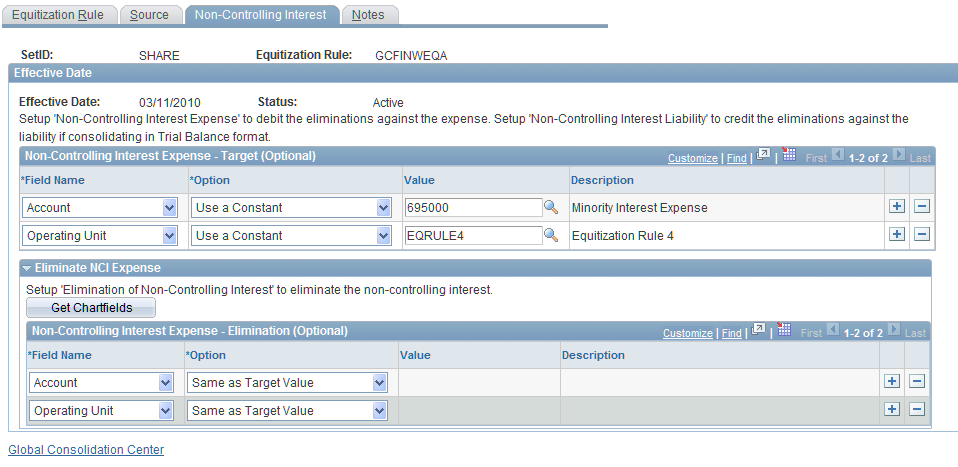

Specifying the Target

Use the Equitization Rule - Target page to specify the target accounts for equitization.

Image: Equitization Rule - Target page

This example illustrates the fields and controls on the Equitization Rule - Target page. You can find definitions for the fields and controls later on this page.

Use the Investment Offset - Target grid to specify the accounts to use when computing amounts due to non-controlling interest. The system uses the accounts to temporarily store the information that it needs to compute non-controlling interest. Even though you are not using this rule to equitize, the system must use this to compute amounts for cases of indirect ownership with multiple levels.

| Parent Investment - Target |

Specify the target ChartFields. Account is required. |

Eliminating Non-Controlling Interest for Subsidiary Equity

Use the Equitization Rule - Non-Controlling Interest page to sthe accounts to offset earnings attributed to non-controlling interest.

Image: Equitization Rule - Non-Controlling Interest page

This example illustrates the fields and controls on the Equitization Rule - Non-Controlling Interest page. You can find definitions for the fields and controls later on this page.

This page's contents differ depending on the consolidation ledger format. The example shown is for a trial balance format.

By completing this page, when you process equitization the system calculates the amount of the current period or YTD subsidiary equity accounts (subsidiary income) that is attributed to outside owners. The amount due to non-controlling interest is booked to the elimination entity. The system increases the non-controlling interest liability and non-controlling interest expense accounts for trial balance format consolidation ledgers. For financial statement format consolidation ledgers, this affects only the non-controlling interest expense account.

For the account ChartField, you must select Constant, and specify the ChartField value for the appropriate account. To specify additional ChartFields, such as department, insert additional rows.

Equitization Rule Page (Dividend Reclassification)

Use the Equitization Rule page to establish an equitization rule.

