Collection Criteria vs. Write Off Criteria

The following diagram introduces important concepts related to the C&C processes:

| Statement | Meaning |

|---|---|

| An account's debt comes from its contracts | An account's debt is managed at the contract level, i.e., the system keeps track of how much a customer owes in respect of each contract. In order to determine an account's balance, the system must add up the debt on each of the account's contracts. |

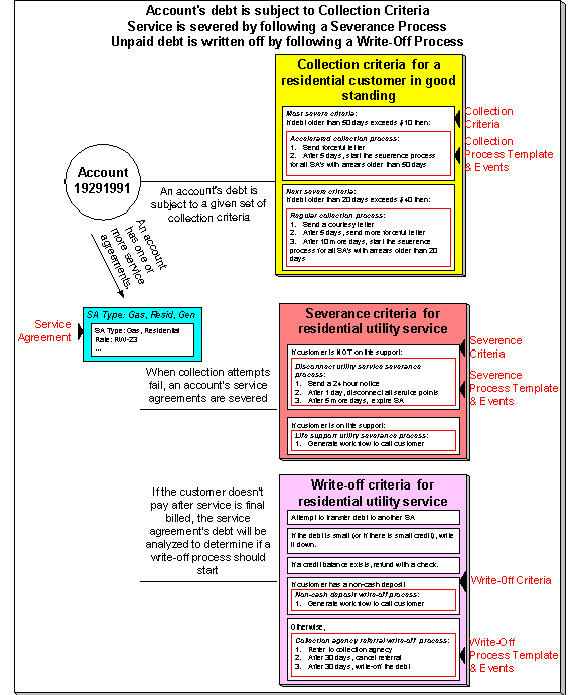

| Collection criteria define intolerable debt | Collection criteria are control data that define intolerable debt. Most criteria are defined using a combination of number of days in arrears and a dollar amount. |

| Collection criteria may be compared to an account's total debt or to subsets of debt | If your organization has simple collection procedures, you will probably target collection criteria at an account's total debt. However, you have the option of segregating an account's debt into debt classes and targeting the collection criteria at each class. For more information about debt classes, see Different Collection Criteria For Different Customers And Different Debt . |

| Collection criteria also define what to do when the level of intolerable debt is exceeded | When you define collection criteria, you also define how the system should respond if an account violates your criteria. These collection events are defined in respect of a "collection process template". |

| There are usually several collection events that take place when criteria are violated | A collection process template usually has several collection events. Each event is meant to prod the customer to pay. The initial collection events are typically letters. |

| After a contract is severed, it will be final billed | When the last active contract linked to an account is stopped, the system changes the account's bill cycle to bill that evening. If only one of many contract's is stopped, the contract will only be final billed as per the account's original bill cycle schedule. |

| If a customer doesn't pay their final bill, the account's debt will be analyzed to determine if the system can reduce the debt to zero using a variety of mechanisms |

The system will look at an account's finaled debt on its next scheduled credit review date (typically a few days after the bill's due date). The system will attempt to reduce the contract's debt to zero using all of the following methods:

|

| If a customer's finaled debt cannot be reduced via any of the previous methods, the system creates a write-off process |

A write-off process contains one or more write-off events. These events can generate a letter, send a To Do entry to a CSR, send a referral to a collection agency, etc. When you set up the system, you define the type of write-off process to use for every collection class / write-off debt class combination. In addition, you can also indicate when the type of write-off process should differ depending on some attribute of the customer. For example, you may have a different write-off process if the customer has a non-cash deposit. |

| The last write-off event typically causes the debt to be written off | Ultimately, if the write-off events fail, the debt will have to be written off. When debt is written-off, the system creates a write-off contract and transfers the outstanding debt to it. This means the debt stays with the account for life and will have to be paid off if the customer ever returns. |