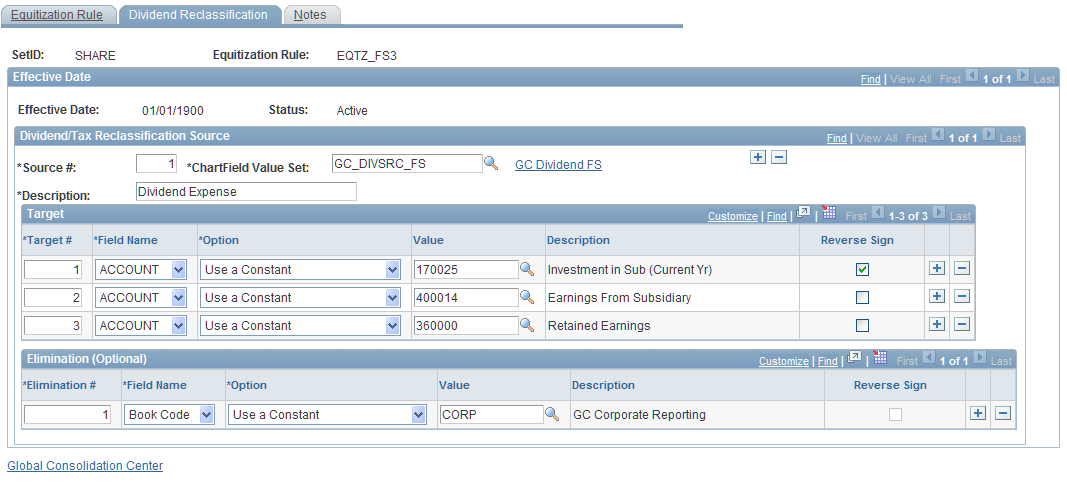

Specifying the Dividend Reclassification Source

Use the Equitization Rule - Dividend Reclassification page (GC_EQTZ_DIV) to specify the source and target accounts for a dividend reclassification equitization rule.

This page is only available when the equitization rule processing option is set to Dividend Reclassification

Image: Equitization Rule - Dividend Reclassification page

This example illustrates the fields and controls on the Equitization Rule - Dividend Reclassification page. You can find definitions for the fields and controls later on this page.

Dividend reclassifications need to occur when there is a subsidiary that is owned by multiple parents and where, in total for all parents, there is enough control held to require equitization, but for some individual parents, the level of control is below the equitization threshold. For the parents whose control is below the equitization threshold, the dividend is recorded as income; this needs to be reclassified when you reach the appropriate level of the tree at which the equitization threshold is met.

To properly reclassify the dividends, it is necessary to make two sets of entries. The first set of entries is made against the equitizing parent. This adjusts the data for the equitizing parent, but does not totally correct the overall consolidated results. So, a second set of entries is made to the common elimination unit between the direct parent and the equitizing parent. These are not true elimination entries in the respect that they are directly eliminating the entries made against the parent. Rather they are an independent set of reclassification entries that need to be made to the elimination unit to adjust the overall consolidation.

The equitizing parent and the entries for the elimination unit are independent of one another. In both cases, the process reads the source, and makes the appropriate entries to each business unit to constitute a balanced set of entries. The reverse sign is used the same way in each case. Some entries read the source amount and keep the same sign while others reverse the sign to make the balanced entry. This flag is always in reference to the source.

Use dividend reclassification to redistribute dividends received from subsidiaries and the associated tax withholding accounts. Dividend reclassification is applicable in situations where:

Dividends were recorded as income at lower levels of the organization.

Dividends now need to be reclassified at higher levels of an organization where ownership percentages dictate the use of the equity method.

Specify the ChartFields to use for dividend reclassification by completing the fields within the Dividend/Tax Reclassification Source group box.

Equitization Rule Page (Source)

Use the Equitization Rule (GC_EQTZ_RULE) page to establish an equitization rule.

Note: Source elimination rules can be defined only for financial-statement-based consolidation ledgers.

Specifying the Source for Source Elimination

Use the Equitization Rule - Source (GC_EQTZ_SOURCE) page to specify the source ChartField values to equitize

Image: Equitization Rule - Source page

This example illustrates the fields and controls on the Equitization Rule - Source page. You can find definitions for the fields and controls later on this page.

Source elimination rules can only be defined for financial statement based consolidation ledgers. You can eliminate the equitization source by creating source elimination equitization rules. Source elimination is typically used in conjunction with an equity pickup rule. The equity pickup rules takes the source, equitizes the owned percentage to the parent, and equitizes the non-owned percentage to non-controlling interest. The source elimination should have the same source ChartField value set as the regular equity pickup rule. It completely eliminates the source and reverses the non-controlling interest created by the pickup.

Specifying the Non-Controlling Interest Accounts for Source Elimination (Optional)

Use the Equitization Rule - Non-Controlling Interest page to specify the accounts to offset earnings attributed to non-controlling interest.

Image: Equitization Rule - Non-Controlling Interest page

This example illustrates the fields and controls on the Equitization Rule - Non-Controlling Interest page. You can find definitions for the fields and controls later on this page.

Complete this page to reverse the non-controlling interest..

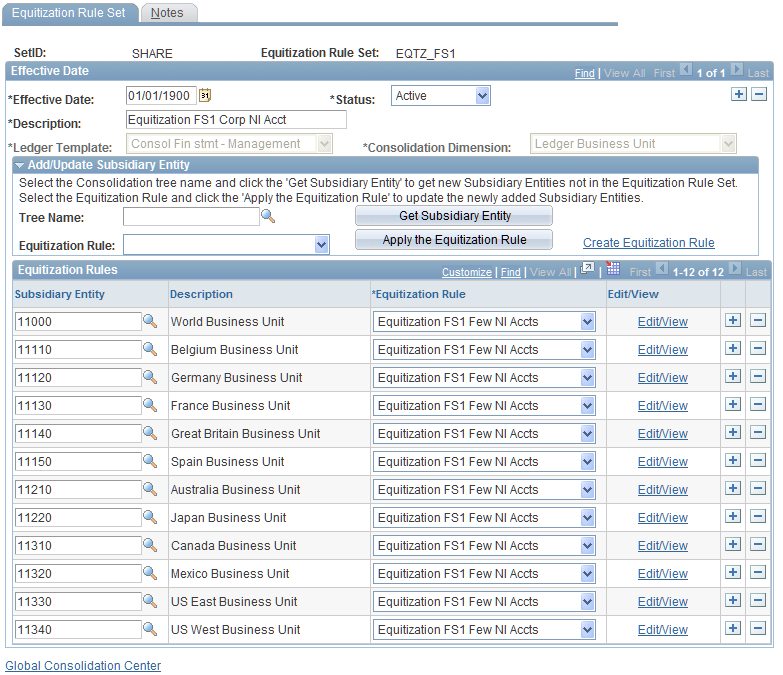

Equitization Rule Set Page

Use the Equitization Rule Set (GC_EQTZ_SET) page to associate ownership sets with equitization rules to calculate the equitization adjustments and identify the set of equitization rules that should be used for subsidiaries.

Image: Equitization Rule Set page

This example illustrates the fields and controls on the Equitization Rule Set page. You can find definitions for the fields and controls later on this page.

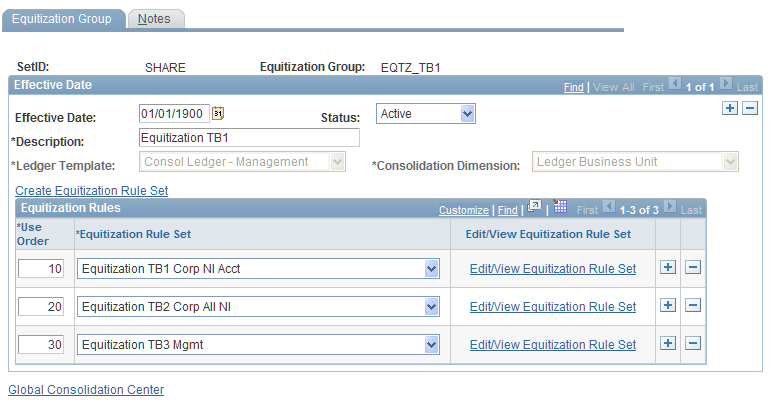

Equitization Group Page

Use the Equitization Group page (GC_EQTZ_GROUP) to define the equitization rule sets that comprise an equitization group and the order in which to process them.

Include all the equitization rule sets needed to describe every subsidiary for which the system should process equitization.

Image: Equitization Group page

This example illustrates the fields and controls on the Equitization Group page. You can find definitions for the fields and controls later on this page.

Within the Equitization Rules grid, specify all of the equitization rule sets to include in this equitization group, adding additional rows as needed. Include all of the equitization rule sets needed to identify every subsidiary for which equitization should be processed, because only one equitization group is assigned to a consolidation model.

Enter the use order value. Rule set processing occurs in ascending order based on the number in this field. If you selected the data processing option, Skip Previously Processed Data, and the same data exists in multiple rule sets, the first time the data encountered it is used. If you selected the data processing option, Process All Data, the data is processed again for the rule in the rule set appearing in a later sequence order.